The recent surge in portfolio valuations, characterized by the author as a "rocket" return, highlights a recurring tension between passive index-tracking strategies and the reality of sector-specific volatility. While the author reported a Financial Freedom (FF) portfolio value of £389,242.68 at the end of April 2026, the underlying mechanism driving these gains appears to be a concentration in energy-heavy index trackers. This serves as a practical reminder that when broad market indices rally, the performance is often decoupled from individual savings rates and instead tethered to the cyclical nature of oil and gas equities.

The Energy Sector Read-Through

For investors tracking their own progress against broader benchmarks, the author's experience underscores the danger of assuming that portfolio growth is purely a function of disciplined capital allocation. When index trackers outperform, it is frequently due to a heavy weighting in energy companies, which have recently benefited from supply-side constraints and price volatility. If an investor's portfolio is heavily tilted toward these sectors, the "rocket" effect is less a sign of market-wide health and more a reflection of specific commodity price sensitivity.

This creates a divergence between the investor's goal of consistent, long-term wealth accumulation and the erratic nature of the energy sector. As the author noted, the rapid gains seen in early 2026 have induced a sense of unease. This skepticism is well-founded; when growth is driven by a single sector, the probability of a sharp reversal increases. Investors should distinguish between gains derived from compounding dividends and those derived from temporary sector-specific tailwinds.

Capital Allocation and Dividend Reinvestment

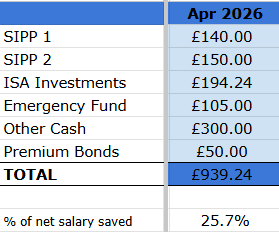

With a savings rate of 25.7% of net salary, the author’s strategy relies on the consistent reinvestment of dividends to reach a new target of £6,000 in annual passive income. The receipt of £541.58 in dividends—split between ISAs and SIPPs—highlights the importance of tax-advantaged accounts in the FIRE (Financial Independence, Retire Early) framework. By reinvesting these payouts, the author effectively lowers their cost basis and accelerates the compounding effect, regardless of the current market valuation of the underlying index trackers.

However, the reliance on dividend income as a primary milestone requires a clear-eyed view of corporate payout policies. If the energy companies currently propping up the index trackers were to face a downturn, the dividend yield could compress, potentially spoiling the "bumper" months the author anticipates. For those building a portfolio, the lesson is to ensure that dividend income is diversified across sectors rather than concentrated in the same energy-heavy vehicles that are currently driving capital appreciation.

Practical Framework for Portfolio Monitoring

Evaluating a portfolio's health requires more than just checking the total value at the end of the month. Investors should categorize their holdings to understand which sectors are contributing to the current volatility. If a portfolio is heavily exposed to energy, it is essential to stress-test the impact of a 10% to 20% decline in oil prices on both the total portfolio value and the expected dividend yield.

For those interested in how different sectors behave under current market conditions, reviewing stock market analysis can provide context on whether a portfolio's growth is sustainable or merely a byproduct of a temporary sector rotation. The author's decision to increase their savings rate following a performance-based pay rise is a sound tactical move, as it increases the "dry powder" available to buy into dips, effectively hedging against the risk of a market correction.

Evaluating the FIRE Mindset

The author’s interaction at a Manchester FIRE meet-up serves as a proxy for the broader market sentiment. The skepticism encountered from a non-believer—who questioned the utility of saving for a retirement that might never arrive—is a common psychological hurdle for long-term investors. This "what if you die?" argument is the ultimate test of an investor's conviction.

From a practical standpoint, the FIRE philosophy is not about denying the present but about managing the risk of future insolvency. By maintaining a high savings rate and focusing on dividend growth, the investor creates a buffer against both market volatility and personal life events. The author’s commitment to increasing their dividend goal to £6,000 per year is a shift toward a more aggressive, income-focused strategy that prioritizes cash flow over pure capital gains. This shift is particularly important for those who, like the author, feel uneasy about the current pace of market appreciation.

When evaluating your own path, consider the following:

- Sector Concentration: Are your gains coming from broad market growth or a single, volatile sector like energy?

- Dividend Sustainability: Is your projected income growth tied to companies with stable payout ratios or cyclical firms that may cut dividends during a downturn?

- Savings Discipline: Does your investment rate increase in lockstep with your income, or is it static?

As the author continues to track their progress, the next concrete marker will be whether the dividend income meets the new £6,000 annual target. If the market experiences a significant correction, the ability to maintain this savings rate will be the primary determinant of whether the FIRE journey remains on track or faces a temporary delay. For those managing their own portfolios, the focus should remain on the consistency of the input—the savings rate—rather than the volatility of the output—the market-driven portfolio value.