Back to Markets

Stocks● Neutral

Why CDCTC Refundability Matters to Child Care Stocks

A pandemic-era blueprint shows refundability plus a higher cap boosts paid care usage. That policy template is the next catalyst to track for child care providers.

Continue with

The Child and Dependent Care Tax Credit (CDCTC) has a structural flaw: it is nonrefundable, meaning families with zero tax liability receive nothing. Emerging research cited by EconoFact shows that increasing the credit's generosity does increase paid child care use. That finding creates a clear catalyst path for the child care sector.

For an investor watching the care-services space, the question is whether a policy fix is likely. The pandemic-era expansion of the CDCTC offers a concrete template. That expansion made the credit refundable and raised its maximum value. If legislators move toward a permanent version of that template, it represents a direct demand catalyst for child care providers.

How the CDCTC’s Nonrefundable Design Blocks Demand

The CDCTC allows families to claim a portion of caregiving expenses for children under age 13 or for adult dependents. The credit reduces tax liability dollar-for-dollar up to a cap. Because it is nonrefundable, a family with zero tax liability after other deductions receives zero benefit. That structural exclusion is the core design flaw.

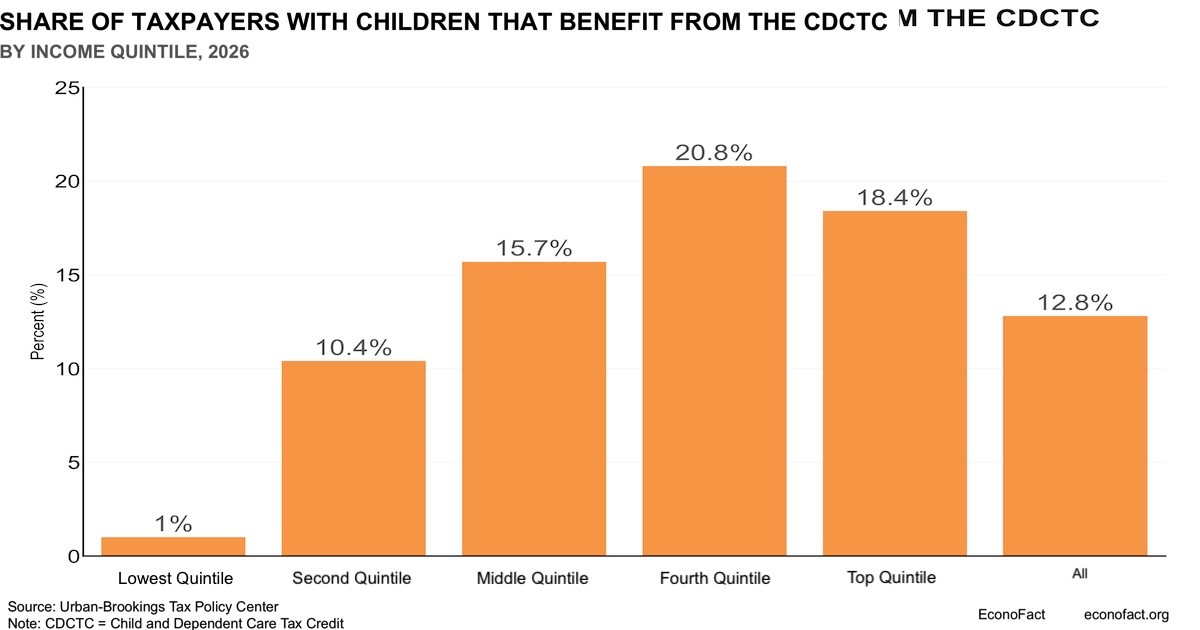

Why Low-Income Families Get No Help

Lowest-income families face the highest care cost burden as a share of income. The CDCTC’s nonrefundable structure means exactly those families get no help. Research cited by EconoFact shows that increasing generosity increases paid care use. The effect concentrates among families with a tax liability. The credit acts as a middle-class subsidy, not a poverty-reduction tool.

Key insight: Refundability is the lever that reaches low-income families. Data from the temporary pandemic expansion shows that when the CDCTC became refundable, usage rose across the income distribution.

The Inflation Erosion Problem

The credit’s dollar amounts are not indexed for inflation. Child care costs rise faster than general prices. That trend erodes the credit’s real value each year. The EconoFact analysis notes that the credit “does not keep pace with inflation.” Over a multiyear period, the effective subsidy shrinks annually. Congress must act to maintain its purchasing power.

Risk to watch: A temporary expansion that lacks an inflation index loses real purchasing power quickly. That would limit the demand boost for care providers.

The Pandemic Blueprint: Refundability Plus Scale

The temporary expansion during the Covid-19 pandemic is the real-world example. Congress made the CDCTC refundable and increased the credit’s maximum value. The EconoFact analysis calls this expansion “a blueprint for a credit that is generous enough to make a difference to family budgets.” That specific policy template is the next catalyst for the sector.

The table shows the two critical levers. Refundability extends the benefit to the full income distribution. A higher maximum credit increases the subsidy magnitude. Combined, they create a step-change in effective demand.

What the Blueprint Means for Demand

A family earning $50,000 with two children and $10,000 in care expenses receives a small nonrefundable credit currently. Under a refundable expansion with a higher cap, that family could receive several thousand dollars in cash. The net price of care drops. At the margin, some families switch from informal arrangements to licensed day care or in-home aides.

That switching effect drives revenue for child care providers. Revenue depends on enrollment numbers. Higher subsidies increase enrollment directly, all else equal.

What this means: The elasticity of care usage to the credit’s generosity is the key input for any demand forecast. Research suggests a positive elasticity. The magnitude matters for stock price response. A small nonrefundable expansion may produce a muted reaction. A large refundable expansion could trigger a sector re-rating.