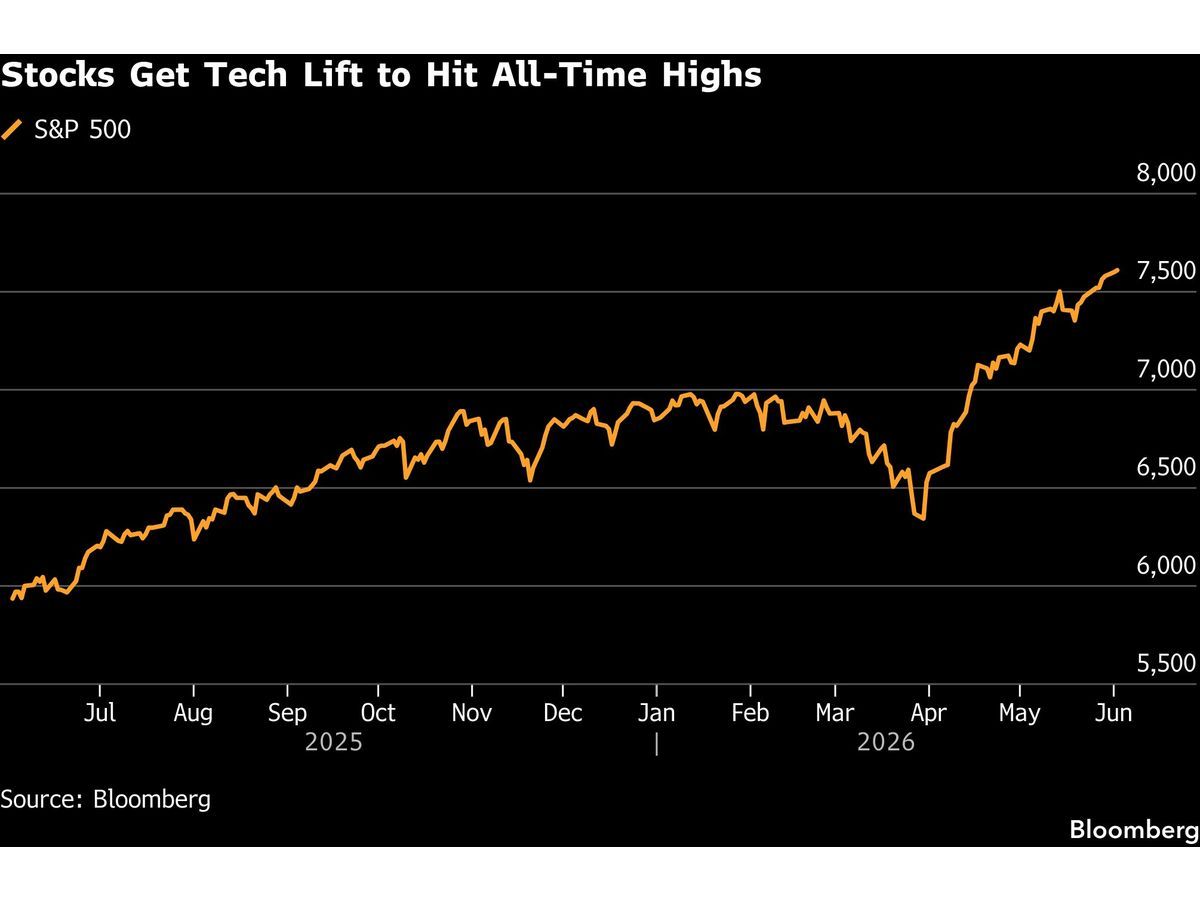

Global equities pushed to fresh all-time highs on Tuesday, driven by a surge in AI-related stocks. The MSCI All Country World Index rose 0.1% to a record, with both Asian and US benchmarks setting new peaks. The Philadelphia Semiconductor Index rallied almost 6% to a record, lifting Tokyo Electron Ltd. and Taiwan Semiconductor Manufacturing Co. to new highs. South Korean markets were closed for a holiday.

Yet the rally masks a growing tension. The yen hovered near 160 per dollar, a level that has historically triggered Japanese intervention. Brent crude rose for a third day on pessimism over US-Iran peace prospects. Gold edged lower to about $4,480 an ounce as inflation worries fueled expectations that borrowing costs will stay elevated. Bitcoin slid below $66,000.

The simple read is that AI momentum is overwhelming everything else. The better read is that a policy divergence trade is building: the Federal Reserve is repricing toward a hike, while the Bank of Japan may signal a path away from negative rates. That divergence is the real story for currency, rates, and commodity markets.

The Yen at 160: A Line in the Sand for Intervention

[USD/JPY](/markets/dollar-holds-two-month-high-as-iran-israel-truce-falters) traded near the 160 level on Tuesday, a psychological threshold that has historically prompted Japanese authorities to act. Traders are reluctant to push the pair beyond that level in the face of intervention risk. The immediate catalyst is Bank of Japan Governor Kazuo Ueda's planned speech, which investors will scan for clues on the rate outlook.

The simple read: 160 is a round number that scares the market. The better read: the yen is absorbing a divergence in monetary policy expectations. US Treasury yields edged higher after the first of three labor-market reports reinforced wagers that the Fed's next move will be to raise rates. Japan's 10-year government bond yield sits near 1.5%, leaving a carry advantage that keeps selling pressure on the yen.

The Intervention Calculus

Japan's Ministry of Finance spent a record ¥9.8 trillion propping up the yen in 2024. Officials have warned they are ready to act against excessive moves. The key threshold is not a strict level but the speed of the move. A slow grind through 160 may let officials wait for Ueda's speech. A sudden spike, by contrast, would trigger immediate intervention. Traders are pricing in a high probability of verbal intervention this week, with actual buying likely if the yen breaches 160.50.

Risk to watch: A break above 160 without intervention would signal a new leg in the carry trade, pressuring USD/JPY shorts and raising hedging costs for Japanese importers.

Tech Records Mask a Hawkish Repricing

The Philadelphia Semiconductor Index surged almost 6% to a record, led by Tokyo Electron Ltd. and Taiwan Semiconductor Manufacturing Co., which both closed at new peaks. Futures for the S&P 500 and Nasdaq 100 were little changed in late trading.

The rally masks a growing tension between AI-driven equity momentum and a hawkish repricing of Fed expectations. The 10-year US Treasury yield rose one basis point to 4.45%, extending its climb from the April low of 4.03%. The first of three labor-market reports due this week reinforced the view that the Fed's next move will be a hike. That is a headwind for growth stocks with stretched multiples, even as AI earnings momentum supports the semi sector.

TSM and the AI Valuation Question

TSM carries an Alpha Score of 70/100 on AlphaScala, classified as Moderate in the Technology sector. The stock's rally to a record priced in a future of sustained capex from cloud hyperscalers. The risk: a growing portion of that spending is being financed by debt issued at rising yields. If corporate bond yields push through 5.5%, the cost of capital for AI buildouts increases, potentially slowing orders for ASML and Tokyo Electron. The Philly Semi's 6% explosion looks like a momentum squeeze onto record highs, not a structural repricing.

Practical rule: When a sector index surges 6% in one day while yields rise, check whether the move came on short covering or genuine fundamental upgrades. The source does not specify which, so treat the speed of the rally as a caution signal.

The Tariff Proposal That Reshapes FX Risk

President Trump proposed levies of at least 10% on imports from most major trading partners, following an investigation into forced-labor practices. The tariffs aim to rebuild the sweeping wall struck down by the US Supreme Court. The immediate FX implication: currencies of trade-dependent economies face downside pressure. EUR/USD and GBP/USD both sit near the lower end of their recent ranges, and the tariff news compounds the rate-divergence story.

Transmission Through the Dollar

A 10% across-the-board tariff reduces the volume of US imports, which is mechanically positive for the trade-weighted dollar. The DXY index has stayed stable despite US-Iran deal risk, partly because the tariff threat anchors haven inflows. The mechanism: higher tariffs reduce foreign companies' USD receipts, lowering demand for the dollar for settlement. In the near term, uncertainty over trade policy tends to lift the dollar as a safe haven, particularly against emerging-market currencies. USD/JPY has room to test 161 if the BOJ does not signal a July hike.

Gold and Bitcoin Face a Hawkish Reality Check

Gold edged lower to about $4,480 an ounce as inflation worries stoked expectations that borrowing costs will stay elevated for longer. The simple read: higher yields make gold less competitive. The better read: gold's rally to $4,500 earlier this month was driven by central bank purchasing and geopolitical risk premiums from US-Iran tensions. The retreat tells us the inflation-yield channel is reasserting itself. A sustained break below $4,400 would open the path to $4,300, a level that marks the March low.

Bitcoin slid below $66,000, losing the $67,500 technical support. The correlation between BTC and the Nasdaq 100 is running at 0.45, high by historical standards, meaning tech stock weakness would pressure crypto further. The crypto market's next catalyst is the SEC's decision on spot Ethereum ETF approvals, which may be delayed past the implied May 23 deadline. For now, bitcoin is tracking risk-off shifts from the fixed-income market.

Private Credit Cracks Show Liquidity Risk Spreading

Cliffwater LLC capped redemptions at 5% in the second quarter after investors sought to pull about 17% of shares. The $1.8 trillion private credit market faces a mismatch between quarterly liquidity terms and annual asset valuations. When yields rise, mark-to-market losses on direct lending funds can trigger redemption requests that exceed available cash. This matters for FX markets because pension funds and insurers facing redemptions often liquidate liquid forex positions first, particularly in GBP/USD and AUD/USD.

The Mechanism in Practice

A 5% redemption cap prevents a run does not resolve the underlying valuation gap. If more fund managers follow Cliffwater, the signal to the broader market is that smaller investors are exiting private assets sooner than larger institutions. The alpha decay in private credit has accelerated as public markets offer higher yields with better liquidity. The 10-year Treasury at 4.45% now competes directly with direct lending funds that target 8–10% net returns after fees and losses.

The Next Decision Point

The immediate catalyst for all the above is BOJ Governor Ueda's speech. A signal that the July meeting could include a 25-basis-point hike would boost the yen and ease intervention pressure. A dovish hold would push USD/JPY through 160, triggering intervention and a yen spike that ripples through risk assets. The second US labor report Thursday and the CPI print next week will confirm whether the Fed is indeed done with hikes or poised to cut. For now, the markets are priced for a divergence that benefits the dollar and punishes gold and bitcoin, with the AI rally as the only force holding equity volatility low.

AlphaScala rates MSCI at Alpha Score 46 (Mixed, Financial Services) and TSM at 70 (Moderate, Technology). The semi rally lifts TSM's profile, the mixed score on MSCI reflects exposure to rate-sensitive financial products that may suffer if the private credit stress spreads.