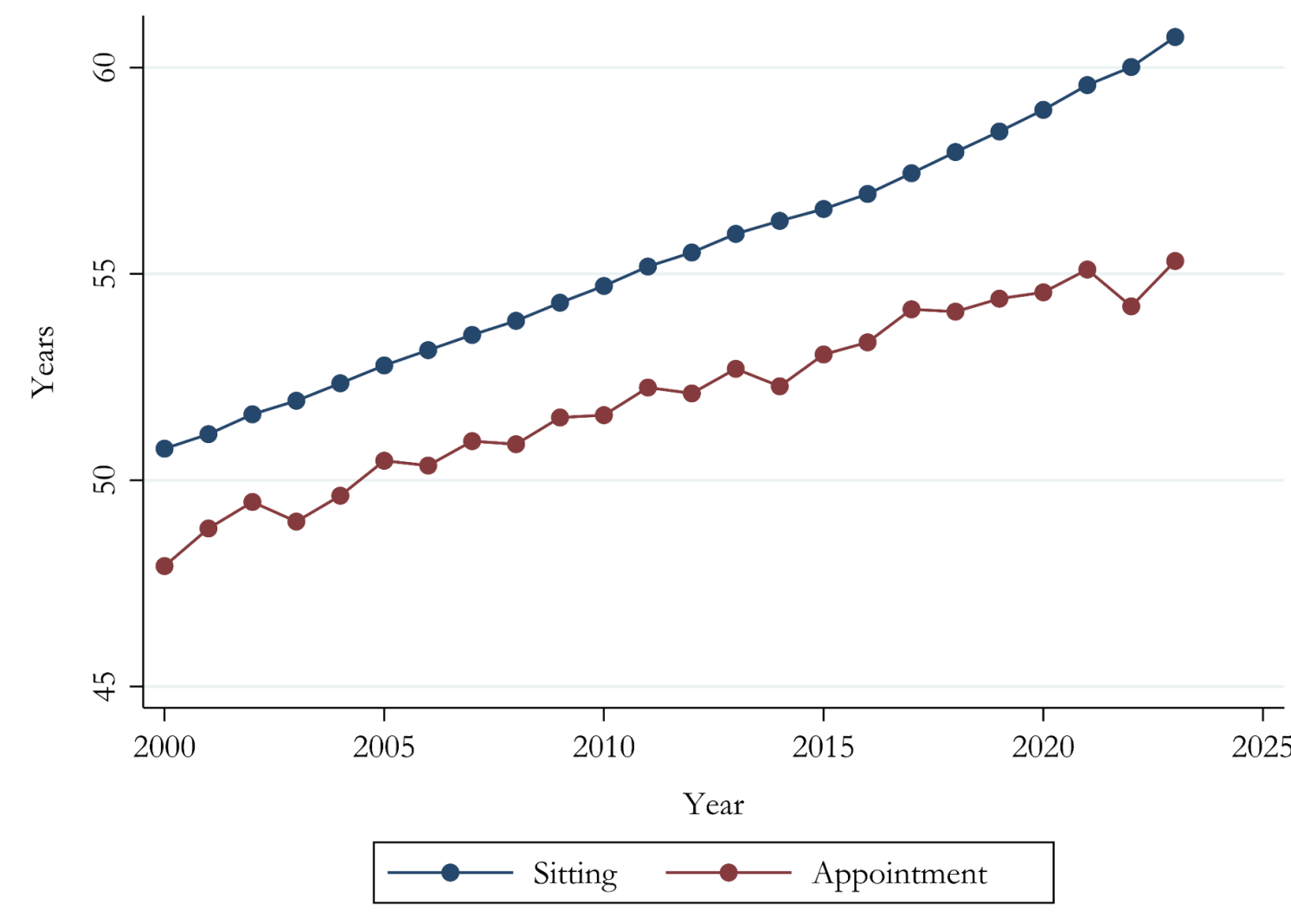

The average age of CEOs in the United States has climbed to 61 as of 2023, a shift that represents an increase of more than 10 years since the turn of the millennium. This trend, which extends across both the US and Europe, is not a byproduct of demographic aging or longer tenures alone. Instead, it reflects a fundamental change in the corporate labor market where firms are prioritizing broad, diversified experience over the raw, mid-career ability that historically defined executive selection. Data covering more than 50,000 CEOs indicates that the age at which individuals are appointed to the top role has risen from under 48 to 55 years, signaling that the shift is occurring at the point of entry rather than through delayed retirement.

The Shift Toward Generalist Human Capital

Corporate boards are increasingly navigating environments defined by heightened economic uncertainty and operational complexity. This environment has created a premium for generalist human capital, which is best acquired through long, varied career paths across multiple sectors, firms, and functional roles. Unlike specialized expertise, generalist skills require time to accumulate, effectively forcing the market to favor older candidates. While large, listed firms have historically maintained older leadership, the most significant convergence in this trend has occurred within smaller, private firms that are now mirroring the hiring patterns of their larger counterparts.

This demand for generalists is not merely a preference for seniority; it is a strategic response to market volatility. Firms operating in industries with high uncertainty are more likely to appoint older CEOs, particularly when they lack access to alternative sources of generalist expertise, such as elite strategy consultants. When firms cannot easily leverage external consultants to bridge gaps in strategy or coordination, they compensate by hiring executives who have spent decades building that experience themselves. This mechanism explains why the rise in CEO age is more pronounced in firms where generalist human capital is harder to develop internally.

Strategic Career Pathing and Supply-Side Shifts

Prospective CEOs are actively adapting to these new market requirements. Data from professional networks reveals that future executives are increasingly willing to accept lateral or even downward career moves in the short term to broaden their skill sets. By the end of the sample period, more than 40% of newly appointed CEOs had experienced a transition into a less senior position at some point in their career, doubling the rate observed in the early 2000s. This willingness to sacrifice immediate wage growth for long-term career diversification suggests that the supply side of the executive market is responding rationally to the higher premium placed on broad managerial capabilities.

This shift in career architecture has meaningful implications for firm-level outcomes. Older CEOs, while often associated with slower growth rates and less radical innovation, are also linked to reduced risk exposure. For investors, this suggests that the aging of the executive suite may be a defensive mechanism against the complexity of modern business cycles. As firms prioritize coordination and adaptation over pure growth, the tenure and age of the C-suite serve as a proxy for a company's risk management posture.

Market Read-Through and Future Constraints

For those analyzing stock market analysis, the trend toward older, generalist leadership suggests a potential ceiling on aggressive innovation in sectors where this hiring pattern is most entrenched. If the rise in CEO age is a rational response to uncertainty, then a reversal would likely require a period of sustained, predictable economic growth that reduces the value of generalist experience. Conversely, if technological shifts like AI continue to automate routine managerial tasks, the relative value of human-centric, generalist decision-making may increase further, cementing the current trend.

In the context of specific sectors, the data shows a clear divergence in how firms manage their leadership pipelines. For instance, FAST stock page and WELL stock page operate within sectors where operational complexity is a constant, yet their specific leadership needs may differ based on their exposure to the broader industrial or real estate cycles. While the average CEO age across the broader market is 61, the specific requirements of these firms remain subject to their individual competitive landscapes. AlphaScala proprietary data currently labels both FAST and WELL as Mixed, reflecting the ongoing tension between traditional operational models and the need for the adaptive, generalist leadership styles that are becoming the new industry standard.

Ultimately, the rise in CEO age is not an indication of institutional stagnation but a structural adjustment to the modern economy. As the pathways through which expertise is acquired become more fragmented, the time required to reach the top will likely remain elevated. Investors should view the age of an incoming CEO not as a static demographic fact, but as a signal of the firm's current strategy regarding risk, complexity, and the necessity of broad-based experience in an uncertain market environment.