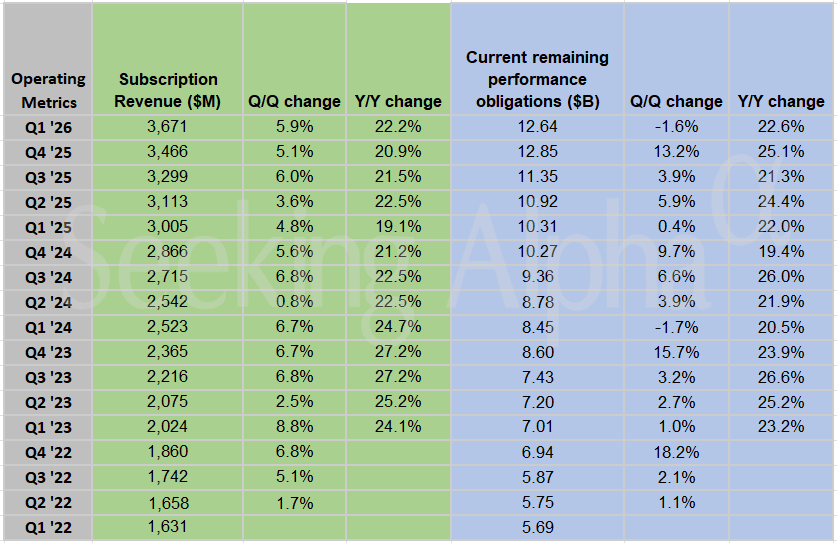

ServiceNow reported a 22% year-over-year increase in subscription revenue for the first quarter, signaling that enterprise demand for workflow automation remains resilient. This growth rate matches the performance observed in previous periods, suggesting that the company is successfully maintaining its scale while navigating a complex macroeconomic environment. The consistency in these figures provides a baseline for evaluating how the firm balances rapid expansion with the operational costs associated with large-scale software deployment.

Subscription Revenue and Enterprise Scaling

The ability to sustain a 22% growth rate in subscription revenue is a primary indicator of ServiceNow's position within the broader enterprise software ecosystem. As organizations continue to prioritize digital transformation, the demand for platforms that consolidate disparate IT and employee workflows remains high. This subscription-based model provides a predictable revenue stream, which is critical for NOW stock page as it continues to invest in its core platform capabilities. The stability of this growth suggests that enterprise clients are not yet pulling back on their long-term commitments to the platform, despite broader concerns regarding corporate spending efficiency.

Sector Read-Through and Competitive Positioning

ServiceNow's performance offers a specific read-through for the technology sector, particularly for firms focused on enterprise resource planning and automation. While some segments of the software market have faced pressure due to budget tightening, the sustained demand for ServiceNow's subscription services indicates that workflow automation is viewed as a necessity rather than a discretionary expense. This trend reinforces the importance of integrated software solutions in maintaining operational continuity for large-scale enterprises. The company's ability to retain its growth trajectory serves as a benchmark for other players in the stock market analysis space that rely on high-volume subscription renewals and new enterprise acquisitions.

AlphaScala Data and Future Markers

According to current AlphaScala data, ServiceNow holds an Alpha Score of 56/100, placing it in the Moderate category within the technology sector. This score reflects a balance between the company's consistent revenue growth and the valuation pressures inherent in the current market environment. The next concrete marker for investors will be the company's ability to maintain these subscription growth levels in the face of potential shifts in enterprise IT budgets during the second half of the year. Monitoring the renewal rates and the average contract value in upcoming filings will be essential to determine if this 22% growth rate represents a sustainable plateau or if it faces headwinds from increased competition in the automation space.