Stocks● Neutral

Credit Markets Pivot to Risk as Geopolitical Tensions Recede

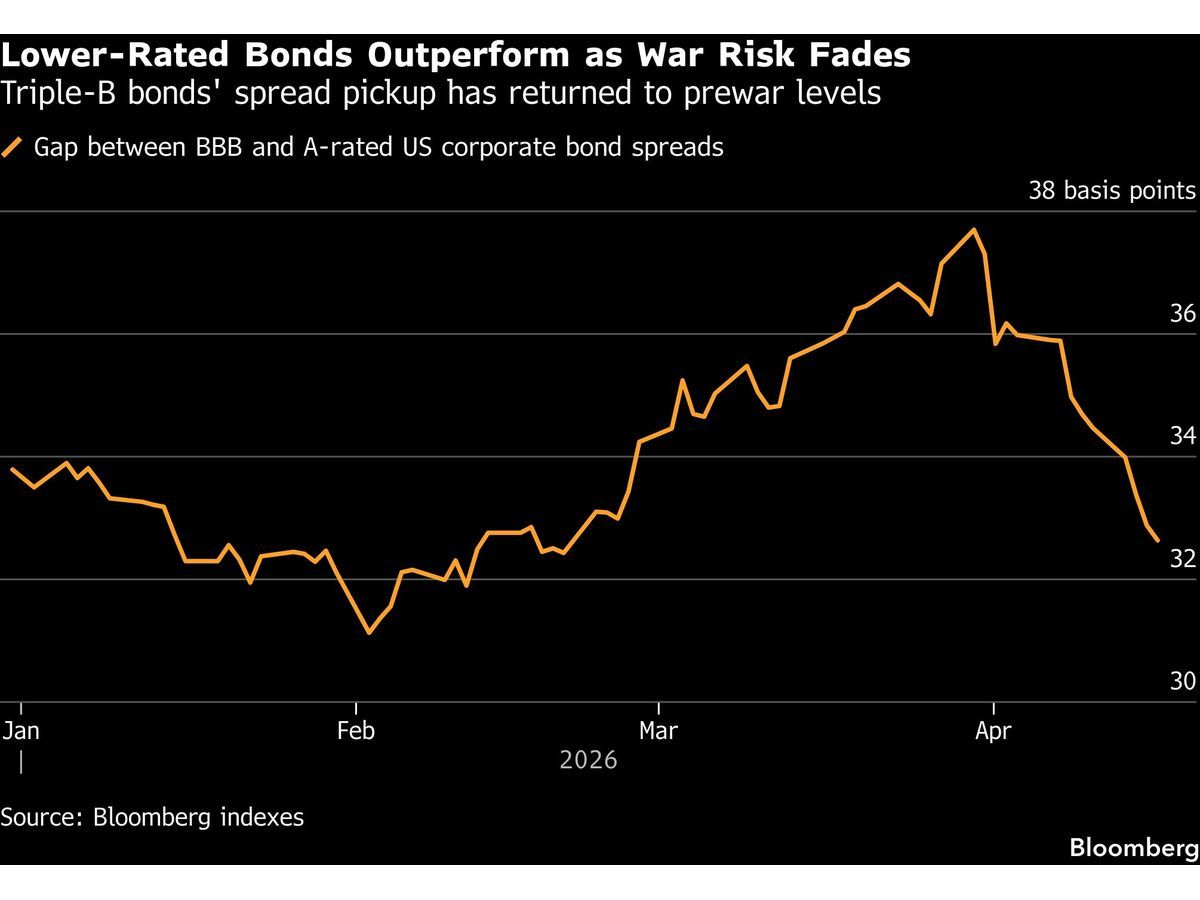

Investors are shedding defensive holdings for higher-yield debt as credit spreads narrow. Watch upcoming corporate debt issuance for signs of a sustained rally.

Continue with

Credit investors are aggressively rotating into riskier debt instruments, signaling a shift in sentiment as the perceived threat of a broader conflict between Iran and the United States recedes. This movement marks a departure from the defensive positioning that defined the previous period, where capital flowed heavily into safe-haven assets. The current appetite for yield suggests that market participants are pricing in a sustained truce, effectively discounting the risk premium that had been attached to credit spreads over the last several weeks.

The Shift in Credit Risk Appetite

The pivot is most visible in the narrowing of spreads across corporate bond markets. Investors are shedding high-grade defensive holdings in favor of lower-rated debt, seeking to capture higher coupons as the urgency for capital preservation wanes. This transition is not merely a tactical adjustment but a broader recalibration of risk-adjusted returns. By moving down the quality spectrum, credit desks are betting that the stabilization of geopolitical conditions will provide a more predictable environment for corporate earnings and debt servicing.

This trend mirrors broader movements in stock market analysis, where equity indices have begun to recover lost ground as the geopolitical overhang lifts. While the credit market often acts as a leading indicator for systemic risk, the current buying activity suggests a high degree of confidence in the durability of the diplomatic pause. The transition from havens to risk-on assets is a direct response to the reduced likelihood of a supply-chain disruption or a sudden spike in energy costs that would have otherwise pressured corporate balance sheets.