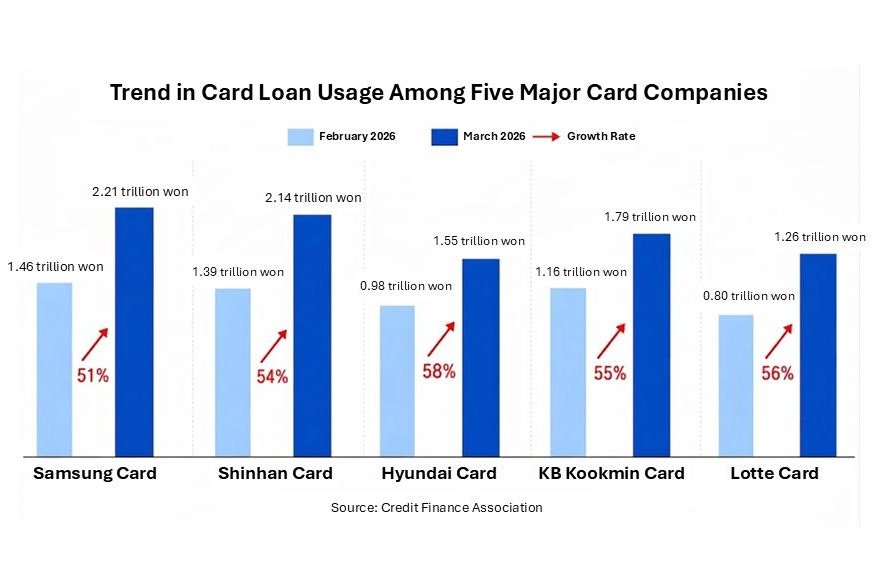

South Korean credit card loans and cash advances surged by 55% in March, marking a significant shift in consumer borrowing behavior. This rapid expansion in high-interest credit utilization points to mounting financial pressure on households struggling to manage liquidity. As these short-term credit products often serve as a last resort for borrowers, the spike suggests a deterioration in the credit quality of the underlying consumer base.

Credit Risk and Industry Exposure

The sudden increase in card-based borrowing forces a re-evaluation of the risk profiles held by major South Korean financial institutions. Credit card companies rely on stable repayment cycles to maintain margins, but a 55% jump in utilization over a single month indicates that a larger portion of the population is relying on revolving debt to meet basic obligations. This trend typically precedes a rise in delinquency rates, which would directly impact the profitability of card issuers.

Financial institutions are now tasked with managing the balance between maintaining market share and tightening credit standards. If the current pace of borrowing continues, issuers may be forced to increase loan-loss provisions, which would weigh on earnings reports throughout the coming quarters. The reliance on cash advances is particularly concerning, as these instruments carry higher interest rates and are frequently utilized by borrowers with limited access to traditional banking credit.

Broader Economic Read-Through

The surge in card debt reflects a broader cooling of the domestic economy where wage growth has failed to keep pace with the rising cost of living. When consumers turn to cash advances, it signals that household savings are exhausted and that discretionary spending is likely to contract sharply in the near term. This shift in stock market analysis suggests that retail-exposed sectors in South Korea may face headwinds as consumer purchasing power diminishes.

Investors should monitor the following indicators to gauge the severity of this credit cycle:

- The monthly delinquency rate reported by the Financial Supervisory Service.

- Changes in the interest rate spreads applied to new card loan originations.

- Any regulatory intervention aimed at capping high-interest consumer debt.

The Path to Normalization

The immediate concern for the sector is whether this spike is a temporary reaction to seasonal factors or the beginning of a sustained trend of credit distress. If delinquency rates begin to climb in the second quarter, the industry will likely see a contraction in new loan originations as lenders prioritize balance sheet preservation over growth. The next major marker for this narrative will be the release of the first-quarter earnings reports from major credit card issuers, which will clarify how much of this debt is being classified as non-performing.

While the current data focuses on the volume of borrowing, the ultimate impact on the financial system will depend on the recovery rate of these assets. A sustained increase in credit risk could lead to a broader tightening of lending conditions across the geopolitical risk and market stability in the Indian subcontinent and regional financial corridors, as institutions look to hedge against potential defaults. Market participants should look for updates on capital adequacy ratios in the upcoming regulatory filings to determine if the sector is adequately prepared for a potential wave of defaults.