Global smartphone production reached 284 million units in the first quarter of 2026, a 1.7% decline from a year earlier, according to TrendForce. Memory prices have been rising since the second half of 2025. The effect on Q1 output was muted because brands still held inventories of cheaper memory components. Consumer expectations of higher prices also helped sustain demand, cushioning the production impact.

That low-cost inventory buffer is now largely exhausted. TrendForce said most smartphone brands have started adjusting production in the current quarter after cheap memory supplies ran thin and price increases kept squeezing profits. The forecaster expects full-year 2026 production to fall roughly 16.2% to 1.051 billion units. If memory price increases stay elevated and brands raise retail prices repeatedly, the annual decline could be even steeper.

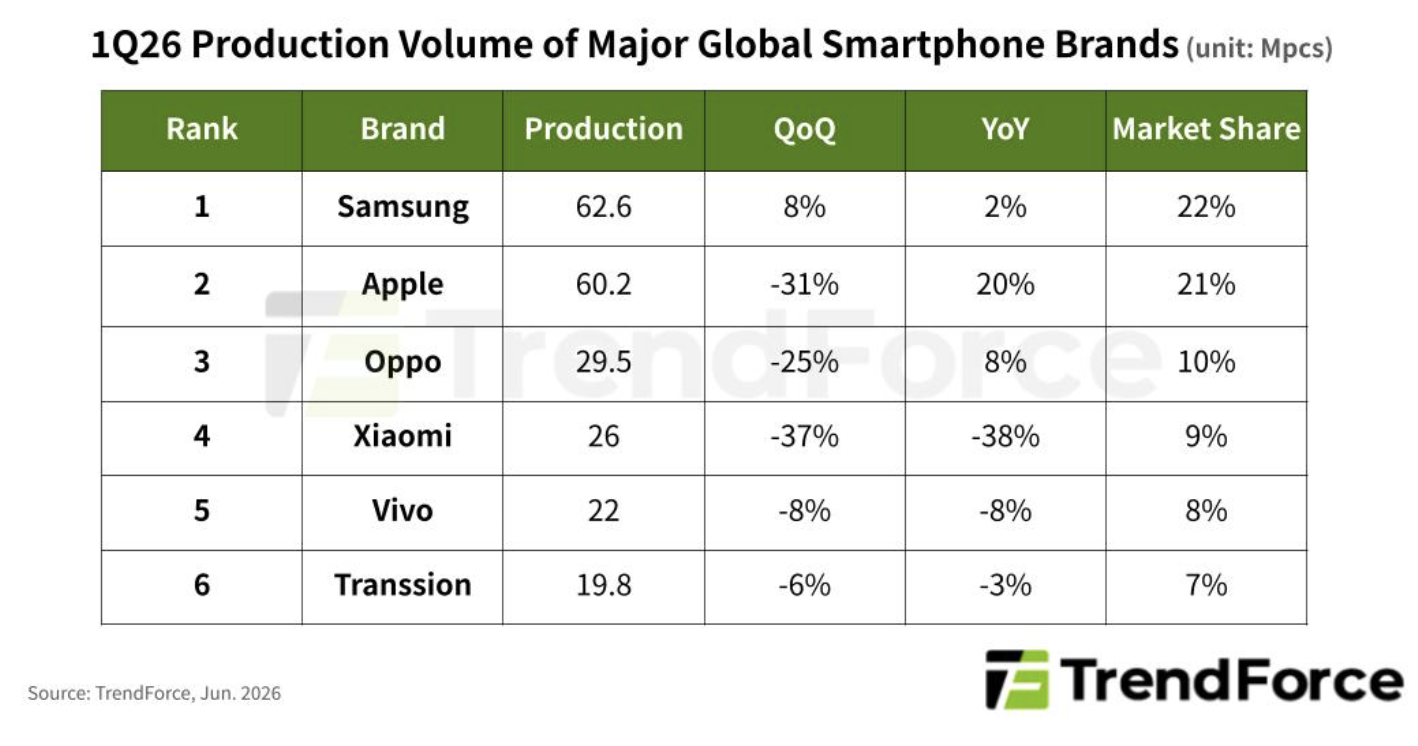

Apple produced about 60.2 million iPhones in Q1, up 19.7% from a year earlier. The iPhone 17e launch and ongoing ramp-up for newer models drove the gain. TrendForce noted that Apple is better positioned than competitors to absorb higher memory costs while maintaining profitability. Apple is more likely to prioritize market share expansion during the downturn, betting on future growth in recurring software and services revenue. For investors, that signals a focus on long-term ecosystem value rather than short-term hardware margin defense.

Samsung held the lead in production volume. The company benefits from Samsung Group's financial backing and a strong premium portfolio. TrendForce flagged a concern: Samsung's heavy exposure to lower-end models remains a risk as consumer sentiment weakens. That leaves Samsung's overall profitability more exposed to a consumer downturn than Apple's.

Among Chinese brands, Oppo led the group with 29.5 million units produced in Q1. Xiaomi and Vivo followed at 26 million and 22 million respectively. All three reported sequential declines from the previous quarter. TrendForce said surging memory costs are now weighing heavily on profitability, creating significant uncertainty around their 2026 production plans. Targets could be cut if cost pressures persist. The profit squeeze may push these brands to pull back on output, potentially tightening supply in the second half if demand holds.

Transsion produced roughly 19.8 million units in Q1, flat year-on-year, placing it sixth globally. The brand is especially vulnerable to the current memory price cycle. Its lineup skews toward entry-level and budget models where profit margins are razor-thin. It also had limited access to the low-cost component inventory that cushioned larger players in Q1. Transsion's thin margins leave little room to absorb cost increases, making its 2026 volume targets highly uncertain.

TrendForce's production data differs from Counterpoint's sales-based tracking. Production may include inventory builds not reflected in sales; sales may reflect drawdowns absent from production. Both research firms point to a market under severe supply-side stress. TrendForce's full-year forecast implies the steepest annual production drop in decades.