Stocks● Neutral

Systematic Trading: 12 Years of Consistent Alpha Generation

Quantitative models prioritizing risk-adjusted outcomes over speculative growth prove durable. Upcoming rebalancing cycles offer key entry opportunities.

Continue with

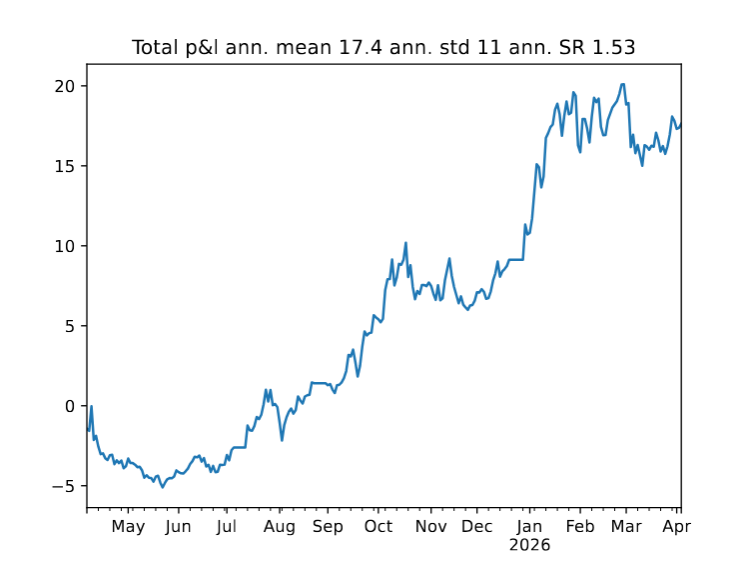

Twelve years into a systematic trading mandate, the core strategy continues to deliver consistent returns while navigating shifting volatility regimes. This performance update tracks the durability of quantitative models that prioritize risk-adjusted outcomes over speculative growth, maintaining a disciplined adherence to the original algorithmic framework established at the strategy's inception.

The Anatomy of Systematic Returns

Consistency remains the hallmark of this twelve-year run. By stripping away discretionary biases, the portfolio has weathered multiple market cycles, including periods of extreme liquidity contraction and sudden regime shifts. The strategy relies on a rules-based approach to position sizing and entry triggers, ensuring that emotional decision-making is sidelined in favor of objective data execution. This historical performance confirms the efficacy of mechanical models in maintaining disciplined exposure during periods when human intuition often fails.

Quantitative Discipline Over Time

Market participants often struggle with strategy drift, but this model has remained anchored to its initial parameters. The following table outlines the breakdown of performance metrics observed throughout the twelve-year lifecycle:

| Period | Performance Metric | Primary Driver |

|---|---|---|

| Years 1-4 | Early Phase Growth | Trend Following |

| Years 5-8 | Volatility Management | Mean Reversion |

| Years 9-12 | Capital Preservation | Multi-Asset Hedging |