Stocks● Neutral

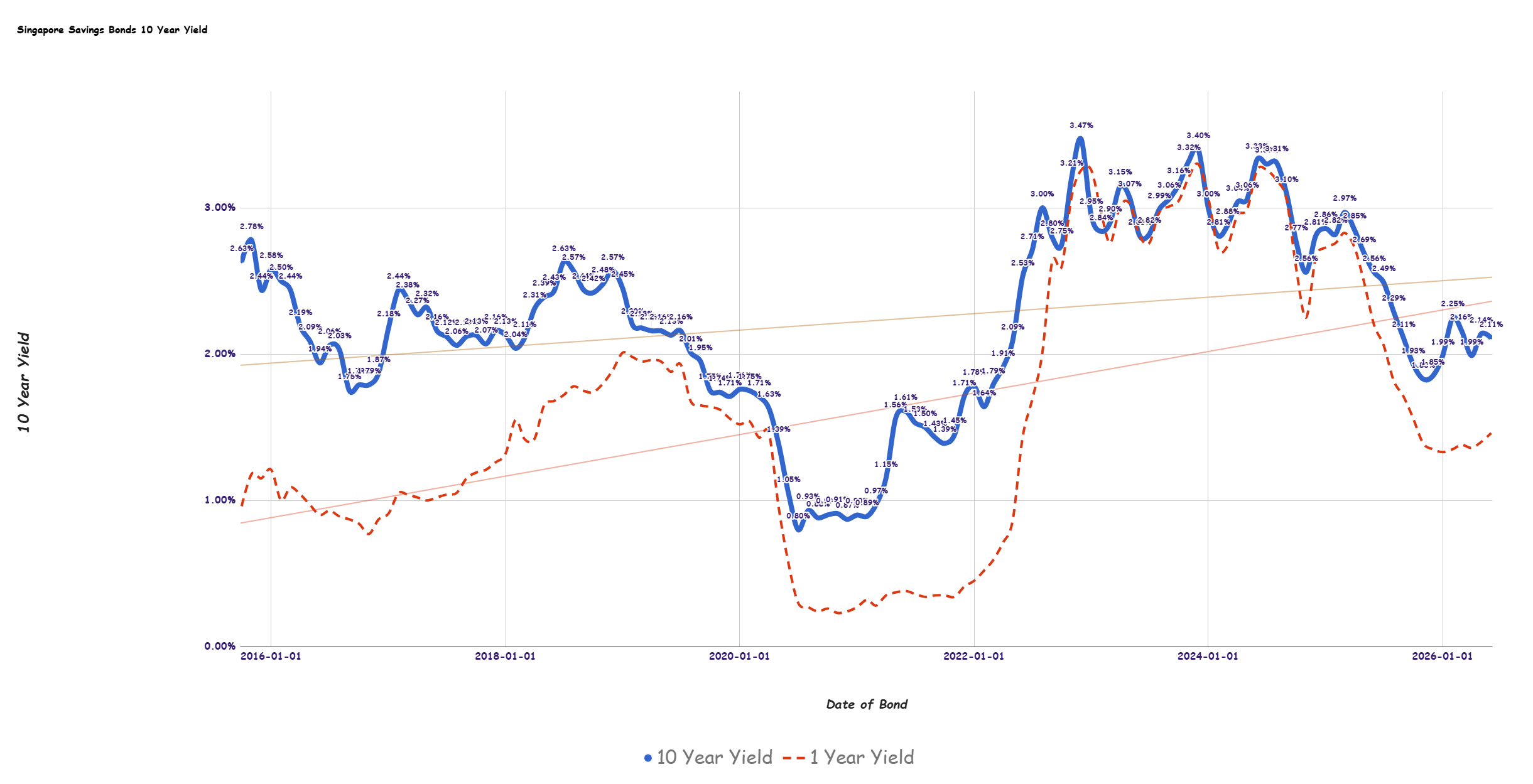

Singapore Savings Bonds June 2026 Yield Holds at 2.11%

The June 2026 Singapore Savings Bonds (SBJUN26 GX26060N) offer a 10-year yield of 2.11%. Investors should monitor allotment risks as demand impacts allocation.

Continue with

The June 2026 Singapore Savings Bonds (SSB), identified by ticker SBJUN26 GX26060N, offer a 10-year average annual yield of 2.11%. This issuance continues a period of relative stability in long-term rates for the instrument, though the underlying yield curve structure is shifting. Investors looking at shorter time horizons will note that the one-year yield for this tranche sits at 1.46%, a marginal increase from the 1.40% seen in the previous month's issue. While the 10-year headline rate remains the primary focus for long-term savers, the slight uptick in the one-year yield suggests a potential flattening of the curve compared to prior months.

Mechanism of the SSB Yield Curve

The Singapore Savings Bonds operate on a step-up interest structure, where the yield increases the longer the bond is held. The 2.11% figure represents the average annual return if the bond is held for the full 10-year duration. Investors should distinguish between this average and the actual cash flow received in the early years. Because the interest is paid semi-annually, the effective yield for an investor who chooses to redeem after only one year is significantly lower than the 10-year average. This mechanism is designed to incentivize long-term capital preservation rather than short-term liquidity, though the bonds remain redeemable on a monthly basis without penalty.

Allocation Risk and Demand Dynamics

One of the most misunderstood aspects of the SSB program is the allotment process. Unlike a standard market purchase where the price adjusts to clear the market, the SSB interest rate is fixed at the start of the subscription period. If total demand from applicants exceeds the issuance amount, the Monetary Authority of Singapore (MAS) implements a pro-rata or ceiling-based allocation. This creates a specific execution risk for investors: you may apply for the maximum allowable SG$200,000 but receive only a fraction of that amount. Historical data shows that during periods of high interest rate volatility or attractive relative yields, individual allotments can be slashed significantly, as seen in the August 2022 issue where the maximum allotment per person was capped at $9,000.