The closure of the Strait of Hormuz to most commerce has rerouted energy flows through Saudi Arabia's Red Sea coast, generating a surge in oil revenue. Saudi Arabia's oil export revenue hit a more than three-year high of $24.7 billion in the first full month of the war. The kingdom is simultaneously advancing Crown Prince Mohammed bin Salman's $1.3 trillion economic transformation plan. The mechanism behind this windfall is not luck. A decade-old contingency pipeline and a highway network turned Saudi Arabia into the Gulf's transit backstop.

The war has slowed economic growth across the Gulf and driven a jump in defense spending. Yet Saudi Arabia's ability to monetise its pre-war infrastructure has produced a clear near-term advantage. The question is whether that advantage survives a potential reopening of Hormuz.

"Saudi Arabia has shown it is the indispensable Red Sea backstop," said Hesham Alghannam, a Riyadh-based scholar at the Malcolm H Kerr Carnegie Middle East Center.

Saudi Arabia's $24.7B War Dividend

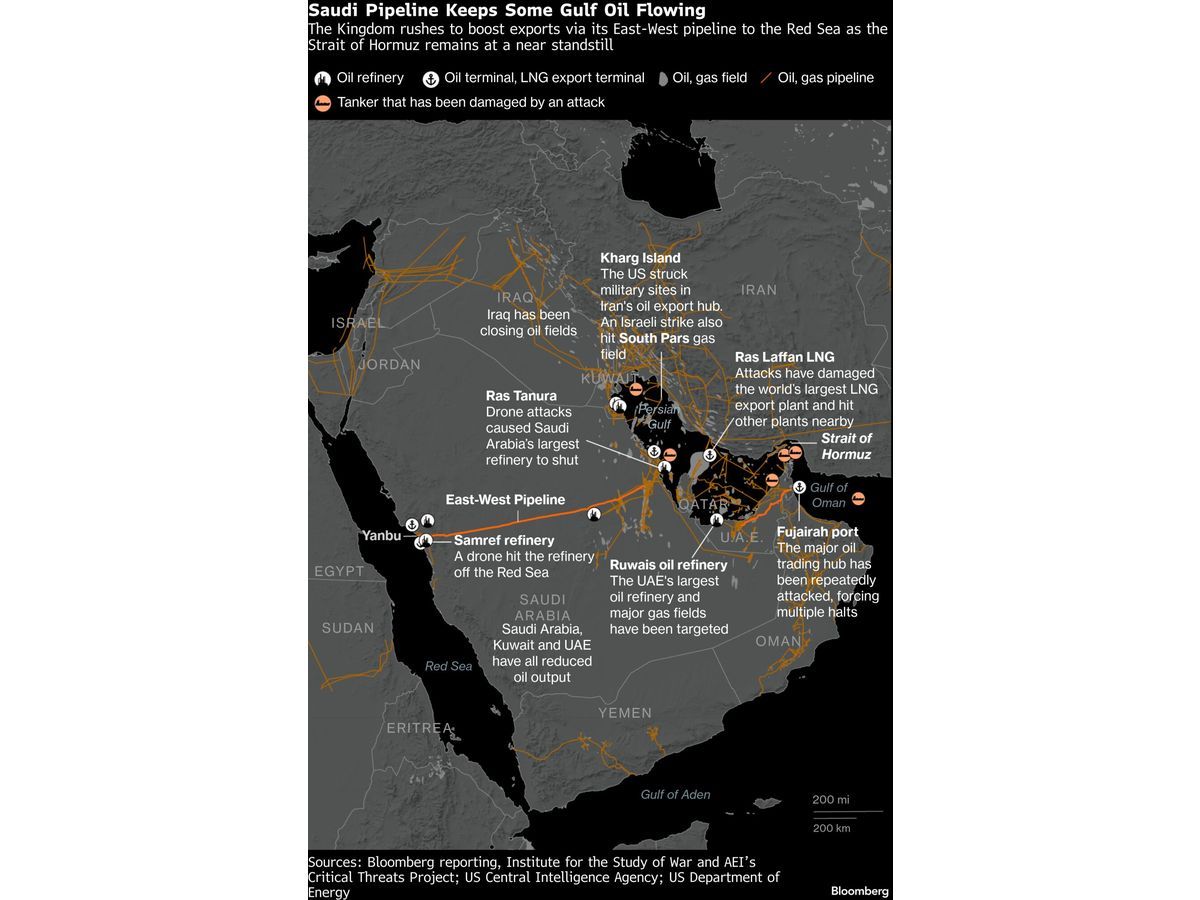

Oil export revenue jumped in the first month of the conflict because Saudi Arabia could ship crude without using the Hormuz chokepoint. Most Saudi crude exports had passed through the strait before the war. The East-West pipeline, a contingency plan built decades ago, now carries a significant portion of production to the Red Sea. That route avoids the war risk and insurance premiums that have made Hormuz passages prohibitively expensive.

Practical rule: Saudi oil revenue gains are real but contingent on Hormuz remaining closed. The premium shrinks if rival routes erode the kingdom's pricing power.

The Pipeline That Changed the Math

The East-West pipeline has a capacity of about 5 million barrels per day. During peacetime, much of that capacity sat idle as tankers loaded directly from Ras Tanura and shipped through Hormuz. The war changed utilisation rates. Satellite data and shipping filings show Red Sea crude loadings rising sharply. The pipeline alone would not have been enough. Saudi Arabia's highway system allowed thousands of trucks to ferry fertilizers and consumer goods from the Gulf coast to Red Sea ports. That created a multimodal corridor that competitors cannot replicate overnight.

Red Sea Corridor vs. Hormuz Closure

The Red Sea has become the Gulf's primary exit point for energy and cargo. Saudi ports on the Red Sea handle crude, refined products, and container traffic that previously moved through the UAE. The shift has boosted port revenues and created demand for logistics services inside the kingdom.

The corridor faces two risks. First, the Strait of Hormuz may reopen. Senior US officials said Sunday that the US and Iran are closing in on a deal that would reopen the strait. President Donald Trump insisted he would not "rush" into an agreement. A reopening would reduce the premium Saudi Arabia collects on its Hormuz-free exports.

Second, the Red Sea itself carries security risks from Houthi attacks and naval deployments. For now, Saudi shipping continues without major disruption.

Competition from UAE and Oman

The source reports that alternative trading routes are developing on the eastern coast of the United Arab Emirates as well as in Oman. The UAE is setting up an export hub on its east coast and accelerating construction of a pipeline to Fujairah port on the Gulf of Oman. The goal is to double crude export capacity. A spokesperson for the UAE pointed to official comments highlighting the pipeline expansion and efforts to bolster supply chains.

Oman has launched a new trade corridor with the Emirate of Sharjah. Omani ports benefit from shipping through the Arabian Sea, which avoids both the Red Sea and the Strait of Hormuz. These routes compete directly with Saudi Arabia's Red Sea corridor.

Key competitive pressures to track:

- UAE Fujairah pipeline: capacity expansion timeline and crude throughput.

- Oman-Sharjah corridor: container and bulk cargo volumes.

- Qatar energy flows: potential for Qatar to use alternative shipping routes for LNG.

IMF Growth Forecast and Defense Spending Costs

The International Monetary Fund in April lowered its projection for Saudi expansion by 0.9 percentage points to 3.1% for 2026. That reduction was the second lowest among Gulf countries, trailing only Oman. Growth slowed in non-oil sectors even as oil revenue surged.

"For Saudi Arabia, each month of fighting costs about 1.5% of GDP in extra spending," Ziad Daoud, chief emerging markets economist for Bloomberg Economics, wrote in May. "For most of its neighbors, the bill is probably higher."

Defense and logistics spending have risen sharply. The Saudi government did not respond to a request for comment. The war has slowed growth across the Gulf, yet Saudi Arabia's ability to capture oil revenue and transit fees partially offsets the damage. The question is whether the gains from contingency planning last long enough to fund structural reforms. They could vanish quickly if Hormuz reopens.

What Confirms or Weakens the Saudi Thesis

Two data points would confirm the Saudi advantage is structural. First, sustained high utilisation of the East-West pipeline even after a Hormuz deal. If the pipeline becomes the preferred route due to lower insurance costs, Saudi Arabia retains the benefit. Second, non-oil transit volumes through Saudi Red Sea ports rising month over month, indicating supply chain inertia.

Two factors would weaken the thesis. First, a US-Iran deal that reopens Hormuz quickly and without ratcheting sanctions back up. Second, UAE and Oman capturing enough routing share to bid down Saudi port fees, reducing the economic benefit.

For commodity traders, the read-through is straightforward. Saudi crude discounts or premiums relative to Brent will reflect Hormuz risk. If Hormuz reopens, the convenience yield Saudi oil carries today will compress. Watch crude oil profile for real-time changes in Saudi-Brent spreads and the commodities analysis section for weekly flow data. A parallel case occurred in 2023 when oil tumbled 5% on US-Iran deal reports. History may repeat if negotiators finalise an agreement.