Back to Markets

Commodities● Neutral

Trump's Beef, Gas Orders: An Inflation Risk Event for Commodities

The US cattle herd is at a 75-year low. Trump's orders suspend tariff-rate quotas, while a gas tax holiday faces 25% odds of passing Congress.

Continue with

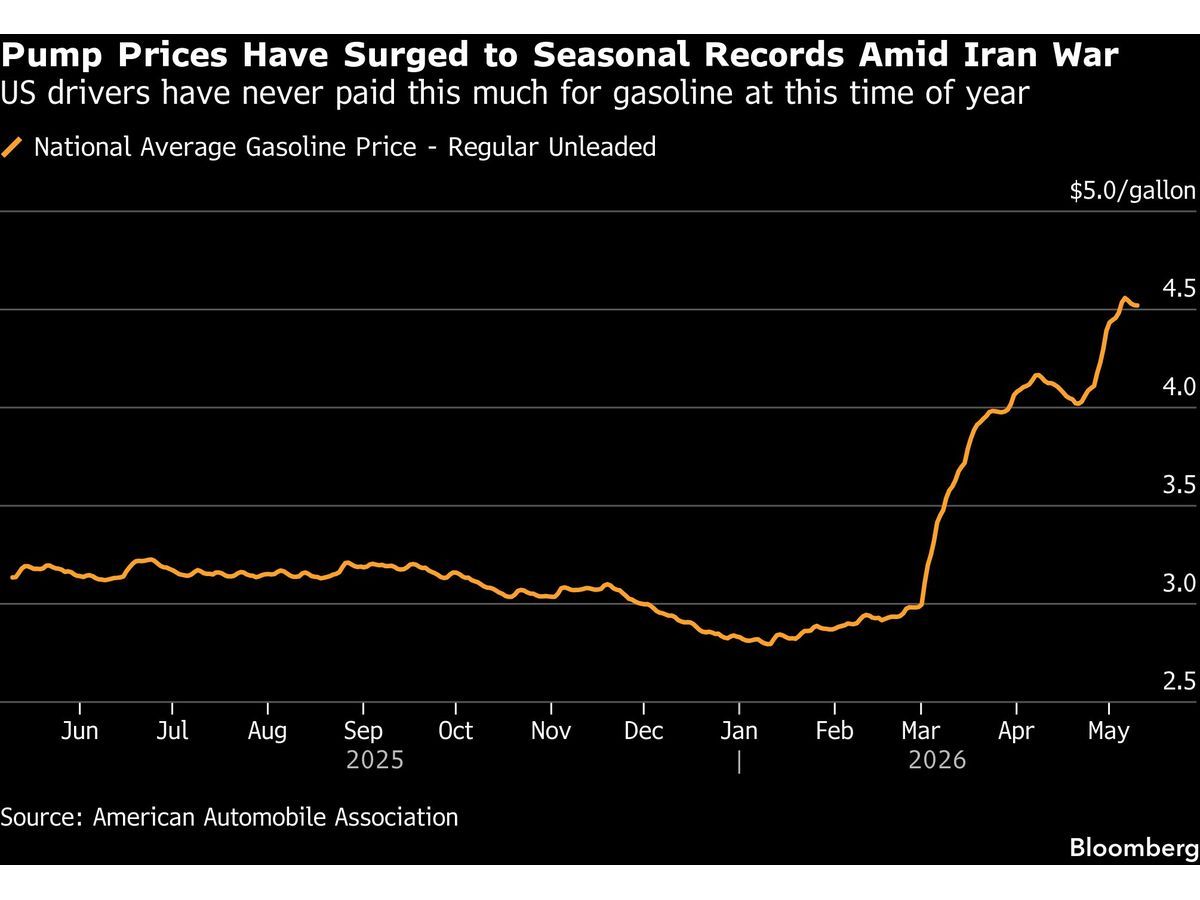

President Trump is poised to sign executive orders Monday targeting beef prices and is pushing for a gasoline-tax holiday ahead of a Tuesday inflation report that economists expect to show sharply higher consumer prices. The dual intervention arrives as the US cattle herd sits at a 75-year low and pump prices remain a political flashpoint ahead of November’s congressional elections.

The simple market read – that executive actions and proposed tax relief will quickly lower food and fuel costs – ignores the mechanisms that determine whether these measures actually flow through to consumers and what they do to the commodity supply chains that underpin those retail prices.

The Executive Orders: Beef Tariff-Rate Quota Suspension

The White House official said the orders aim to address short-term supply issues by expanding imports and supporting a rebuild of the domestic cattle herd. The measure would suspend the annual tariff-rate quota on all beef-exporting nations, according to the Wall Street Journal, citing people familiar with the matter. Under the current system, a certain volume of beef imports enters at a low tariff; beyond that, a higher rate applies. Suspending the quota allows more meat to enter at low rates, effectively bypassing the protective wall for domestic producers.

The US cattle herd has shrunk to a 75-year low, sending consumer beef prices to record highs while tightening margins for meat processors. The immediate commodity exposure sits in live cattle futures (LE) and the cash beef market. More imported product competes with domestic fed cattle, potentially pulling down wholesale beef prices. The domestic herd is not rebuilt overnight. The White House acknowledged the orders also aim to support a herd rebuild. That process plays out over multiple seasons. In the short term, the import relief could reduce the pressure on packers – the same packers President Trump has blamed for high prices and that the Justice Department is investigating for antitrust behavior. Those processors, losing money on tight supplies, might see margin relief if they can source cheaper imported product. The antitrust scrutiny adds a layer of uncertainty, however, because any enforcement action could disrupt how processors commit to forward supply.

The cost of beef has been a key driver of food inflation, making it a political flashpoint. Trump has blamed meatpackers, particularly foreign-owned firms, and the Justice Department probe keeps the political risk baked into the protein supply chain.

Gas Tax Holiday: A 25% Probability Play

Trump told reporters he’ll seek to suspend the federal 18.4 cents-a-gallon tax on gasoline “until it’s appropriate.” Senator Josh Hawley later said he would introduce legislation to suspend the gasoline tax and the 24.4-cent tax on diesel. The tax holiday requires an act of Congress. Rapidan Energy Group, a Washington consulting firm, put the odds of success at 25%.

The direct commodity exposure sits in RBOB gasoline (RB) and ULSD diesel (HO) futures. The federal excise taxes are applied per gallon, and a suspension would mechanically lower the price consumers pay at the station – if refiners and retailers pass the full cut through. When supply is tight, the incidence of a tax cut can be shared between producers and consumers, muting the headline relief. A diesel tax suspension would reduce costs for farmers and truckers, potentially moderating food distribution costs.

The better market read is that a gas tax holiday serves as a political signal rather than a lasting supply or demand solution. The low probability reflects the legislative jam in a divided Congress. Even if the bill gains traction, the diesel component appeals to farm-state interests, which could broaden support. The White House’s scramble for answers on rising electricity bills and pump prices ahead of midterms points to a reactive policy posture that can inject noise into energy markets.