The 20-Year CAGR vs. 42% Hold/Sell: A Contrarian Setup

Apple's compounded annual growth rates over the past 20 years are exceptional. Net income grew at a 26.6% CAGR, revenue at 21.5%, and the share price compounded at 27.7%. That math means the company's market value effectively doubled every 2.6 years for two decades. The stock price line on a logarithmic chart traces that steady ascent, rising alongside earnings multiples that have expanded and contracted cyclically.

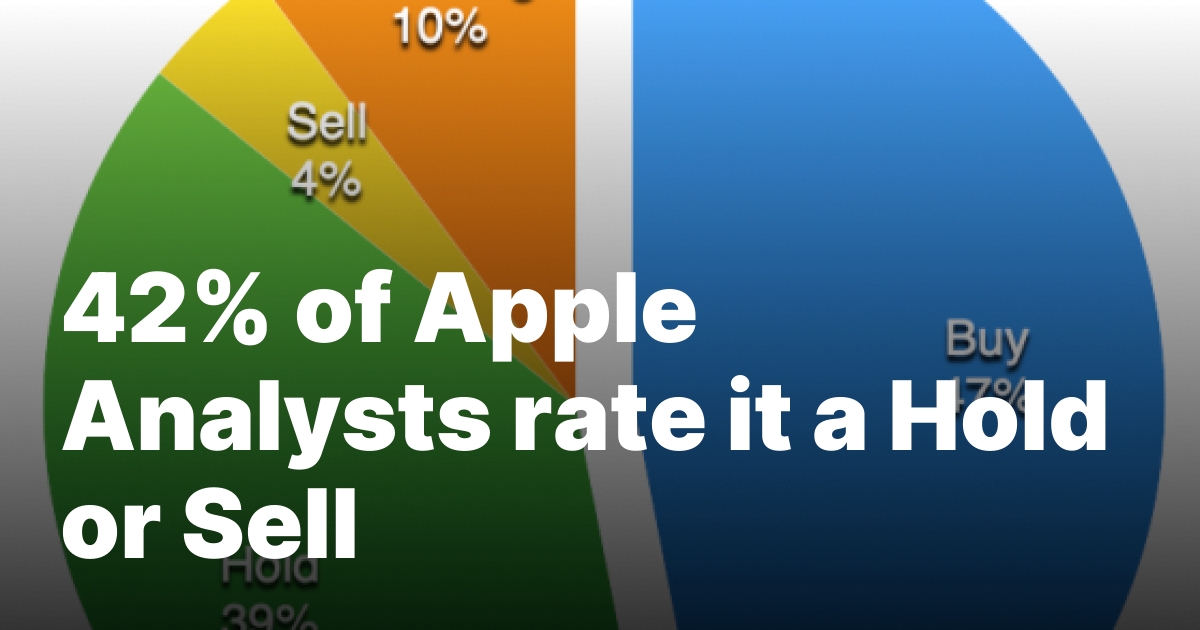

Against that backdrop, analyst ratings tell a different story. According to data from Asymco, 21 out of 49 analysts who cover Apple ($AAPL) have the equivalent of a "Hold" or "Sell" rating. Another five analysts follow the stock without expressing a rating opinion. In other words, more than 42% of sell-side analysts are not recommending a buy on a stock that has appreciated at a 27.7% CAGR for two decades.

The divergence raises a practical question for anyone building a stock market analysis watchlist: is the analyst pessimism a contrarian signal or a correct call on future deceleration?

Key insight: The hold/sell ratio has been rising even as Apple's stock price has climbed, suggesting the market has already priced in the skepticism.

Why the Rising Hold/Sell Ratio Matters More Than the Absolute Number

The source data, published by Asymco, provides a granular look at how these ratings break down. The table below approximates the distribution based on the available facts:

| Rating Category | Number of Analysts | Share of Total |

|---|

| Buy equivalent | 23 | 47% |

| Hold/Sell equivalent | 21 | 43% |

| No opinion | 5 | 10% |

| Total | 49 | 100% |

This breakdown is striking because Apple has rarely operated in a growth-company valuation range that naturally invites hold or sell ratings. The stock has historically been a core holding in many portfolios, and the buy ratio was far higher during earlier product cycles. As the source notes, "It takes significant courage to predict a reversal of a 20 year trend." The implication is that the 42% hold/sell group is betting against the kind of momentum that has rewarded long-term holders for more than a generation.

That line, from the Asymco piece, captures the core tension. The stock's recent ascent is partly fueled by AI optimism, yet the analyst community is more bearish than the price action suggests. The short-term divergence between price momentum and fundamental ratings is a key input for a Apple (AAPL) profile review.

The Mechanism Behind the Divergence

Why would analysts hold or sell a stock that has compounded at nearly 28% annually? The answer lies in the challenge of extrapolation. A 27.7% CAGR over 20 years implies a company that has consistently found new growth vectors – from the iPod to the iPhone to services. Sell-side analysts are rewarded for calling inflection points. The longer a trend runs, the more pressure builds to forecast a reversion.

The rising hold/sell ratio itself is a datapoint. The source includes a chart showing that the percent of Hold, Sell, Underperform, and no-opinion ratings has been trending up over time. That means the analyst community has been gradually shifting away from "Buy" even as the stock continued to climb. The practical takeaway: the market has been climbing a wall of worry built by the very people whose job is to have an opinion on valuation.

The Target Range and What It Suggests About Valuation

The source also provides a graph of analyst price targets, sorted by rating and then value. "Buy" ratings are encapsulated, while other ratings are displayed separately. The red line indicates the average of all ratings. Some targets, especially the lowest ones, are described as out of date.

What this tells the disciplined investor: the dispersion of targets is wide. Some analysts are projecting significant upside, while others see almost no room for appreciation. The out-of-date low targets may reflect stale views that have not been adjusted for the recent AI-driven rally. Even accounting for that, the presence of a large cluster of hold/sell ratings implies that many analysts see limited upside at current levels.

For earnings analysis, this matters because Apple's revenue and net income CAGRs, while impressive, have decelerated in absolute terms as the revenue base grew. A 21.5% revenue CAGR on $25 billion in 2006 is a much smaller dollar number than a 10% growth rate on $400 billion today. The law of large numbers is real, and analysts who are underweighting the stock may be betting that the growth rates continue to shrink.

The AI Catalyst: Confirmation or Noise?

The source specifically points to "optimism around AI" as a recent price driver. Apple's AI strategy, centered on on-device processing and privacy, could unlock a new upgrade cycle. If that thesis plays out, the 42% hold/sell rating would look too conservative, and the stock could re-rate higher.

If the AI cycle disappoints – either because the consumer response is tepid or because competition erodes Apple's premium positioning – then the hold/sell group would appear prescient. The key is that the stock has already moved on the AI narrative. The analyst ratings reflect a skepticism about whether that narrative can sustain the valuation multiple.

What the Earnings Investment Case Must Address

For the earnings analysis archetype, the core question is whether upcoming quarterly results can shift the 42% hold/sell dynamic. The historical trend of rising skepticism means that earnings must deliver not just a beat, a material acceleration or a new product thesis to win back the skeptical analysts.

Three things would confirm a bullish breakout from the current rating setup:

- A reported quarter where services revenue growth exceeds 15% year-over-year, proving the margin story is intact.

- Guidance that implies iPhone unit growth in the next cycle, particularly in Greater China.

- A clear AI monetization path, such as a new subscription tier or recurring revenue from AI features.

Three things would weaken the bull case and validate the hold/sell crowd:

- A quarterly miss in revenue growth below 5% year-over-year, signaling maturity.

- A deteriorating gross margin trend due to higher component costs or AI investments.

- A reduction in the buyback authorization, which has been a key support for EPS growth.

The Post-Print Stock Setup

After the next earnings release, the immediate reaction will depend on whether the numbers beat consensus. The more interesting dynamic is the medium-term shift in analyst ratings. If Apple delivers a beat and raises guidance, some of the hold/sell analysts may upgrade. That would create a positive catalyst chain: better ratings lead to higher target averages, which bring in new buyers.

A miss could accelerate the existing trend, pushing the hold/sell percentage above 50%. That would mark a clear shift in sentiment that could weigh on the stock even if the miss is small.

Final Take for the Watchlist Decision

The disconnect between Apple's 27.7% stock CAGR over 20 years and the 42% hold/sell analyst ratio is one of the more visible contrarian setups in large-cap tech. The source material does not give a definitive view on which side is correct. Instead, it lays out the data and lets the reader draw conclusions.

For a trader or investor building a watchlist, the practical approach is to track the analyst rating distribution over the next two quarters. If the hold/sell ratio drops below 35% without a major price increase, that would suggest the sell-side is capitulating to the trend. If it rises above 50%, the market may be headed for a reassessment.

Either way, the 42% figure is a powerful reminder that even the most consistent compounders eventually face a judgment day from the analyst community. The trading question is not whether the skepticism is right or wrong – it is whether the next catalyst will confirm or contradict the existing divergence.

Watch the next Apple earnings call for signs of AI monetization and services acceleration. Those are the two factors that could close the gap between the stock's track record and its analyst rating profile.