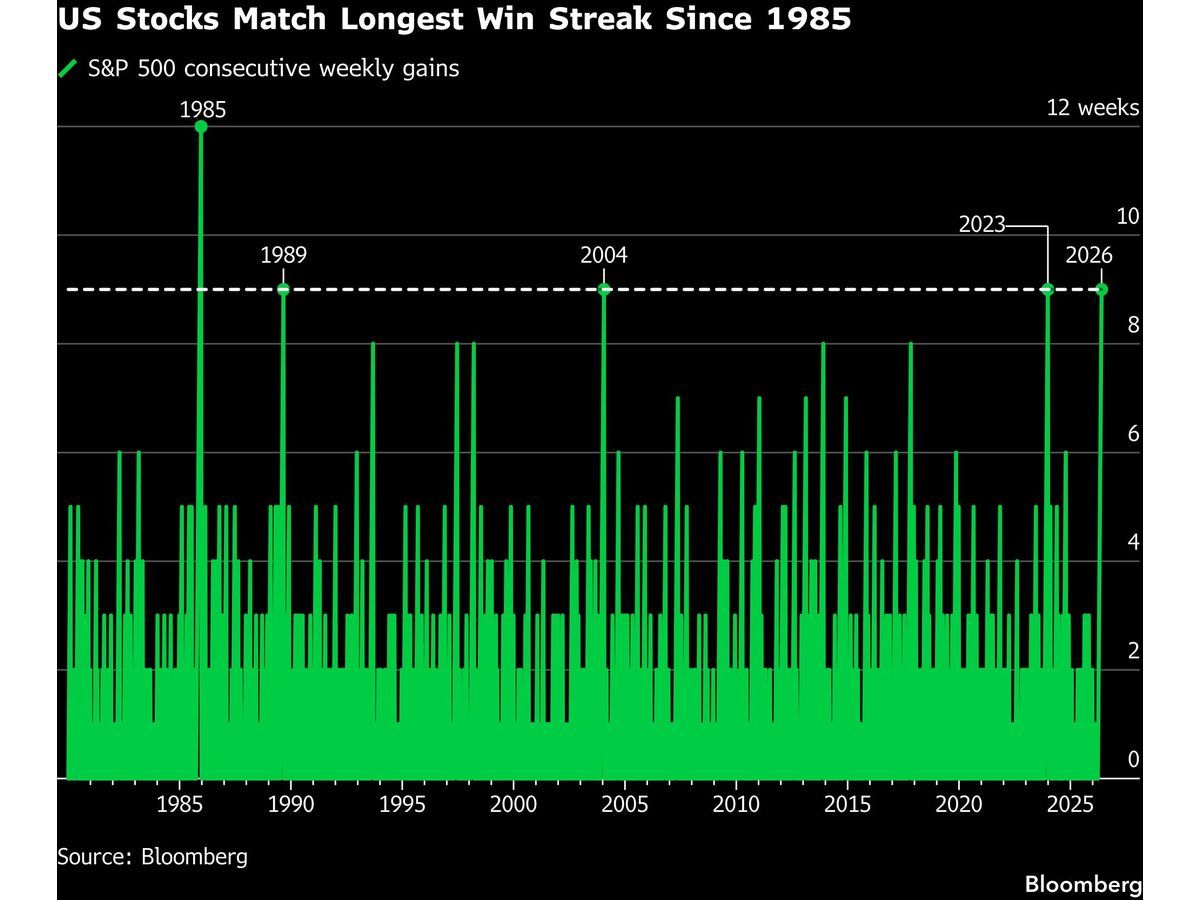

The S&P 500 closed at an all-time high near 7,600 on Monday, extending its winning streak to eight straight gains – the longest since May 2025. The move rested on two distinct catalysts: President Donald Trump’s statement that talks with Iran are continuing at a rapid pace, and a tech-led surge tied to renewed artificial-intelligence enthusiasm.

US crude pared its rally to $92 a barrel after Trump also said Israel and Hezbollah agreed to stop attacking each other. The combination of a softer geopolitical risk premium and a fresh AI bid pushed the index higher. The underlying mechanics, however, are more fragile than the headline suggests.

The Dual Catalyst That Pushed the S&P 500 to 7,600

The Iran Diplomacy Leg

Trump’s remarks came after days of escalating violence in Lebanon that risked upending indirect negotiations between Washington and Tehran on extending a ceasefire agreement. Earlier Monday, Iran said it would suspend negotiations with the US in protest over Israel’s offensive. The market’s immediate reaction was a rotation out of energy and into equities – a repricing of tail risk around a broader Middle East conflict, not a fundamental improvement in the US economy or corporate earnings.

Jason Pride and Michael Reynolds at Glenmede described the situation bluntly:

The Glenmede strategists added that while progress toward a deal appears likely over time, conditions in the Strait of Hormuz remain fragile and the direction of energy prices will continue to play a key role in shaping the near-term outlook for inflation and interest rates.

The AI Enthusiasm Leg

Alongside the geopolitical repricing, the S&P 500 got a second lift from renewed AI enthusiasm. The tech sector led Monday’s advance, adding to a run that has now produced eight straight gains. The source text does not specify which AI-related catalysts moved stocks on Monday. The pattern, however, is consistent with a market that has been rotating between geopolitical headlines and AI narratives for weeks. When the Iran risk premium compresses, capital flows back into the high-beta tech names that have dominated the 2025 rally.

Key insight: The S&P 500 at 7,600 is a composite of two separate trades – a short oil / long equity position on Iran diplomacy, and a momentum-driven AI bid. If either leg reverses, the index is exposed.

The Oil Mechanism and the Fragile Geopolitical Premium

The price action in crude tells the real story. US oil fell back toward $92 after Trump’s comments, paring a rally that had been building on fears of a Strait of Hormuz disruption. The Glenmede strategists noted that conditions in the Strait remain fragile. A breakdown in talks would send crude back above $100 quickly. The market is pricing a diplomatic resolution that has not yet been signed.

Risk to watch: Any new escalation between Israel and Hezbollah or a suspension of US-Iran talks would reverse the oil premium compression and hit equities, especially the rate-sensitive tech names that led Monday’s rally.

The ISM Data Contradiction: Rate Hike Risk vs. Rally

While markets cheered the geopolitical and tech headlines, the economic data released Monday told a different story. The Institute for Supply Management reported that US manufacturing activity expanded in May at the fastest pace in four years. The group’s price gauge remained close to levels not seen since 2022, indicating that materials costs continued to rise sharply for producers.

Combined with the renewed advance in oil, the ISM report added to speculation that the Federal Reserve’s next move on interest rates will be a hike. That is a direct threat to the equity rally, particularly in the rate-sensitive tech names that led Monday’s advance.

| Metric | Reading | Implication |

|---|

| S&P 500 | ~7,600 | All-time high, 8-day win streak |

| US crude | ~$92 | Pared rally on diplomatic hopes |

| ISM manufacturing | Fastest expansion in 4 years | Economy running hot |

| ISM price gauge | Near 2022 highs | Input cost pressure rising |

| Fed rate speculation | Hike probability rising | Contradicts equity rally thesis |

What this means: The equity market is pricing a Goldilocks scenario – falling geopolitical risk, steady AI growth, and no Fed tightening. The ISM data directly challenges the third assumption. If oil stays elevated and the price gauge remains high, the Fed will have a strong case to hike, which would compress equity multiples.

What Confirms or Breaks the Setup

Confirmation signals

- A signed or detailed framework for US-Iran negotiations, which would lock in the lower oil premium.

- The ISM price gauge declining in June, which would reduce rate hike pressure.

- Continued AI earnings beats or product announcements from major tech names.

Risk signals

- A breakdown in Iran talks or renewed Israel-Hezbollah hostilities, which would send crude above $100 and reverse the equity rally.

- The Fed signaling a hike at the June or July meeting, which would hit the tech sector hardest.

- A spike in oil above $95, which would feed directly into the ISM price gauge and reinforce the hike narrative.

Bottom line for traders: The S&P 500 at 7,600 is a fragile construct. The Iran trade is unconfirmed, the AI trade is momentum-dependent, and the ISM data is pointing toward a rate environment that would normally cap equity valuations. The next move in oil or the next Fed comment will likely determine whether this rally has legs or reverses.

For a broader view on how geopolitical risk interacts with sector positioning, see AlphaScala’s stock market analysis. Investors tracking the tech-heavy side of this rally can review the NVIDIA profile for AI exposure benchmarks.