Stocks● Neutral

Snowline Gold Secures $100M Funding for 2026 Exploration

Snowline Gold has locked in $100M for its 2026 field season, targeting the Valley gold deposit and a 10,000-metre drill program to hit a 2027 PFS deadline.

Continue with

Snowline Gold Corp. (TSX: SGD) has confirmed that its 2026 field season is fully funded, backed by a cash balance of approximately $100 million. This liquidity position allows the company to accelerate development at its flagship Rogue Project, specifically targeting the Valley gold deposit. By securing this capital, the company aims to bypass common financing hurdles that often stall junior mining projects during the pre-feasibility stage.

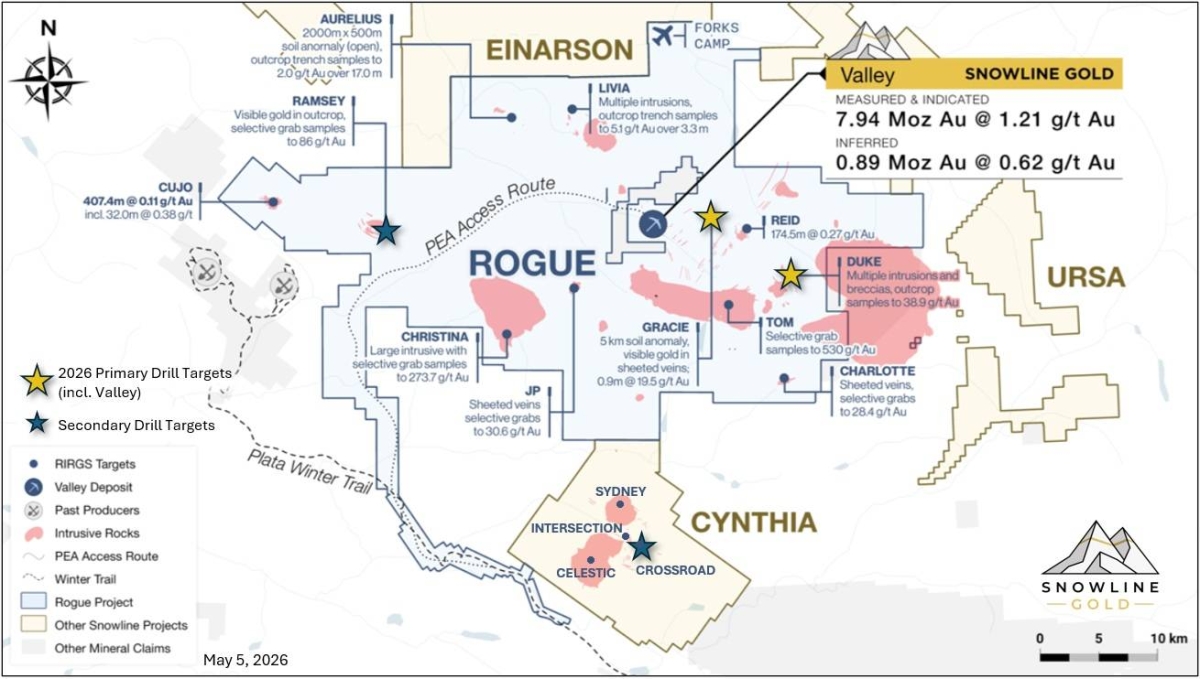

Advancing the Valley Gold Deposit

The primary objective for the 2026 season is the advancement of the Valley deposit to provide the necessary data for upcoming economic studies. The company is currently mobilizing its largest field team to date, with drilling operations scheduled to begin in mid-May. This operational scale is intended to streamline the permitting process and provide a clearer path toward the Pre-Feasibility Study (PFS), which remains on schedule for completion by early 2027.

Beyond the primary deposit, the company has committed to an extensive regional exploration program. This includes over 10,000 metres of planned drilling, which will focus on both the expansion of the Valley deposit and the testing of high-priority regional targets. For investors, this represents a shift from initial discovery phases toward resource definition and economic validation.