The $380 Target: What Changed in the Apple Thesis

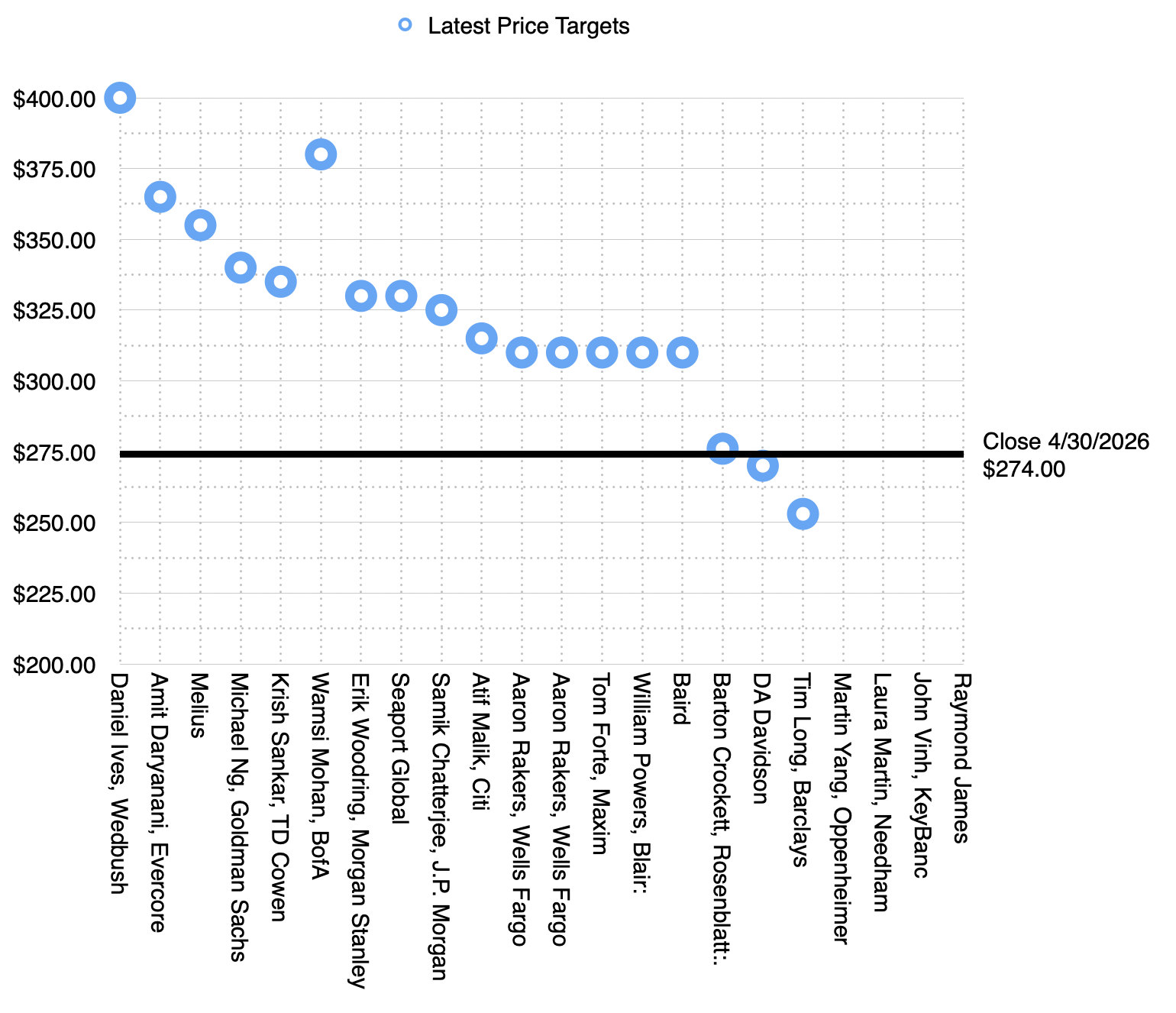

Bank of America raised its price target on Apple Inc. to $380 from $330, keeping a Buy rating. The revision follows a detailed analysis by analyst Wamsi Mohan on how agentic artificial intelligence could reshape the company’s revenue base. The new target is about 23% above the current price of $308.33.

The upgrade is not about iPhone unit sales or Services growth in the near term. It rests on a structural thesis: Apple’s control over silicon, iOS, and the user identity layer positions it as the default platform for AI agents that act on behalf of users. In Mohan’s words, “value accrues to the platform that controls user intent, personal context, app access, permissions, identity, authentication, payments, and trust.” The smartphone is the device where all of those factors already converge.

How Agentic AI Changes Apple’s Competitive Position

The Silicon and Software Moat

Mohan’s analysis points to two assets that competitors cannot easily replicate: Apple’s custom silicon and iOS. On-device processing is critical for latency, reliability, privacy, and cost. Apple’s A-series and M-series chips already handle machine learning workloads. The company’s Neural Engine and Secure Enclave give it an edge in running AI models locally while preserving user privacy.

iOS determines how AI interacts with apps, permissions, and payments. If AI assistants become the primary interface for search, commerce, and scheduling, the operating system’s control over those functions becomes a revenue lever. Mohan notes that Apple can dictate what happens on the device and how the AI is used by the user.

Distributed Compute Architecture

Token usage at scale forces a hybrid approach. Mohan writes, “Our analysis around token usage suggests Apple will need to rely on distributed compute (on device), Private Cloud Compute and third-party compute to deliver a robust AI experience.” Apple’s Private Cloud Compute infrastructure is still in early stages. The company has removed its net cash neutral target, which Mohan sees as a signal that a new period of AI-driven investment has begun.

The Revenue Case for an Agentic Siri

A $15B to $65B Opportunity by 2030

Mohan estimates that an agentic version of Siri could generate $15B to $30B in incremental revenue in fiscal 2030 under a baseline adoption scenario. If users become highly acclimated to the agent, the range expands to $40B to $65B. That would represent a meaningful addition to Apple’s current Services revenue, which ran at about $85B in fiscal 2024.

These numbers assume that Siri becomes capable of understanding intent, retrieving context, bringing up apps, and completing workflows. The redesign requires integrating large language models into the iPhone operating system while maintaining the privacy architecture that Apple markets as a differentiator.

What Needs to Happen

The path from the current Siri to a full agent is not technically trivial. The assistant must:

- Understand user intent across apps and contexts

- Access personal data with granular permission controls

- Execute multi-step workflows (booking, paying, scheduling)

- Rely on distributed compute to keep latency low and privacy intact

Any failure in reliability or privacy could slow adoption. Competitors like Google and Samsung are also pushing agentic AI on their own devices, though their platforms lack the same level of hardware-software integration and permission infrastructure.

Valuation and the Alpha Score Context

At $308.33, Apple trades at roughly 31x trailing earnings – a premium that already prices in some Services growth. The BofA upgrade adds a new long-duration option on AI monetization. The Alpha Score of 66/100 from AlphaScala labels Apple as Moderate, suggesting that the current price reflects fair risk-adjusted expectations. The score does not yet fully discount the agentic AI thesis, which depends on execution over the next three to five years.

What Confirms or Weakens the Thesis

The BofA target relies on three concrete markers:

- Siri redesign details in any future iOS preview – if Apple shows a functional agent, the stock could re-rate higher.

- Capital expenditure disclosures – any increase in infrastructure spending for Private Cloud Compute signals commitment, not just experiments.

- Developer adoption – if third-party apps integrate with Siri for payments and scheduling, the platform effect takes hold.

The main risk is execution. Apple has a mixed track record with AI features, and agentic systems introduce complexity around privacy, latency, and real-world reliability. If the Siri redesign remains incremental, the revenue estimates become aspirational rather than realistic.

For traders watching the setup, the upgrade provides a valuation floor but not a quick catalyst. Apple’s next earnings report and any AI-related commentary from management will determine whether the $380 target holds or fades.

For more on broader market positioning and rotation risks, see Short-Dated Bond Yield Premium Signals Rotation Risk and other market analysis on AlphaScala. The AAPL stock page tracks live updates on the thesis.