Back to Markets

Macro● Neutral

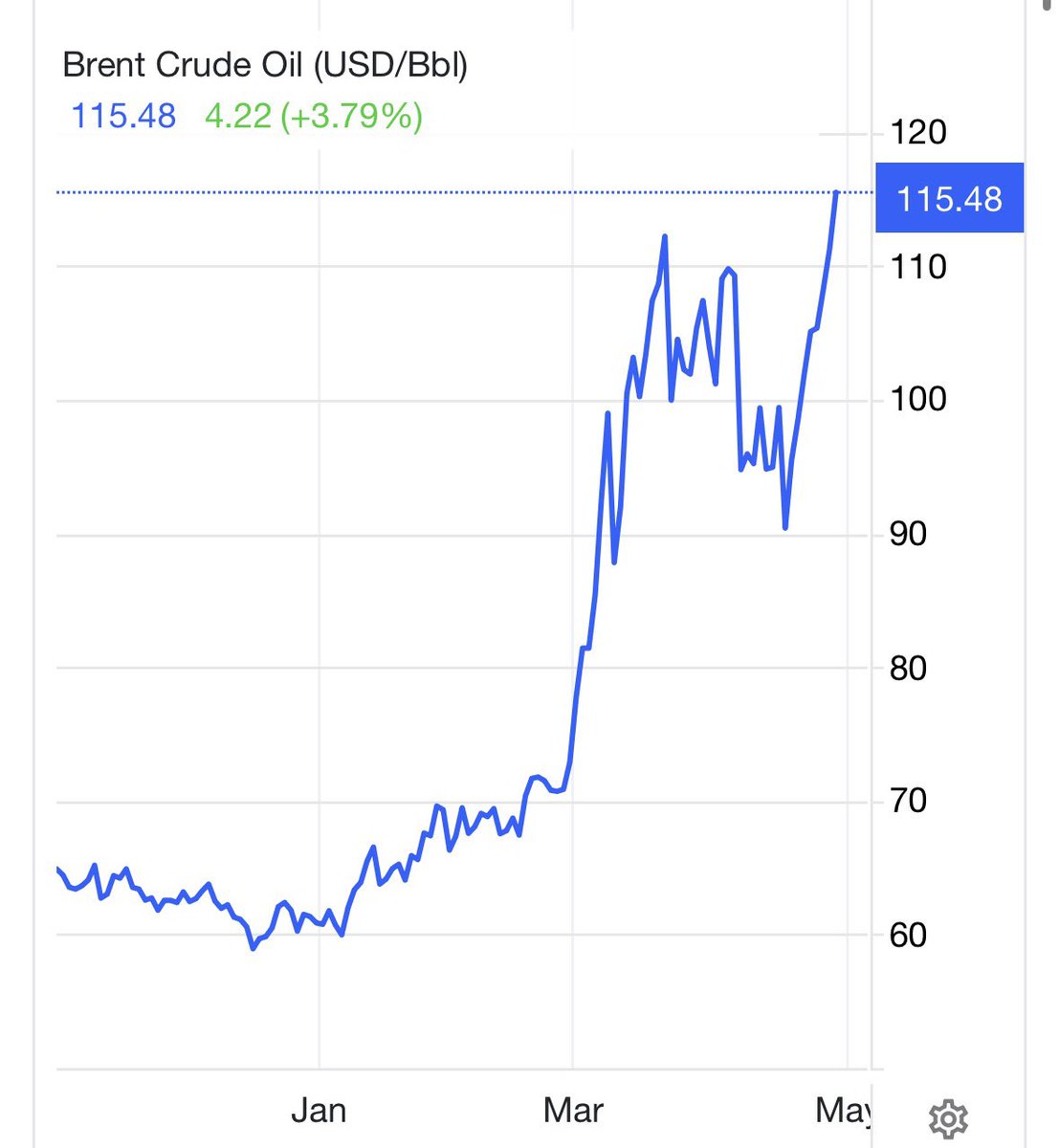

Treasury Debt Shifts Threaten Long-Term Yield Curve Stability

Rising issuance forces a recalibration of term premiums as private markets absorb supply. Watch bid-to-cover ratios in upcoming auctions for rate signals.

Continue with

The recent policy signals from the Treasury Department regarding debt management strategies have introduced a new layer of uncertainty into the long end of the yield curve. By signaling a potential shift in issuance priorities, the administration is forcing a recalibration of term premium expectations. This adjustment occurs against a backdrop of persistent federal deficit spending, which necessitates consistent market absorption of new debt.

Treasury Issuance and Yield Curve Dynamics

The transmission mechanism from Treasury supply to broader market conditions remains tied to the liquidity profile of the primary dealer system. When issuance patterns deviate from established expectations, the immediate impact is often observed in the volatility of the 10-year and 30-year bond yields. As the market digests the potential for increased supply, the cost of capital for private sector borrowers faces upward pressure, independent of the Federal Reserve's benchmark rate path. This dynamic is explored further in Fed Policy Stasis Deepens as Powell Commits to Board Tenure.

Market participants are now evaluating how these issuance shifts interact with the ongoing quantitative tightening process. The reduction of the central bank's balance sheet removes a significant buyer of sovereign debt, leaving the private market to absorb the entirety of the supply. If the Treasury increases the frequency or size of auctions to fund fiscal obligations, the resulting competition for capital can lead to a widening of credit spreads. This environment complicates the outlook for financial institutions, such as those tracked on the ALL stock page, where the Alpha Score currently sits at 69/100.