A meeting between President Donald Trump and China's Xi Jinping on May 14-15 is the next live risk event for Chinese equities. The base case from sell-side desks is that tariffs stay where they are without a new escalation, but a JPMorgan estimate puts the effective US levy on Chinese goods at roughly 22%. That number is already priced, but what traders are repricing now is the probability of waivers, a dollar that has softened enough to let the yuan breathe, and whether the two leaders signal any path off the Iran-linked friction that has crept into the bilateral setup. The simple read is that no new tariffs equals a relief rally. The better read is that a sum of small, structural concessions from both sides is what would actually narrow the risk premium embedded in Chinese equities, which have lagged regional peers even as broader Asia rallied last month on easing Iran war fears.

Markets are not pricing a grand trade deal. Macquarie Group's base case is tariffs stay in place without meaningful escalation. That alone does not unlock a sustained rerating. The mechanics that matter are: first, whether the meeting produces any concrete easing of US curbs on tech exports to China, which would hit semiconductor and hardware names directly; and second, whether the conversation over Iran reduces the secondary sanctions risk that has been attaching to Chinese refiners and trade intermediaries. Both are moving parts in the supply chain that set the floor for exporter multiples.

The Tariff Overhang: A 22% Floor That Caps Gains

The effective US tariff rate on Chinese goods sits near 22%, per a JPMorgan Chase estimate. The bank's proprietary Alpha Score, a blended quantitative and fundamental signal, registers 49 out of 100, labelled Mixed, with shares trading at $302.10, down 1.36% on the day. That mixed signal aligns with the interpretation many macro desks are applying to the summit: no single catalyst is likely to swing the rate itself, but even a marginal reduction in uncertainty about additional levies can compress the risk premium that has made Chinese stocks cheap relative to earnings growth.

Eugene Hsiao, head of China equity strategy at Macquarie in Hong Kong, frames the tariff base case as one that "marginally improves visibility for broader China exporters by easing escalation risk and providing better supply-chain certainty, even as existing tariffs continue to cap upside." The mechanism is straightforward: exporters have already adjusted sourcing and routing to absorb a low-20% tariff. What hurts incremental investment and hiring decisions is the tail risk of a jump to 30% or 40% that gets surfaced during periods of heightened US-China rhetoric. If the summit removes that tail, forward earnings estimates for the exporter basket become less volatile, and multiples can grind a little higher.

The yuan is the other channel. As the dollar has retreated, optimism over a stronger renminbi has built. A stable to firmer yuan reduces the cost of servicing dollar-denominated input contracts for Chinese manufacturers and simultaneously makes Chinese equities more attractive to foreign investors who hedge currency. Any communique that even hints at a currency understanding–not a Plaza Accord repeat, but a reaffirmation of existing G20 commitments–would be read as a positive by the equity market.

Biotech and Tech Supply Chains: Who Gets a Waiver

Tariff escalation risk is not evenly distributed. Hsiao notes that companies tied to energy security or the global tech supply chain are likely to receive waivers or be carved out from any new levies. That set includes semiconductor packaging firms and some clean-energy component makers. The logic is that restarting tariff fights on those segments would immediately backfire on US manufacturing costs and on the administration's own industrial policy goals.

In contrast, biotech firms with significant US revenue exposure sit in a much more vulnerable position. WuXi Biologics (Cayman) Inc. and WuXi AppTec Co. are already under pressure from the Biosecure Act, which targets Chinese biotech companies on national security grounds. Additional tariffs on pharma intermediates or finished therapies would compound the legislative overhang and shrink the margin of safety that US pharma partners have been pricing in. For traders, the WuXi names are a real-time barometer: if they rally into the summit, it signals that the market believes biotech will escape further punitive measures; if they sell off, the headline risk is being taken seriously.

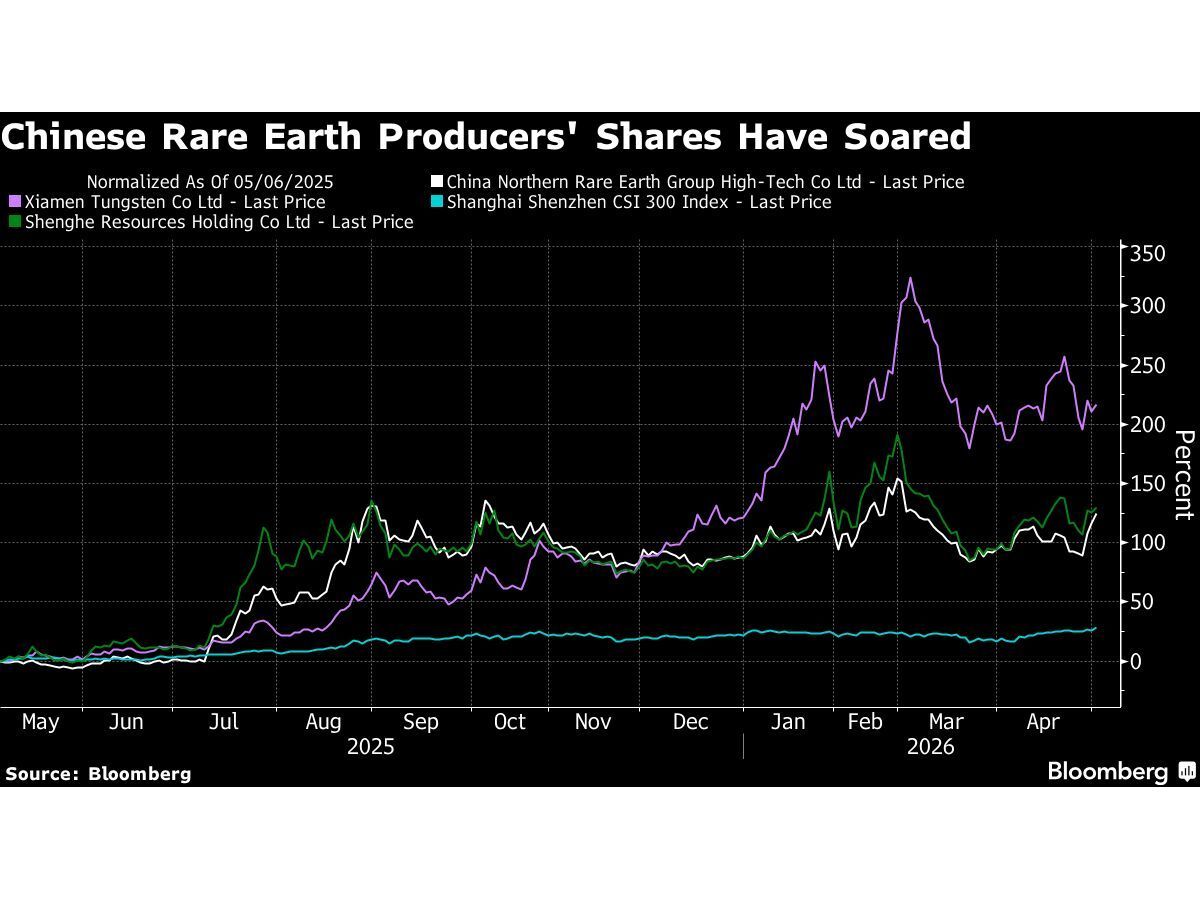

The tech export curb side is tied to a broader debate about US chip equipment and AI accelerator access. Even a non-binding signal from Xi that China will respond to US export controls with restraint rather than escalating its own restrictions on rare earths would be enough to lift the hardware sector. Conversely, a US statement that export controls will be tightened further–unlikely but not impossible if the summit turns confrontational–would hit the Shanghai and Shenzhen tech boards first, with ripple effects into South Korea and Taiwan suppliers.

Iran: The Other War That Could Reroute Sentiment

The Iran war adds a layer of strain that did not exist at prior Trump-Xi meetings. Washington's efforts to tighten pressure on Tehran are increasingly affecting China, which remains Iran's largest trading partner and a major buyer of its crude exports. The US has already sanctioned Chinese refiners that process Iranian oil, and any signal from Trump that he is willing to link progress on Iran with trade concessions–or the opposite, that China's Iran purchases will be treated as a violation–can trigger sharp moves in the energy-heavy Shanghai index and in the yuan.

Trump has said he will discuss the Iran war with Xi during the summit. If the readout includes language that suggests China will cooperate on enforcing sanctions, even in a limited way, the market will interpret it as a reduction in secondary sanctions risk for Chinese banks and commodity traders. That would lift the entire China financials sector, which has been heavily discounted because of fears that US Treasury could block dollar clearing access for institutions that facilitate Iran-linked trade. On the other hand, a Chinese refusal to budge that is met with a US threat to designate additional entities would immediately revive volatility in the onshore equity market and push the yuan weaker.

Analysts note that prior Trump-Xi meetings have often triggered sharp swings in Chinese shares, not because of the formal communique but because of off-the-record briefings and unilateral tweets in the 24 to 48 hours after the summit. That pattern means the real risk management window extends from May 14 through May 17, and traders who buy the initial relief headline without hedging gamma risk in the subsequent sessions have historically been forced out of positions.

JPMorgan's Mixed Alpha Score and the Rate Estimate

JPMorgan Chase itself, with an Alpha Score of 49 and a Mixed label, is not a clean directional read on the summit outcome, but the bank's 22% effective tariff estimate is the reference point most institutional accounts are using to calibrate exporter exposure. The stock's -1.36% move today is coincident with broad financial sector weakness and does not reflect any unique summit-related position. Still, the estimate provides a hard number for a market that often trades on vague perceptions of "high tariffs." When every percentage point of effective rate translates into roughly 0.4 percentage points of GDP drag for China's export sector, the difference between the 22% status quo and a hypothetical 15% rate–if talks produce real tariff rollback, which no one expects–would be enough to justify a 5% to 7% rerating in the exporter basket. That math is sitting on every macro trader's sheet.

"If the summit can bring a little bit more certainty to the US-China relationship and drive that risk premium down, that's ultimately going to be very positive for Chinese equities," said Christopher Hamilton, head of client solutions for Asia Pacific ex-Japan at Invesco Ltd.

Hamilton's point is that the risk premium itself is the tradeable variable. The 22% tariff is known. The uncertainty around whether it jumps to 30%, or around whether secondary sanctions escalate, is what keeps Chinese equities trading at a structural discount to their Asian peers. Removing even half of that uncertainty, without a single tariff reduction, adds to the net present value of the earnings stream.

What Would Confirm a Détente–and What Would Unravel It

To avoid chasing a shallow headline bounce, traders need a checklist of concrete markers that would confirm the summit is delivering a genuine reduction in friction. The first marker is language in the joint statement or post-summit readout that commits to a framework for export control discussions. Even a working group announcement, without immediate deliverables, shifts the policy process from unilateral action to a negotiated timeline.

The second marker is any easing of the Biosecure Act enforcement timeline or a signal that biotech tariffs will not be layered on top of existing legislative restrictions. WuXi AppTec call option activity and block trade pricing in the days after the summit will be the cleanest real-time indicator of whether that has occurred.

The third marker is oil market reaction to any Iran-related language. A decline in Brent crude on the expectation that China will reduce Iranian imports would lift refinery margins in China and, perversely, be positive for Chinese energy stocks despite the headline "concession" optics.

What would unravel the constructive setup is simple: a tweet from Trump, within 48 hours of the summit's close, that either raises the tariff threat level or explicitly calls out Chinese banks for sanctions evasion. That sequence would not only reverse any equity gains but likely push the yuan through the 7.30 level, triggering a fresh round of capital outflow restrictions that would damage the investability thesis for foreign portfolio flows.

Chinese equities are sitting on a low base of expectations. The regional lag means that any outcome short of a direct confrontation will probably produce a tactical bid. But the difference between a tradeable bounce and a durable move higher rests on whether policymakers address the structural supply-chain risk that a 22% tariff rate represents, and whether the Iran dimension gets woven into the trade narrative or hived off as a separate, manageable dispute. The summit itself is a catalyst; the follow-through, not the first headline, is what will determine position sizing.