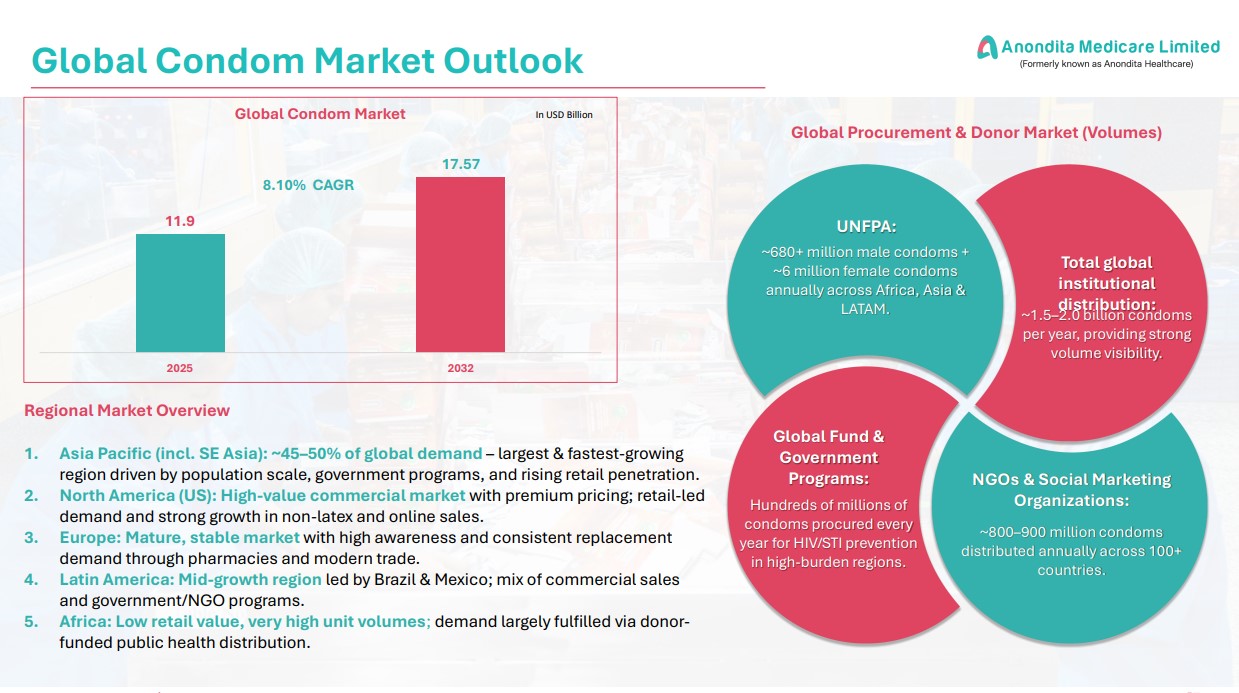

Anondita Medicare has entered the public market spotlight as a specialized player within the sexual wellness sector, a niche currently benefiting from broader shifts in consumer health awareness and accessibility. The company operates within a global condom market projected to reach approximately 17 billion dollars by 2032, supported by a compound annual growth rate of 8.1 percent. This growth trajectory provides a foundational backdrop for the company as it seeks to scale its manufacturing and distribution footprint.

Market Dynamics and Sector Positioning

The sexual wellness industry is transitioning from a fragmented retail landscape toward more standardized, brand-driven consumption. For Anondita Medicare, the ability to capture market share depends on its capacity to navigate the regulatory and supply chain requirements inherent in medical-grade manufacturing. The company is leveraging the expansion of the global market to justify its current capital allocation toward production capacity and product diversification.

Investors are evaluating whether the firm can maintain margins while competing against established multinational incumbents. The sector is sensitive to shifts in public health policy and consumer spending habits, both of which influence the velocity of inventory turnover for wellness products. Anondita Medicare’s current strategy focuses on aligning its output with these long-term demand trends, positioning itself as a beneficiary of the increasing normalization of sexual health products in emerging economies.

Operational Scalability and Growth Drivers

To sustain its growth, the company must demonstrate consistent execution in its logistics and quality control processes. The following factors remain central to the firm's operational outlook:

- Integration of automated manufacturing to reduce unit costs.

- Expansion of distribution networks into under-penetrated regional markets.

- Compliance with international quality standards to facilitate export growth.

These operational pillars are intended to insulate the company from localized price volatility. By focusing on high-volume, recurring demand, Anondita Medicare aims to build a defensive moat that supports its valuation as it scales. The company's ability to maintain its growth rate will be tested as it moves beyond its initial market entry phase and faces the realities of sustained competitive pressure.

AlphaScala Data and Market Context

For broader industrial and manufacturing comparisons, investors often look toward established entities like Deere & Company, which currently holds an Alpha Score of 36/100 and a Mixed label within the Industrials sector. You can view the latest metrics on the DE stock page to understand how large-cap industrial performance compares to emerging SME plays. While the scale of these companies differs significantly, the underlying focus on manufacturing efficiency and supply chain resilience remains a common theme in current stock market analysis.

The next concrete marker for Anondita Medicare will be its upcoming quarterly filing, which will provide the first clear look at how its production scaling efforts are translating into top-line revenue. Market participants will look for evidence of margin stability and the successful onboarding of new distribution partners as indicators of long-term viability.