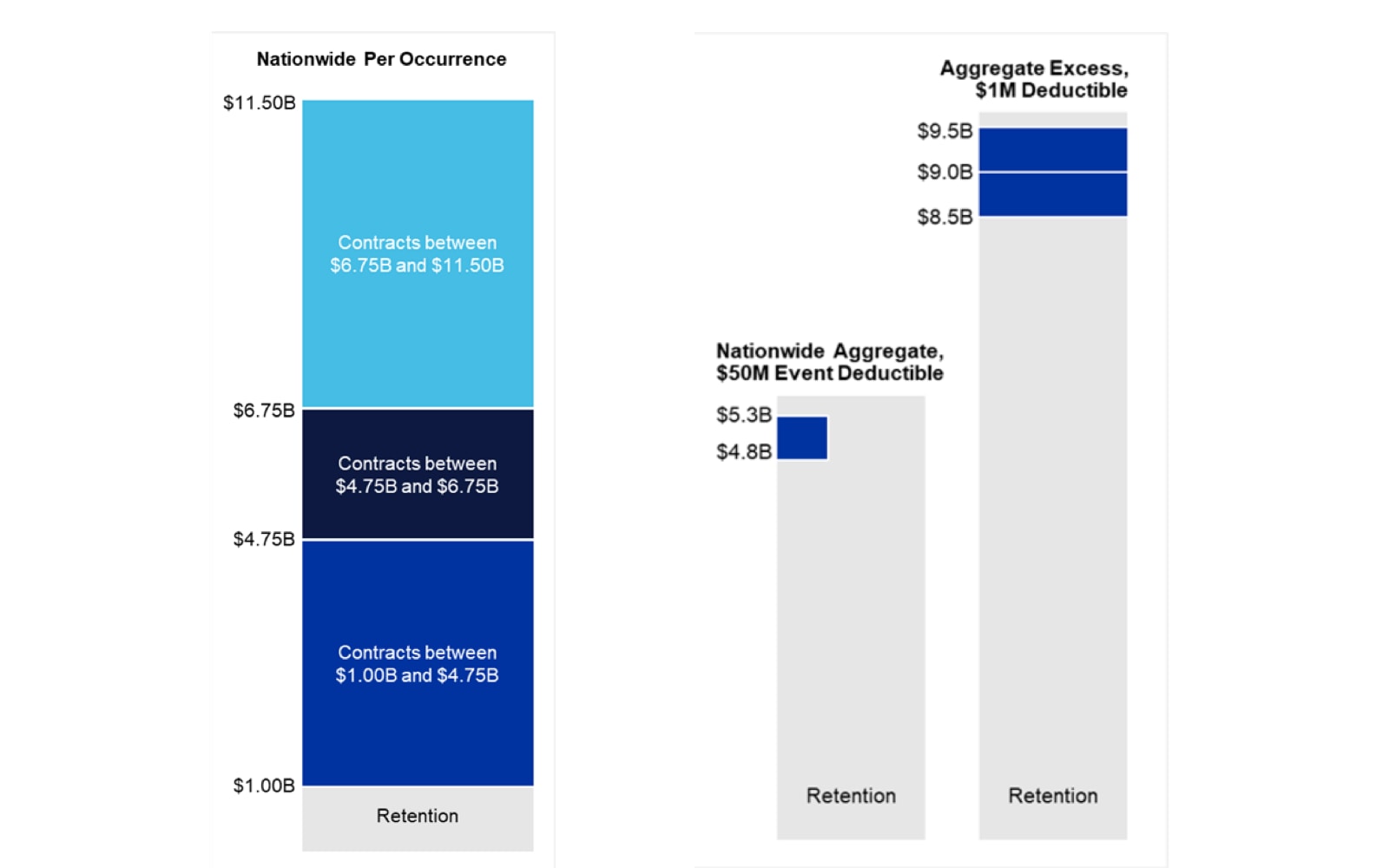

Allstate has expanded its nationwide per-occurrence catastrophe reinsurance tower by $2 billion, a strategic shift designed to provide additional coverage for extreme weather events. This adjustment to the company's risk transfer framework signals a proactive effort to insulate the balance sheet from the increasing volatility associated with large-scale natural disasters. By raising the ceiling on its primary reinsurance coverage, the firm is effectively shifting a larger portion of potential tail risk away from its own capital reserves and toward the reinsurance market.

Structural Changes to Risk Transfer

The expansion of the per-occurrence tower serves as a direct response to the rising frequency and severity of catastrophe losses across the United States. While the company maintains its core underwriting operations, the decision to increase the limit on its nationwide coverage suggests a preference for predictable cost structures over the potential for unhedged earnings volatility. This move complements the insurer's existing aggregate protection layers, which are designed to manage the cumulative impact of smaller, more frequent events throughout the fiscal year.

These adjustments are critical for maintaining underwriting stability in regions prone to significant climate-related claims. By layering this additional protection, the company creates a more robust buffer against the types of events that historically disrupt quarterly performance. The specific calibration of these reinsurance layers reflects a broader industry trend where primary insurers are increasingly reliant on third-party capital to absorb the costs of catastrophic events.

Impact on Financial Stability and Underwriting

The financial implications of this reinsurance expansion are tied to the company's ability to manage its capital position without compromising its competitive standing in the insurance market. By securing higher limits, the firm reduces the probability of a single, massive event forcing a significant capital impairment. This strategy is essential for maintaining consistent credit ratings and ensuring that the company can continue to meet its obligations to policyholders during periods of heightened environmental stress.

AlphaScala currently tracks the performance and risk profile of the insurer. The ALL stock page reflects an Alpha Score of 66/100, categorized as Moderate within the Financials sector. This score accounts for the firm's ongoing efforts to balance premium growth with the necessary costs of risk mitigation and reinsurance.

Future Markers for Capital Allocation

The next concrete marker for investors will be the company's upcoming quarterly earnings report, which will provide insight into the net cost of these reinsurance premiums and their impact on the combined ratio. Market participants should monitor the subsequent filings for details on how these new layers interact with the firm's existing aggregate protection programs. Any further adjustments to the reinsurance tower in the coming months will serve as a bellwether for the company's outlook on catastrophe risk and its appetite for retaining exposure in the current environment. These developments are essential for understanding the broader stock market analysis regarding how major insurers are adapting to the evolving climate risk landscape.