Wuhan Optics Valley (Donghu High-Tech Development Zone) has delivered a series of globally competitive breakthroughs in OLED display technology, medical devices, and biotechnology. The zone's cluster of specialized companies – part of a broader “tech tree” incubator model – produced innovations that match or exceed current industry standards in each vertical. This is not a single product launch. It is a sustained output of indigenous R&D that directly challenges the incumbent supply chains in South Korea, the United States, and Europe.

Why it matters now: China's central government is accelerating self-sufficiency targets across semiconductors, displays, medical equipment, and advanced biomanufacturing. A regional hub delivering commercial-grade breakthroughs in three separate high-barrier sectors simultaneously signals that the policy push is producing tangible assets, not just subsidies.

The mechanic: The “tech tree” model pools shared infrastructure – cleanrooms, testing labs, raw material sourcing – while keeping individual companies competitive. That lowers the capital required for a single firm to reach production scale and shortens the time from lab to factory floor.

OLED Breakthroughs: Supply-Chain Pressure on Korean Incumbents

The zone's OLED advances target the largest cost and performance bottlenecks in display manufacturing: evaporation materials, encapsulation layers, and driver ICs. Local sourcing of these components could cut display panel costs by 10–15% for Chinese makers. That margin advantage directly pressures Samsung Display and LG Display in the mid-range smartphone and IT panel segments.

What this means: The global OLED market is still dominated by Korean producers. China's share of active capacity has risen sharply in the last three years. A second source of high-performance materials and IP inside the country removes a key supply risk for Chinese panel makers. It could accelerate their timetable for entering high-margin markets like tablets and notebooks.

Risk to watch: Commercial yields at scale matter more than lab-level specs. If the zone's companies can demonstrate yield rates above 85% on Gen-6 lines within two quarters, the technology is ready for adoption. If yields stall, the breakthrough remains a paper claim.

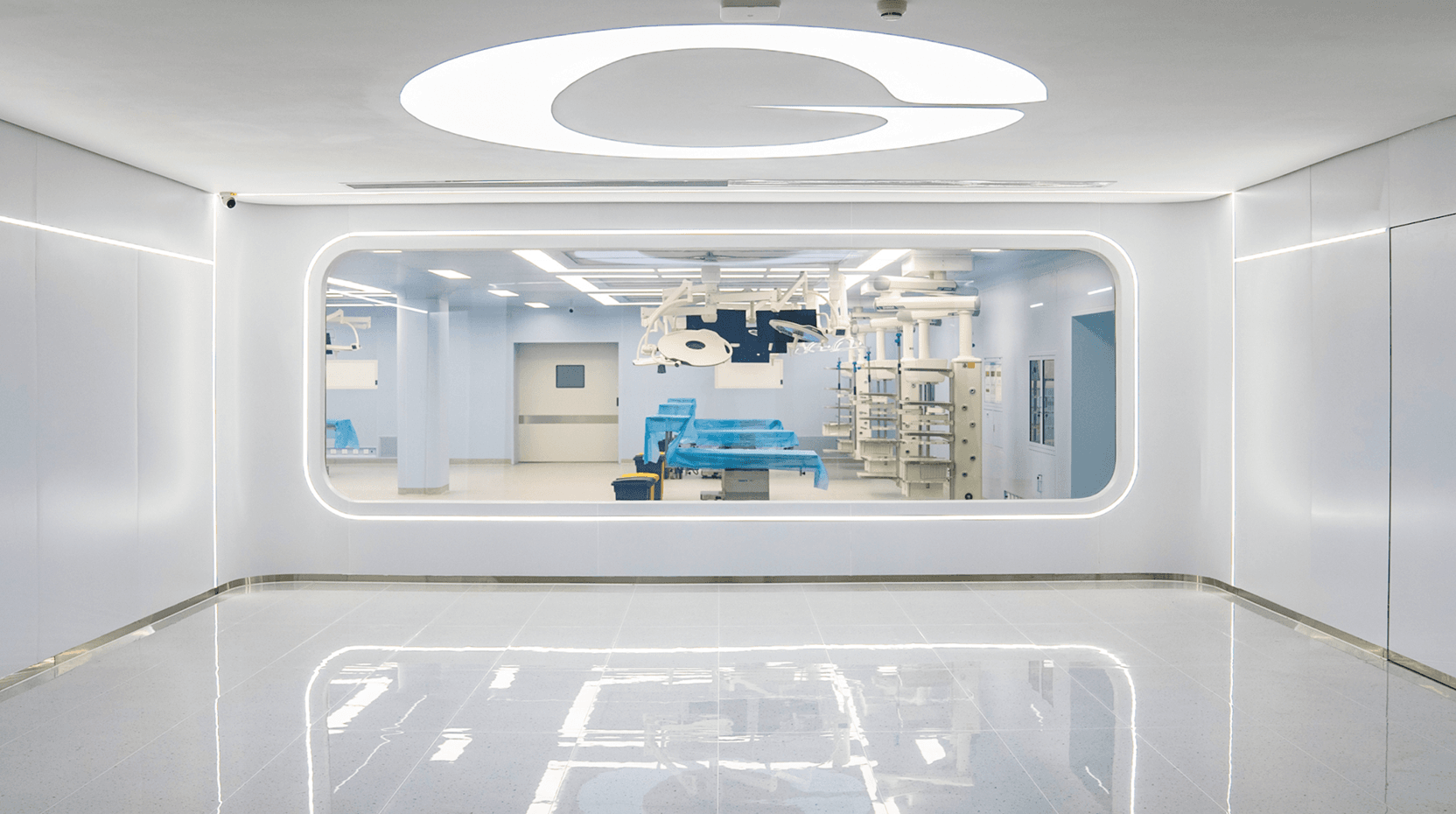

Medical Devices: The Domestic Substitution Play Accelerates

The medical device breakthroughs from the zone cover diagnostic imaging components and surgical robotics subsystems. The cluster has produced a high-resolution CMOS detector for CT and X‑ray machines that meets international dose-efficiency standards. It has also produced a force-feedback actuator for laparoscopic tools that competes with imported counterparts from Intuitive Surgical and Medtronic.

Why it matters now: China's procurement policies increasingly favor domestically sourced medical devices for public hospitals. A reliable local alternative for core imaging components reduces cost and supply-chain lead times for Chinese OEMs. The global medtech market is large enough that even a single-digit share shift represents billions in revenue reallocation.

Mechanic: The detachable actuator design allows Chinese surgical robot startups to assemble their own systems without buying the complete imported platform. That cuts entry costs by an estimated 30–40%.

What to track: NMPA (National Medical Products Administration) approval filings for any device using these components. A fast-track approval is the near-term catalyst that would validate the technology for large-scale hospital purchases.

Biotechnology: Synthetic Biology and Cell Therapy Manufacturing

The biotechnology segment of the zone's breakthroughs centers on synthetic biology platforms and cell therapy manufacturing processes. The cluster claims to have developed a continuous bioprocessing system that reduces cell therapy production time from weeks to days while maintaining viability rates above 90%.

Why it matters now: Cell and gene therapies are bottlenecked by cost and scalability. A manufacturing breakthrough that cuts production time and cost without sacrificing quality could unlock a wave of China‑developed CAR‑T and stem‑cell products priced competitively for the domestic market. Eventually, those products could be exported to Southeast Asia and the Middle East.

Mechanic: Continuous processing eliminates the batch-to-batch variability that plagues current cell therapy manufacturing. The zone claims its system uses closed-loop sensors and AI‑driven process control to maintain consistent conditions.

Risk to watch: Regulatory acceptance of continuous manufacturing for cell therapies is still nascent globally. Even if the technology works, the NMPA and FDA will require extensive validation data before approving products made on the platform.

Execution Risk and Next Catalysts

The single biggest risk across all three verticals is scaling. Lab‑scale or pilot‑line performance at Wuhan Optics Valley does not guarantee cost-effective mass production. Investors should watch for:

- OLED: Yield reports from any Chinese panel maker using the zone's materials on Gen‑6 lines.

- Medtech: NMPA registration filings for finished devices incorporating the CMOS detector or surgical actuator.

- Biotech: Partnership announcements with clinical‑stage cell therapy companies, plus any IND (investigational new drug) filings.

The next decision point comes in the next 12 to 18 months. If the zone's companies convert these breakthroughs into revenue-generating supply contracts, the case for a structural re-rating of the Chinese display and medtech supply chain will strengthen. If they do not, the story remains a speculative R&D pipeline with no near‑term earnings impact.