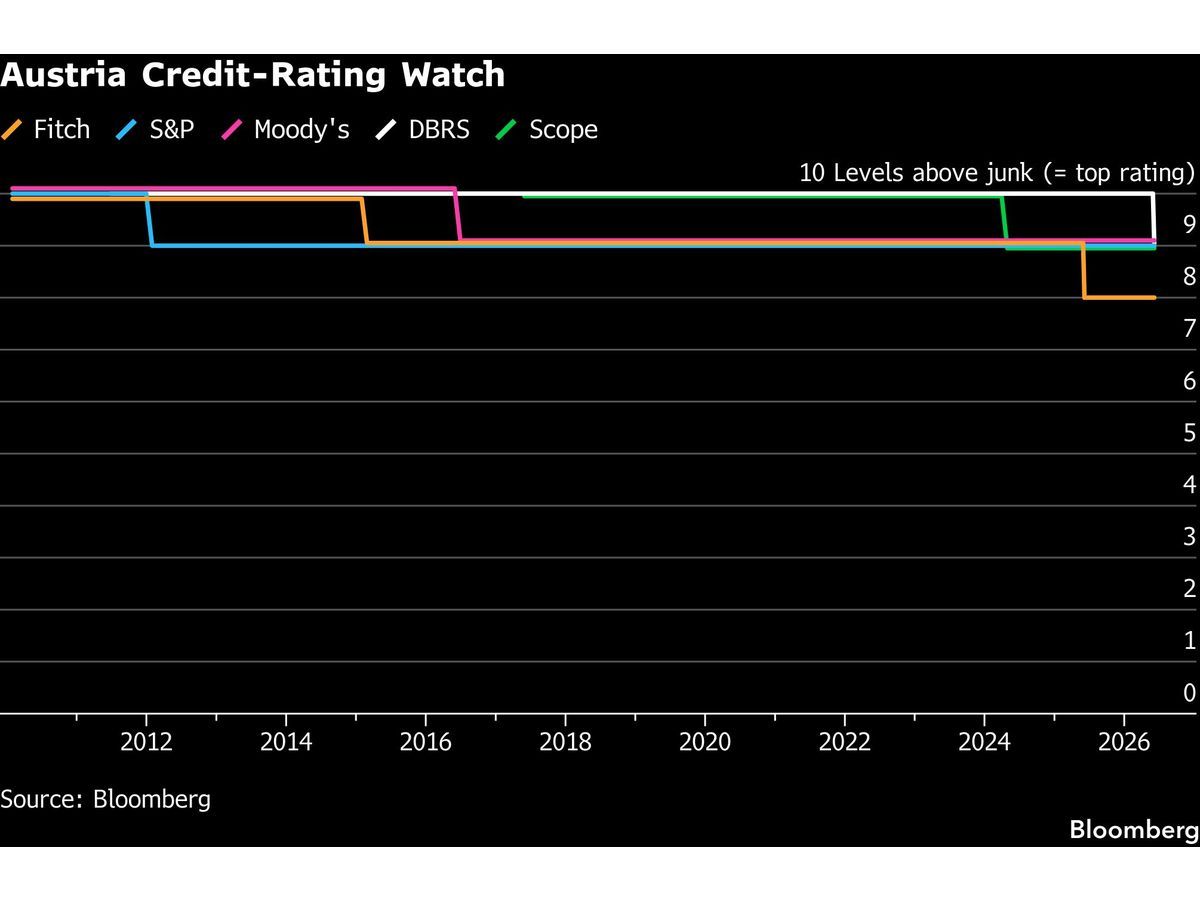

Austria lost its final top-tier credit score from a major rating agency on Friday, ending a multi-decade run as one of Europe's safest sovereign borrowers. Morningstar DBRS lowered the country to AA (high) from AAA, citing persistently wide budget deficits and a debt trajectory that continues to climb.

The downgrade means all five rating agencies used by the European Central Bank to assess collateral now place Austria below the highest grade. The decision caps a 14-year erosion that began when S&P Global Ratings cut the country during the euro-area debt crisis.

Why the DBRS Downgrade Hits Different Than Previous Cuts

The Mechanism Behind the Rating Change

Morningstar DBRS explicitly tied its decision to structural spending patterns. "Austria is running wider fiscal deficits than pre-pandemic largely due to durably higher expenditure levels," the agency wrote in its report. Despite the government's stated consolidation targets, DBRS concluded that "Austria's debt trajectory ratio will remain on a slow upward trend."

The key phrase is "durably higher expenditure levels." This is not a cyclical shortfall that will self-correct as growth returns. The agency is flagging a permanent upward shift in the spending baseline, which makes deficit reduction harder without politically difficult cuts or tax increases.

What Changed in the Fiscal Math

Austria's budget deficit has remained above the 3% of GDP threshold that triggers European Union fiscal scrutiny. The three-party coalition government – conservatives, social democrats, and liberals – aims to bring the deficit below 3% by 2028 through a two-year budget that Finance Minister Markus Marterbauer will present to lawmakers on Wednesday.

Practical rule: A rating downgrade that follows a multi-year trend rarely moves markets on its own. The question is whether the new rating level triggers forced selling by mandate-constrained investors or changes collateral eligibility.

The timeline matters here. The government has been negotiating this budget for months, and the downgrade adds urgency to Marterbauer's presentation. Markets will watch whether the budget includes credible measures or relies on optimistic growth assumptions.

The Bond Market's Surprising Indifference

Why Austrian Yields Haven't Reacted

Despite multiple downgrades in recent years – including Fitch Ratings cutting Austria to two steps below AAA last year – Austrian government bonds have barely budged. The 10-year Austrian yield currently sits 24 basis points above comparable German Bunds. That spread is below the 10-year average.

This tells a specific story about the bond market's current priorities. In a world where investors are focused on inflation, central bank policy, and geopolitical risk, the difference between AAA and AA+ for a stable euro-area economy is a second-order concern. The spread compression also reflects the ECB's role as a dominant buyer in the government bond market, which compresses differentiation between issuers.

What Would Break the Calm

The risk scenario for Austrian bonds is not the downgrade itself. It is what follows. If the government fails to deliver a credible deficit-reduction plan on Wednesday, or if the budget relies on growth assumptions that prove too optimistic, the spread could widen. The trigger would be a loss of confidence in the fiscal trajectory, not the rating label.

| Metric | Current | What Would Confirm the Risk | What Would Weaken It |

|---|

| 10-year spread vs Bunds | 24 bps | Widening above 40 bps | Compression below 15 bps |

| Budget deficit | Above 3% of GDP | No credible path to 3% by 2028 | Concrete spending cuts or revenue measures |

| Debt trajectory | Slow upward trend | Acceleration above 80% of GDP | Stabilization or decline |

The Structural Headwinds DBRS Identified

Energy Costs and Competitiveness

Austria's economy has struggled with high energy costs that have lifted inflation and hurt competitiveness. DBRS analysts Max Dietz and Michael Heydt acknowledged that economic momentum "is gradually picking up." They also flagged multiple structural risks:

- Prolonged geopolitical tensions that keep energy prices elevated

- Adverse demographic trends that increase pension and healthcare costs

- Increasing global competition in key manufacturing industries

- Elevated energy and labor costs that weigh on medium-term growth

These factors are not unique to Austria. Much of central Europe faces similar headwinds. Austria's high-cost industrial base makes it more exposed than lower-cost peers in the region.

The Demographic Time Bomb

The demographic issue is particularly acute. Austria's aging population means that even if the government balances the operating budget, long-term liabilities for pensions and healthcare will continue to push debt higher. This is the kind of structural pressure that rating agencies cannot ignore, and it explains why DBRS sees the debt trajectory as "slow upward" rather than stabilizing.

What Wednesday's Budget Must Deliver

The Credibility Test

Finance Minister Marterbauer faces a straightforward task on Wednesday. He must present a budget that convinces markets, rating agencies, and EU authorities that Austria can bring its deficit below 3% of GDP by 2028. The coalition government has already spent months negotiating, which suggests the final product will be a compromise.

Key insight: The downgrade is already priced into the spread compression. Wednesday's budget is the next catalyst. If the plan lacks specifics or relies on optimistic growth assumptions, the next rating action – likely a negative outlook from one of the remaining agencies – could follow within months.

The three-party coalition includes conservatives, social democrats, and liberals. Any spending cuts will face political resistance. The most credible path would combine modest spending restraint with revenue measures. The political math makes deep cuts unlikely.

The EU Dimension

Austria is currently under EU fiscal scrutiny for exceeding the 3% deficit threshold. The budget must satisfy domestic political constraints and also meet EU requirements. Failure to deliver a credible plan could lead to enhanced EU oversight or even fines, though the latter is rare in practice.

The Broader Read-Through for European Sovereigns

What Austria's Downgrade Signals for Peers

Austria's downgrade is not an isolated event. It reflects a broader pattern in which European sovereigns that entered the pandemic with strong fiscal positions have seen those buffers erode. Countries like the Netherlands, Finland, and Sweden face similar structural pressures from aging populations and high energy costs.

The difference is that Austria started from a higher rating and had further to fall. For investors holding European government bonds, the key question is whether the market will begin to differentiate more aggressively between AA and AAA credits. The alternative is that the ECB's presence will continue to compress spreads.

The Execution Risk for Bondholders

For now, the market is giving Austria the benefit of the doubt. The 24 bps spread over Bunds suggests investors see the downgrade as a lagging indicator of known fiscal trends rather than a new shock. That calculus changes if Wednesday's budget disappoints.

What to track:

- Wednesday's budget presentation: Does it include specific, credible measures or vague targets?

- EU response: Does the European Commission accept the plan or demand revisions?

- Spread movement: A sustained widening above 35 bps would signal that the downgrade is starting to matter for real money accounts.

- Next rating calendar: The remaining agencies (S&P, Moody's, Fitch) will review Austria in the coming months. Any negative outlook changes would compound the pressure.

Austria's loss of its last AAA rating is a milestone. It is the end of a long process, not the start of a new crisis. The real test comes Wednesday, when the government must show it can reverse the fiscal trajectory that the rating agencies have been warning about for 14 years.