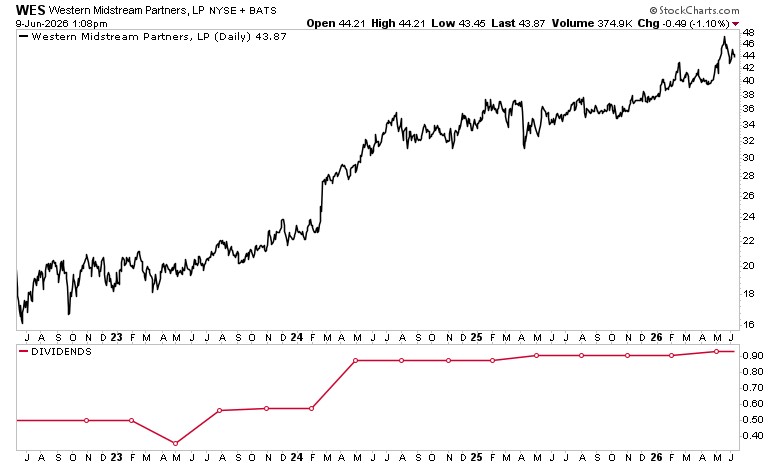

Western Midstream Partners units hit a record $48.01 on May 20 and have held near that level since. The catalyst is straightforward: two large acquisitions closed or announced in the past eight months are feeding through to distributable cash flow, and the partnership is passing more of it to unitholders.

The bigger story is the shift in the asset base. WES paid $2 billion for Aris Water Solutions in October 2025, then in May agreed to buy Brazos Delaware II for $1.6 billion – half cash, half units. Brazos brings 900 miles of pipeline, 460 million cubic feet per day of gas processing capacity, and 470,000 dedicated acres in the Texas Delaware Basin under long-term fixed-fee contracts. That acreage processed 336 MMcf/d of gas and 25,000 barrels of oil per day in 2025.

First-quarter results show the Aris contribution already landing. Adjusted EBITDA hit a record $683.1 million, up 7% from the prior quarter and 15% year over year. Distributable cash flow came in at $508.9 million. Free cash flow was $242.3 million on $469.9 million of operating cash flow.

CEO Oscar Brown credited the Aris deal for the sequential jump. The Brazos deal, expected to close late in the second quarter, will add another layer.

The fee structure is the reason the cash flow is predictable. 97% of gas contracts and 100% of liquids contracts are fee-based, with minimum-volume commitments and acreage dedications. That means WES collects on throughput regardless of where crude or gas prices trade. The Iran conflict pushed West Texas Intermediate from $57 a barrel on Jan. 1 to $109 on April 8, and it has since settled near $90. WES units barely flinched through the volatility.

The distribution has been reliable since 2008. In May, WES paid $0.93 per unit for the first quarter, a 2.2% increase from the prior quarter. That annualises to $3.72 per unit, or roughly 8.5% at current prices.

Wall Street sees room to run. The 12-month analyst price target range runs from $44.73 to $54.00, implying up to 23% upside from the record close. Insiders hold 38.39% of units. Institutions hold another 42.45%, with Alps Advisors, Invesco, and Goldman Sachs among the largest positions.

WES carries an Alpha Score of 65 out of 100, labelled Moderate, in the Energy sector. The score reflects the cash flow visibility from the fee-based contracts and the recent acquisition-driven growth, balanced against the leverage from the $1.6 billion Brazos deal.

The risk to watch is the integration. WES is funding the Brazos cash portion from the balance sheet, and the unit issuance dilutes existing holders by roughly 5%. If the combined asset base delivers the throughput growth Brazos showed in 2025, the coverage ratio should hold. If volumes slip, the distribution growth rate could stall.

For now, the record high and the 8.5% yield are both backed by cash flow that does not depend on the next oil price move. That is the case for owning WES through the cycle.