Back to Markets

Commodities● Neutral

Why the $505 Billion Bridge Pipeline Faces Margin Risks

Contractors face critical margin compression as raw material costs surge and public budgets tighten. Operational precision will now dictate future winners.

Continue with

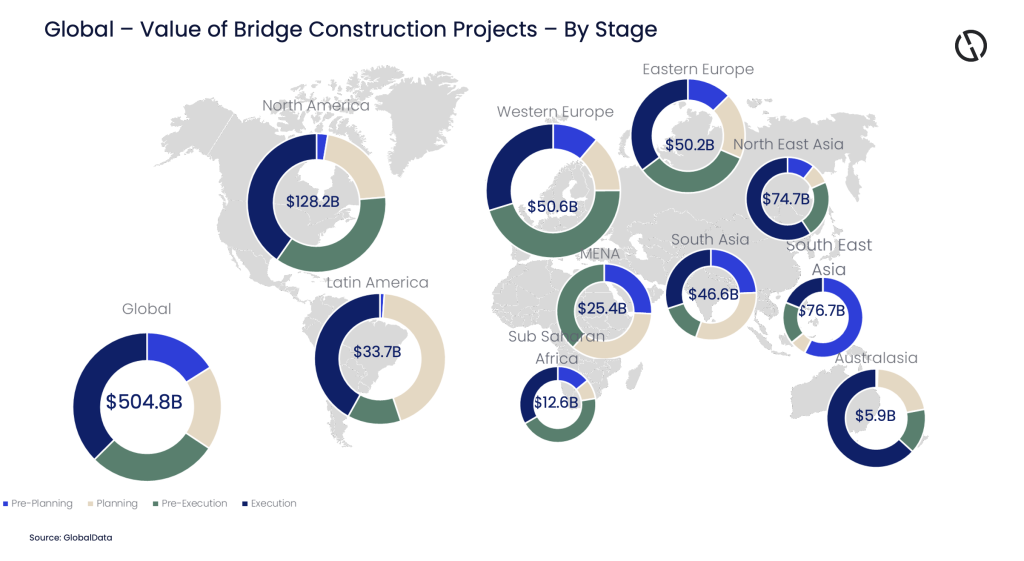

The $505 Billion Pipeline

The global bridge construction sector currently holds a massive $505 billion project pipeline. While the sheer scale of capital investment suggests a period of growth, the reality for contractors is far more complex. Public budgets are under intense pressure, and the cost of raw materials remains unpredictable. These factors are forcing firms to abandon the strategy of chasing low-margin wins in favor of operational precision.

Financial Constraints and Material Costs

Contractors are operating in an environment where public sector spending is no longer guaranteed. Tightening government finances mean that project owners are scrutinizing bids more closely than ever before. When combined with the volatility of steel, concrete, and other essential materials, the risk profile for major infrastructure projects has changed. Firms that cannot manage these price swings effectively are finding their profit margins erased.

"Success will depend less on winning projects and more on delivering them under pressure."

Operational Realities for Contractors

Winning a contract is no longer the finish line. In the current market, the focus has shifted entirely to execution. Projects that were once considered safe bets are now subject to delays and cost overruns if supply chains are not managed with extreme care. Traders and investors tracking the commodities analysis sector should note that the price of raw inputs remains a primary driver of project viability.