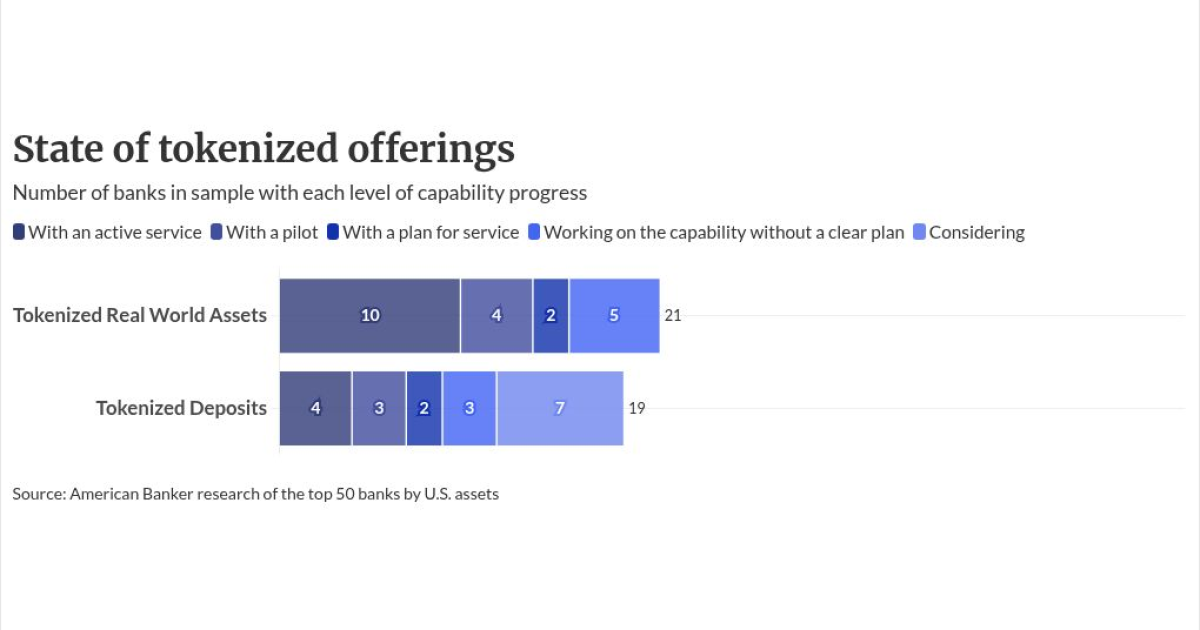

Tokenization is not a theoretical future. BlackRock launched the BUIDL fund, a tokenized Treasury money market fund, in 2024 and it became the largest of its kind within months. JPMorgan's Onyx platform has processed hundreds of billions of dollars in blockchain-based repo transactions. The Federal Reserve Bank of New York, alongside Swift and several large banks, completed a proof of concept settling cross-border U.S. dollar transactions on a shared ledger.

The infrastructure exists. The question is where the rules that govern it will be written.

Europe, Singapore, and the UAE are moving deliberately. They are drafting frameworks for tokenized securities, stablecoins, and digital asset custody. The U.S. capital markets, still the deepest and most liquid in the world, face regulatory uncertainty that pushes development elsewhere.

The debate centers on how securities law applies to blockchain networks. Citadel Securities submitted a proposal to the SEC arguing that public, permissionless blockchain rails should be regulated as financial intermediaries. The Blockchain Association filed a response arguing that treating validators and smart contracts as intermediaries is legally misapplied and practically damaging.

Securities laws regulate intermediaries because they hold custody, exercise discretion, and control user assets. Validators, autonomous smart contracts, and noncustodial software do none of those things. Extending intermediary regulation to neutral infrastructure would impose compliance obligations on systems that have no mechanism to meet them.

The SEC already has tools that could provide clarity. Exemptive relief, no-action letters, and iterative pathways have been used before. The shift from floor trading to electronic markets in the 1990s did not require new laws. The SEC used no-action letters to allow electronic communication networks to operate. The move from paper settlement to electronic clearing followed a similar path.

The same pattern could work for tokenization. The assets themselves do not change. A tokenized Treasury bond is still a Treasury bond. A tokenized share of a real estate fund is still a share of a real estate fund. The rails change. The risk is that regulators apply old categories to new infrastructure without understanding how that infrastructure actually functions.

The cost of inaction compounds. Each month of regulatory ambiguity is another month for projects to launch in jurisdictions with clear rules. Singapore's Monetary Authority has licensed several digital asset platforms. The UAE's Abu Dhabi Global Market has a comprehensive framework for tokenized securities. Europe's Markets in Crypto-Assets regulation provides a baseline.

What would reduce the risk: The SEC issues exemptive relief or a no-action letter for a tokenized fund or secondary market, setting a precedent. The Fed's proof of concept shows regulators can be involved directly. A clear signal that neutral blockchain infrastructure is not an intermediary would keep development onshore.

What would increase the risk: The SEC or Congress adopts the Citadel framework, treating validators and smart contracts as intermediaries. That would make the U.S. functionally hostile to tokenized markets. Projects would have no compliant path forward within U.S. borders.

Tokenization records traditional assets on blockchain networks, making transfer and settlement programmable. Settlement windows, batch processing, and siloed databases are the legacy. Shared ledgers can reduce delays, cut reconciliation costs, and automate compliance. The Fed's proof of concept settled cross-border USD transactions in near-real time. The banks involved confirmed the results. Regulators were in the loop.

The tools to provide clarity exist. The question is whether Washington uses them before the next generation of market infrastructure finds its home elsewhere.