Stocks● Neutral

ZSP.TO Tax Reporting Error: Why Five Entries Appear on T3s

Investors face reconciliation hurdles as BMO S&P 500 ETF reports five distributions despite four cash payments. Verify T3 slips to avoid potential tax liabilities.

Continue with

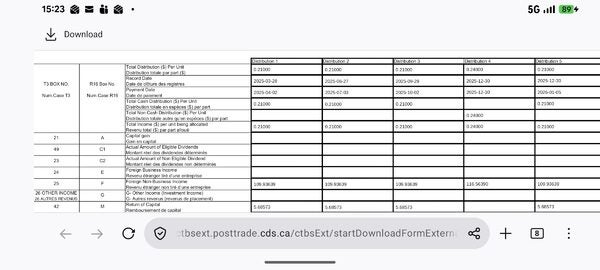

A recurring discrepancy in the 2025 T3 tax reporting for the BMO S&P 500 Index ETF (ZSP.TO) has surfaced, with investors reporting five distinct distribution entries on tax summaries despite receiving only four cash payments throughout the fiscal year. This administrative misalignment creates immediate friction for retail holders attempting to reconcile their investment income against official tax documentation provided by financial institutions.

Reconciliation Challenges for ZSP.TO Holders

The core issue stems from the divergence between actual cash flow events and the tax reporting structure applied to the ETF. Investors typically track distributions based on the four quarterly cash payments deposited into their accounts. When a T3 summary lists five entries, it often indicates an accounting adjustment, a phantom distribution, or a reclassification of income that does not correspond to a direct cash event for the shareholder. This creates a reporting burden where the investor must verify whether the fifth entry represents a non-cash reinvestment or a correction of prior-period data.

For those managing portfolios across multiple institutions, the inconsistency complicates the aggregation of tax data. Because the discrepancy appears across different brokerage platforms, the issue likely originates at the fund provider level or within the data transmission process to tax authorities. Investors are currently tasked with verifying whether these entries reflect taxable income that was never realized as cash or if they represent a reporting error that requires a corrected T3 slip.