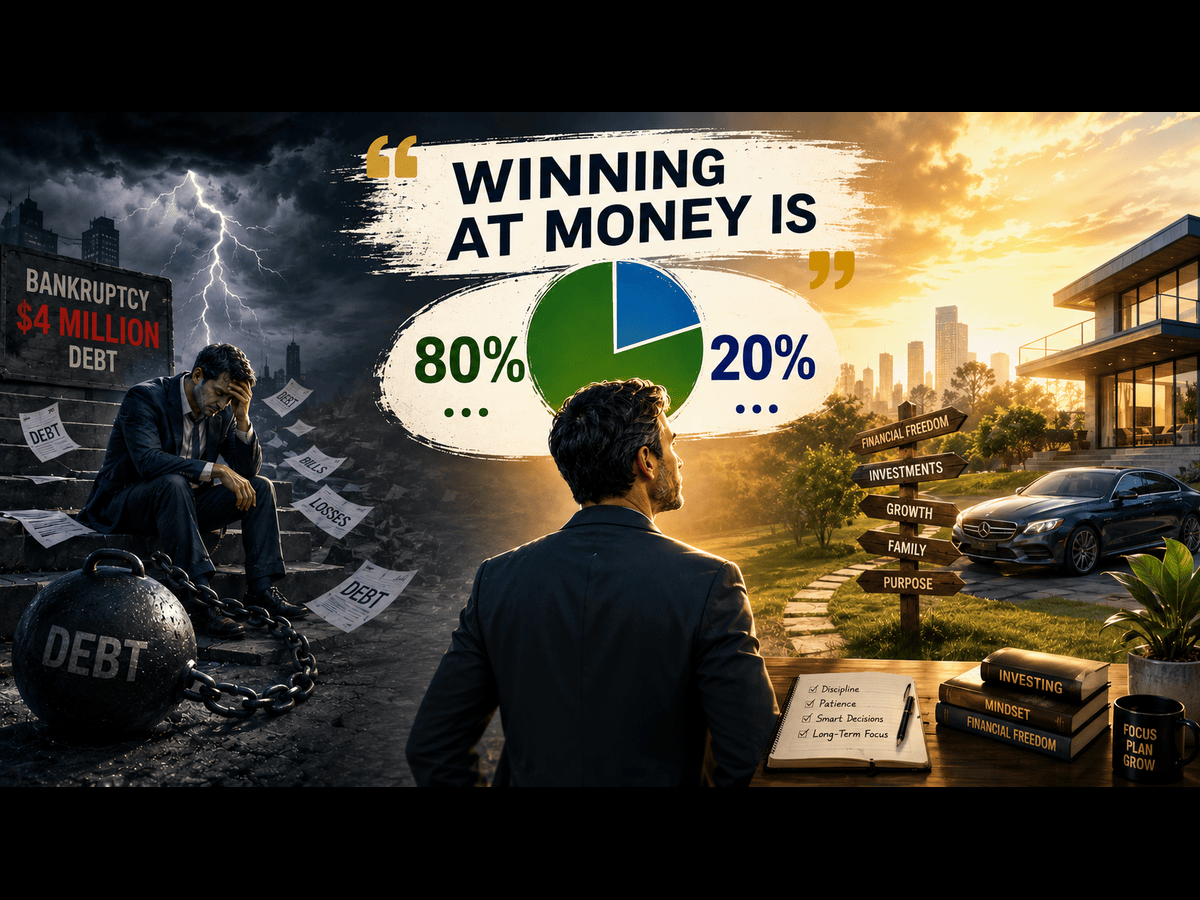

Dave Ramsey built a personal finance empire on the back of a $4 million bankruptcy. The radio host and author turned that failure into a systematic approach to money management he calls the 7 Baby Steps. The core idea: winning with money is 80% behavior and 20% head knowledge. That ratio, drawn from Ramsey's own experience, underpins his insistence on incremental savings and debt payoff.

Ramsey's first step is a $1,000 starter emergency fund. He argues that before any serious investing begins, a household needs a cash buffer against life's surprises. Step two is the debt snowball: list debts from smallest to largest, pay minimums on everything, and throw every extra dollar at the smallest balance. Critics call it mathematically inefficient. Ramsey points to the behavioral wins. A $500 credit card paid off in two months feels like a victory. That momentum keeps people in the game.

Step three pushes the emergency fund to three to six months of expenses. Only then does Ramsey allow investing. Step four is 15% of household income into retirement accounts. Step five is college savings for children. Step six is paying off the mortgage early. Step seven is building wealth and giving.

The sequence matters. Ramsey insists that skipping the emergency fund to invest faster is a trap. The market drops, the car breaks down, and the investor sells at a loss. His framework treats personal finance as a series of gates, not a spreadsheet exercise.

Behavioral finance researchers have found evidence that the snowball method reduces default rates relative to the avalanche method, even though avalanche saves more in interest. The reason is psychological: the quick wins reinforce the habit. Ramsey's insight is that the person in the mirror is the hardest variable to manage.

Applied to the broader market, Ramsey's approach suggests that consumer credit health is a leading indicator for spending. If households follow his steps, credit card balances shrink and saving rates rise. That is good for long-term capital formation. It is bad for short-term consumption. Companies like Apple (AAPL), which rely on discretionary spending, benefit when consumers are debt-free and confident, not when they are stretched.

Ramsey's critics argue that his 8% withdrawal rate assumption in retirement is too aggressive and that his ban on credit cards is impractical for many. The core thesis – that behavior drives financial outcomes more than knowledge – is hard to dispute. He has helped millions of households avoid the bankruptcy he himself once faced.