Cygnus Metals (ASX: CY5, TSXV: CYG, OTCQB: CYGGF) released final assays from its winter infill program at the Golden Eye deposit within the Chibougamau Copper-Gold Project in Quebec. The headline numbers include 39.5g/t AuEq over 3m, 5.9m at 28.8g/t AuEq, and 8.4m at 16.3g/t AuEq. The company also confirmed the start of exploration drilling at the Gwillim gold prospect with joint venture partner Alamos Gold (NYSE: AGI).

For a junior explorer, these two workstreams – resource conversion and greenfield exploration – serve very different purposes. The market often lumps them together. The risk profile, valuation impact, and timeline to production differ sharply. This article breaks down what each program actually means for Cygnus and how to separate signal from noise in the drill results.

The Two-Track Strategy: Resource Conversion vs. Discovery

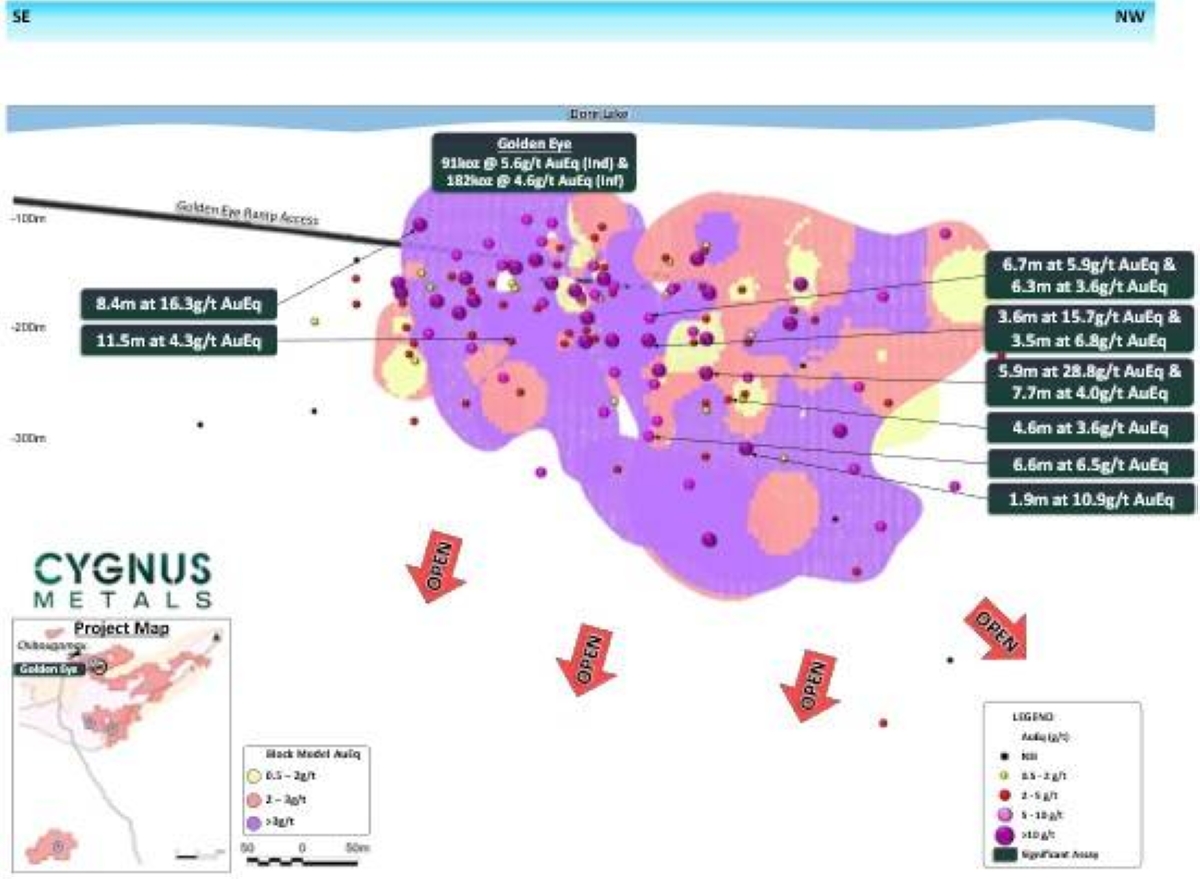

Cygnus is pursuing a dual track: upgrade Inferred resources to Indicated at Golden Eye while drilling new targets like Gwillim to grow the overall resource base. The winter program at Golden Eye used three rigs on an engineered ice pad, drilling 15 holes for 5,632 metres. All results are now received.

The Golden Eye deposit is shallow – within 100m of surface – and sits 3km from the existing process plant. It has double ramp access to within 140m of the deposit. That existing infrastructure is a meaningful advantage: the Chibougamau processing facility is the only base metal plant within a 250km radius, and the area has a sealed highway, airport, rail, and 25kV hydro power.

What Resource Conversion Actually Changes

Inferred resources are the lowest confidence category under JORC and NI 43-101. They cannot be used in economic studies for mine planning. Converting them to Indicated allows the company to include them in a feasibility study and ultimately a mine plan. That is the direct path to a production decision.

The recent intercepts at Golden Eye – including 8.4m at 16.3g/t AuEq and 5.9m at 28.8g/t AuEq – are consistent with the grades reported in the 2025 maiden resource. The company is not discovering new ounces. It is proving that the existing ounces are where the model says they are. That reduces geological risk. It does not add a new catalyst by itself.

The Common Mistake: Treating Infill Results Like Discovery Hits

A naive read of the press release might treat 39.5g/t AuEq over 3m as a bonanza-grade discovery. In reality, that intercept is one of several infill holes designed to tighten drill spacing. High-grade intervals within an already-defined deposit are expected. The real question is whether the average grade and continuity hold up across the full resource.

Cygnus’s Gwillim program is the discovery track. The company is targeting historic high-grade intersections with one rig. Historic intersections from the source include 10.2m at 22.4g/t Au, 2.3m at 41.6g/t Au, and 4.7m at 13.3g/t Au. No new assays are out yet. The presence of Alamos Gold as a joint venture partner adds credibility. Alamos is a mid-tier gold producer with operations in Canada and Mexico. Its involvement suggests the prospect has enough scale potential to interest a producer.

The Alamos Gold JV: What It Signals

Alamos Gold (AGI) has an Alpha Score of 68/100 (Moderate) in the Basic Materials sector. That score reflects a balanced risk-reward profile for a producer. For a junior like Cygnus, a JV with a well-capitalized partner reduces the dilution risk of funding exploration alone. Alamos is funding the first program at Gwillim. Cygnus retains exposure to any discovery.

Cygnus also has near-term drill targets at Copper Rand and Joe Mann, both historic producers in the district. The company intends to provide updates toward the end of the quarter on Gwillim results.

Valuation Framework for Cygnus

Cygnus trades as a development-stage copper-gold play. The Chibougamau project has a 900,000tpa processing facility already in place. That is rare for a junior – most explorers have to build a plant from scratch. The hub-and-spoke model (feed multiple deposits to a central plant) lowers the capital intensity of each new deposit.

Golden Eye is the first spoke. The infill program is designed to move it toward a feasibility study. The company also has near-term drill targets at Copper Rand and Joe Mann, both historic producers in the district.

What Confirms the Thesis

- Consistent grade continuity in the next resource update (expected later in 2026). If the Indicated resource at Golden Eye matches or exceeds the Inferred grade, the deposit moves closer to a mine plan.

- Discovery-grade intercepts at Gwillim. High-grade gold intersections from the current program would add a new asset to the portfolio and potentially re-rate the stock.

- Alamos Gold continues funding. If Alamos extends the JV beyond the initial program, it signals confidence in the prospectivity.

What Weakens the Thesis

- Grade dilution in the resource conversion. If the Indicated resource shows lower average grades than the Inferred model, the deposit economics deteriorate.

- Gwillim returns sub-economic grades. A dry hole at Gwillim would not kill the stock. It would remove the near-term discovery catalyst.

- Equity dilution. Cygnus is spending on drilling and studies. If it needs to raise capital at a low share price, existing shareholders take the hit.

Risk to Watch: Execution and Funding

Cygnus is a micro-cap explorer. The market cap is small. Liquidity on the ASX and TSXV can be thin. The company has a clear strategy. The timeline to production is years away. The next catalyst is the resource update for Golden Eye. That update will show whether the infill program delivered the expected conversion.

For a deeper look at gold sector dynamics, see the gold profile and the recent analysis of the Predictive Discovery and Robex merger. For Alamos Gold’s current standing, check the AGI stock page.

Bottom line for traders: The Golden Eye results are a check-the-box milestone. They confirm the deposit is real and high-grade. They do not change the valuation by themselves. The Gwillim program with Alamos is the swing factor. Watch for assays from Gwillim in the coming months. If they match the historic high-grade intersections, Cygnus could re-rate significantly. If not, the stock will trade on the slow grind of resource conversion and feasibility work.