Back to Markets

Stocks● Neutral

Why 75% of AI Deployments Fail and How to Fix It

Enterprise AI spending hits $665B in 2026 with 75% failing. The fix: sell decisions, not engines. How to spot the firms that will survive.

Continue with

Enterprise AI spending will reach roughly $665 billion in 2026. Around three-quarters of those deployments will fail to deliver the return they were funded to produce, according to a recent analysis by Procurement Insights.

The models are better. The tooling is better. The practitioners are more experienced. The failure rate has not moved.

The $665 Billion Failure Signal

That headline figure is not a forecast of growth. It is a measure of capital at risk. The naive read is that AI adoption is accelerating and vendors are capturing a massive total addressable market. The better market read is that most of that spending is being allocated to vendors whose sales approach is structurally misaligned with what buyers actually purchase.

Procurement Insights estimates that 75% of enterprise AI deployments will not produce the expected return. That number has held steady across earlier technology cycles – ERP, e-procurement, digital transformation – despite massive improvements in capability. The constraint is not technical. It is commercial.

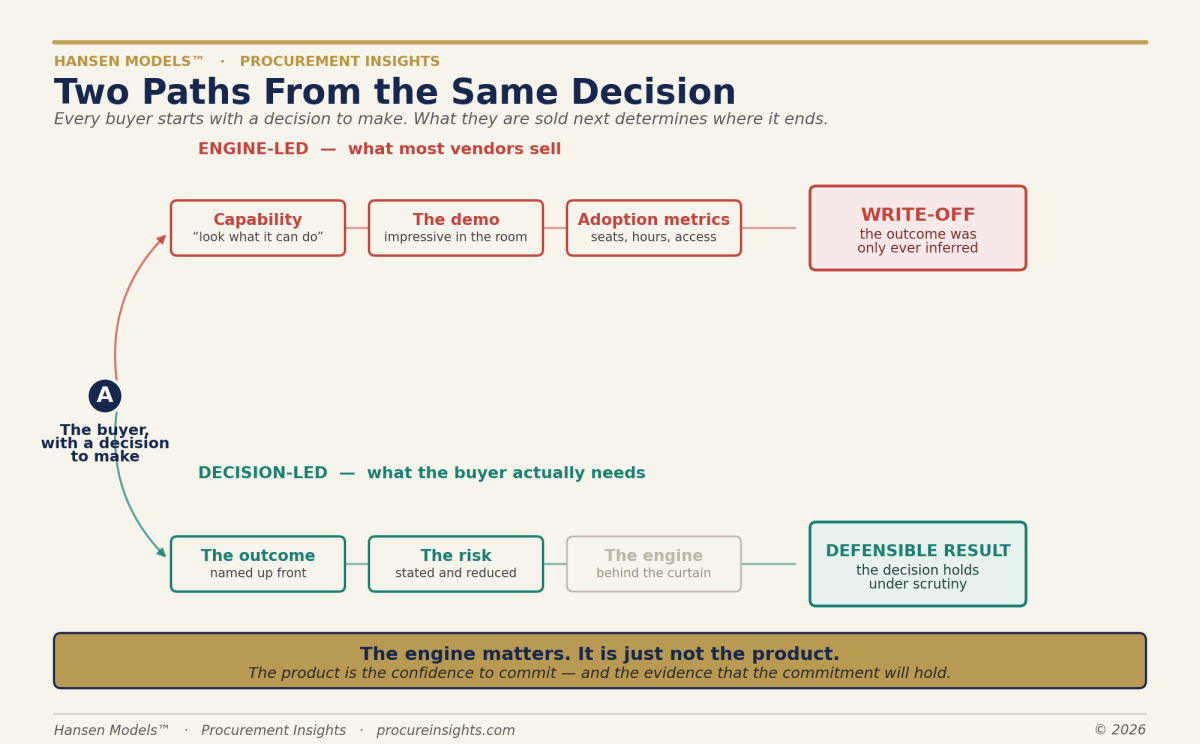

The Engine-versus-Decision Mechanism

Most AI firms lead their sales with capability: the architecture, the model, the mechanism. The buyer is not purchasing the mechanism. The buyer is purchasing the result the mechanism produces, and the confidence that the result will hold.

Consider how established advisory professions handle this. A law firm does not sell its legal-research methodology. A medical specialist does not sell the diagnostic protocol. An investment bank does not sell its discounted-cash-flow models. Each possesses serious proprietary machinery – the machinery stays behind the curtain. The client buys the resolved problem.

The firms that win will be those that lead with the decision and keep the engine behind the curtain. Not because the engine does not matter – it is the entire reason the outcome is reliable – because the buyer does not need to operate the machinery to need what it produces.

Why Capability-Only Sales Are Failing in 2025

There was a window – roughly 2023 to 2024 – when having an AI initiative was itself the value, and a demo that impressed in the room was enough to justify the budget. That window has closed. Having an AI initiative now means nothing. Having a result that holds means everything.

The early measurement habits made the confusion worse. Organizations tracked what was easy to collect and satisfying to report: seats filled, hours logged, access granted. Those numbers describe uptake. They say nothing about whether the AI produced a better outcome than what it replaced. You can hit every adoption metric and still fail, because the organization never absorbed the decisions the engine was supposed to support.

This pattern is not new. Across ERP, e-procurement, digital transformation, and now AI, the pattern has held with remarkable consistency: capability advances, and outcomes lag. If better capability closed the gap, four technology eras of better capability would have closed it. They did not.

The market has quietly inverted the burden of proof. The question is no longer “what can your technology do?” It is “what decision does it let me make with confidence, and can you prove it held?” Firms built to answer the first question are losing to firms built to answer the second.