Stocks● Neutral

How Middle East Instability Forces Global Risk Recalibration

Escalating regional conflict threatens supply chains and energy flows, forcing investors to adjust risk models as diplomatic friction triggers volatility.

Continue with

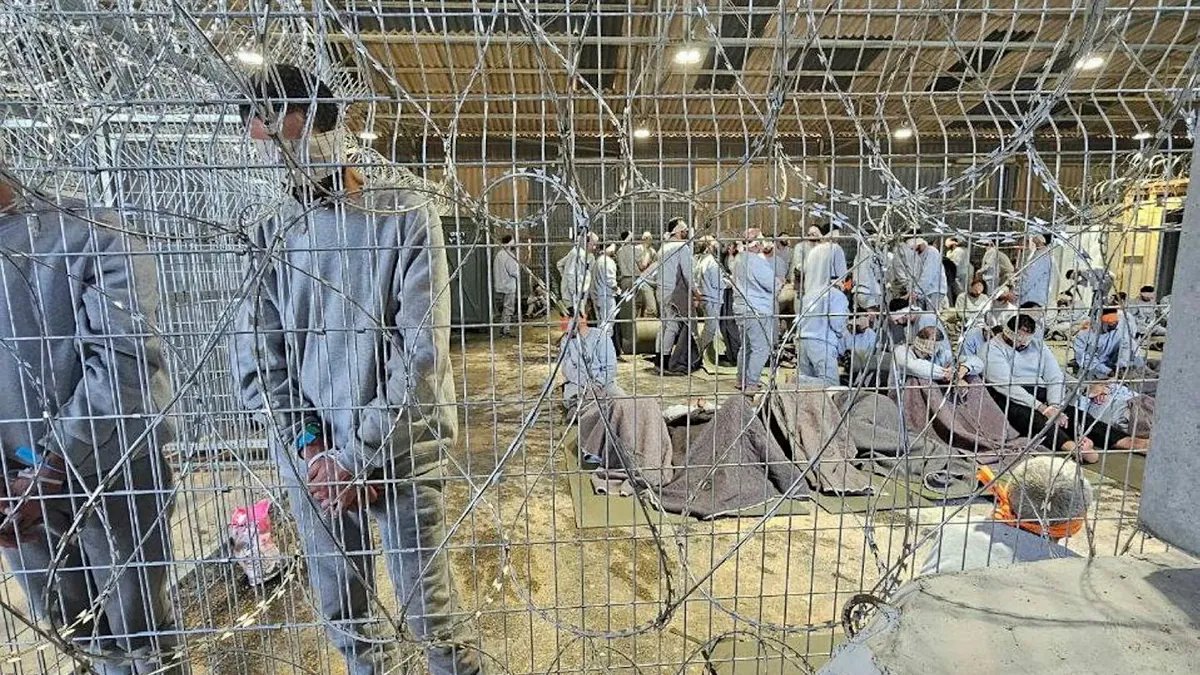

The release of the report titled ‘Another Genocide Behind Walls’ has intensified scrutiny regarding the stability of the Middle East and its subsequent impact on global supply chains. As reports of conflict-related atrocities circulate, the resulting diplomatic friction creates immediate uncertainty for multinational corporations operating within the region. Investors are now forced to recalibrate their risk models to account for potential escalations that could disrupt logistics, energy flows, and regional trade partnerships.

Impact on Regional Operational Continuity

For companies with significant exposure to the Levant and surrounding territories, the primary concern is the potential for sudden operational shutdowns or localized sanctions. The current narrative surrounding the humanitarian situation increases the likelihood of political intervention, which often manifests as sudden shifts in trade policy or security-related costs. When regional instability reaches a threshold that triggers international diplomatic responses, the cost of doing business for firms in the energy and infrastructure sectors typically rises due to heightened insurance premiums and security requirements.

This environment forces a re-evaluation of how South Korea Deploys Emergency Liquidity to Shield Exporters from Middle East Conflict might serve as a template for other nations managing trade-dependent economies. When major exporters face disruption, the immediate reaction from central banks is to provide liquidity to prevent a broader contagion effect. This pattern of intervention is a critical marker for investors tracking the resilience of global supply chains against localized geopolitical shocks.