Back to Markets

Stocks● Neutral

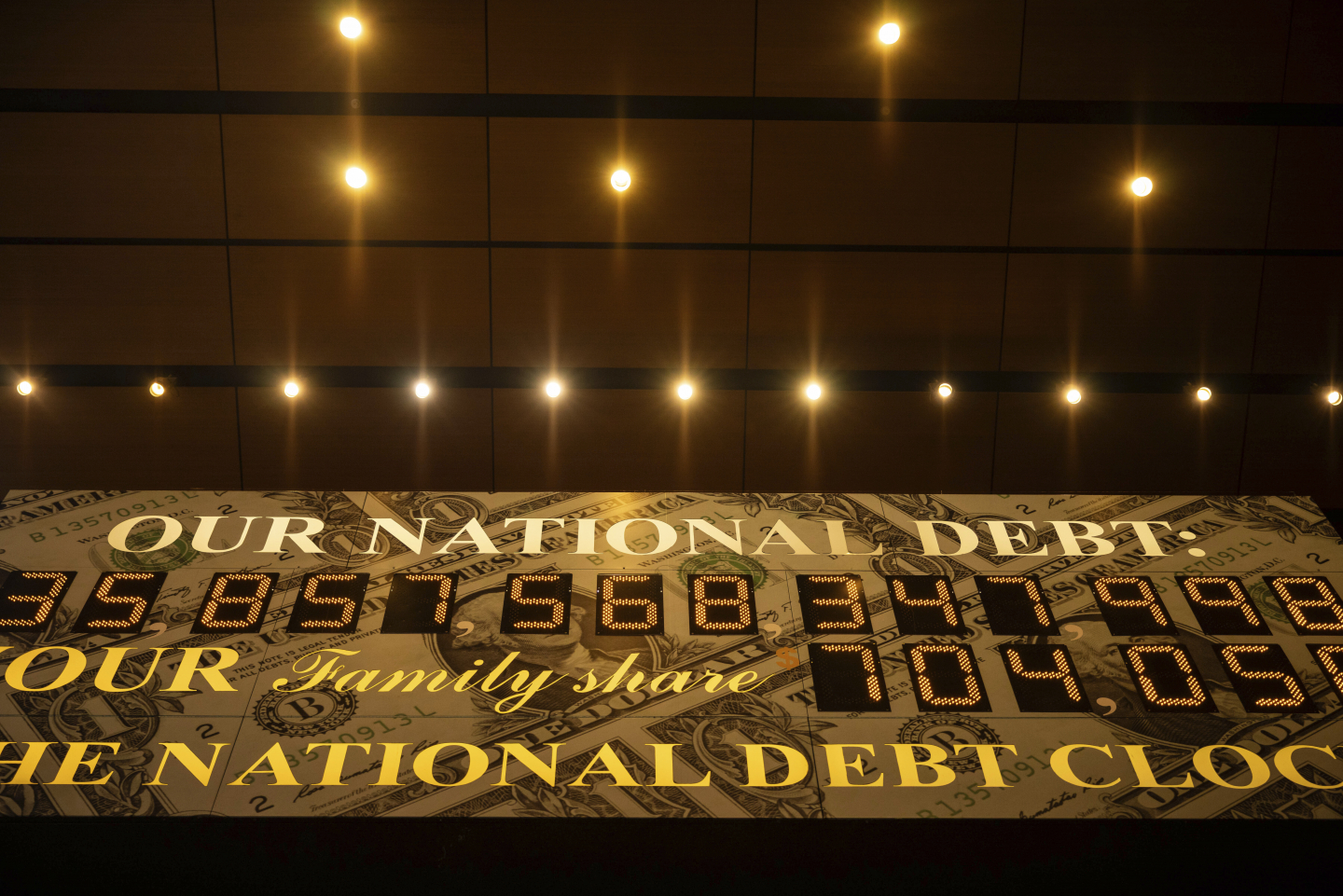

Why Tax Hikes and Spending Cuts Won't Reduce the Debt

Tax revenues have risen since 1981, but the debt has grown. Spending cuts free up borrowing capacity. Growth enables more spending. Ignore the debt crisis noise.

Continue with

The national debt debate rests on a premise that has not held for 45 years. Raising taxes or cutting spending will reduce the debt, the argument goes. Treasury data show otherwise.

Federal tax revenues have risen substantially since 1981. The debt has not fallen. It has grown. The relationship between revenue and debt is not inverse. It is direct. More revenue enables more spending. Politicians spend what they have, then borrow more against the expectation of future revenue. The last 45 years make this pattern unmistakable.

The same logic applies to spending cuts. Reducing government spending does not shrink the debt. It frees up borrowing capacity. Congress redirects the savings to other programs, or uses the improved fiscal headroom to borrow more. The past four decades show this repeatedly.

Growth does not solve the problem either. The argument that the economy can grow its way out of debt has been tested. Stock markets have soared. Economic growth has been remarkable at times. Debt has risen alongside. Growth gives politicians the confidence to spend and borrow more, not less.

Treasury markets have never reflected a debt crisis. Yields have trended lower for decades. The bond market has not priced in default risk for the U.S. government. That lack of concern is the single most important data point the hawks ignore.