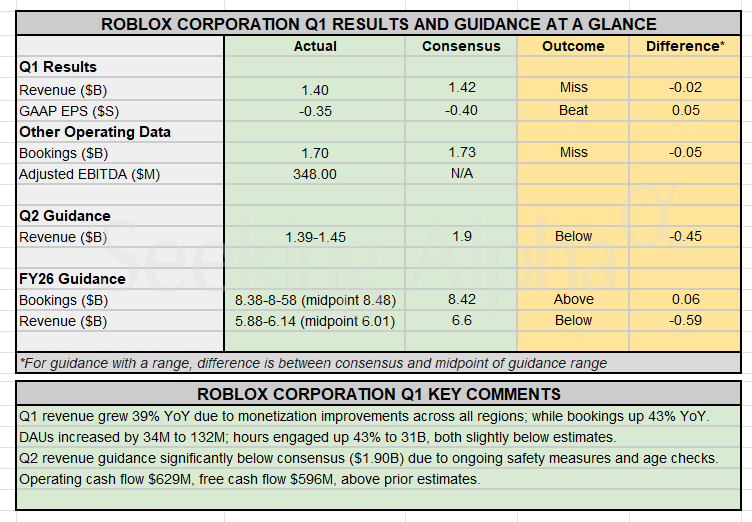

Roblox Corporation reported a mixed first quarter for 2026, characterized by a notable beat in bookings alongside revenue figures and forward-looking guidance that fell short of expectations. While the company demonstrated resilience in cash flow generation and earnings per share, the underlying metrics regarding user growth and revenue recognition suggest a period of moderation. The discrepancy between bookings and revenue highlights the complexities of the company's subscription-based model as it navigates shifting user engagement patterns and the implementation of new safety restrictions.

Bookings Performance and Revenue Moderation

The primary point of tension in the latest print is the divergence between top-line revenue and bookings. Bookings, which represent the sale of virtual currency and remain a critical indicator of platform health, outperformed analyst estimates. This suggests that the core monetization engine remains functional despite broader headwinds. However, the reported revenue failed to meet consensus targets, indicating that the conversion of these bookings into recognized revenue is facing friction. This lag is often tied to the timing of virtual good consumption and the amortization of user spending over the expected life of the player.

User growth metrics also signaled a cooling trend. The platform has historically relied on aggressive expansion of its daily active user base to drive scale. The recent data indicates that this expansion is encountering a plateau, exacerbated by the introduction of safety-focused features. While these measures are intended to improve the long-term quality and safety of the ecosystem, they have created short-term hurdles for user acquisition and retention. The company is now balancing the necessity of a secure environment with the requirement for consistent engagement growth.

Guidance and Operational Outlook

The company's forward guidance for the remainder of the year reflects a cautious stance. Management has adjusted its outlook to account for the current moderation in user activity and the ongoing impact of safety-related policy changes. This conservative posture suggests that the company does not anticipate an immediate rebound in growth rates, opting instead to focus on operational efficiency and cash flow stability. For investors, this shift marks a transition from a growth-at-all-costs narrative to one centered on sustainable margin management and disciplined capital allocation.

AlphaScala currently tracks the company with an Alpha Score of 27/100, labeling the stock as Weak within the Communication Services sector. Detailed performance metrics and historical data for the company can be found on the RBLX stock page. This score reflects the current volatility and the challenges inherent in the company's transition toward more stable, albeit slower, growth phases.

As the company moves into the second quarter, the focus will shift to how effectively it can integrate its safety protocols without further eroding user engagement. The next concrete marker for the market will be the subsequent quarterly filing, which will provide the first clear evidence of whether the current moderation is a temporary adjustment or a structural change in the platform's growth trajectory. Investors will be monitoring the relationship between bookings and revenue to determine if the monetization gap begins to narrow or if the current trend of revenue underperformance persists through the fiscal year.