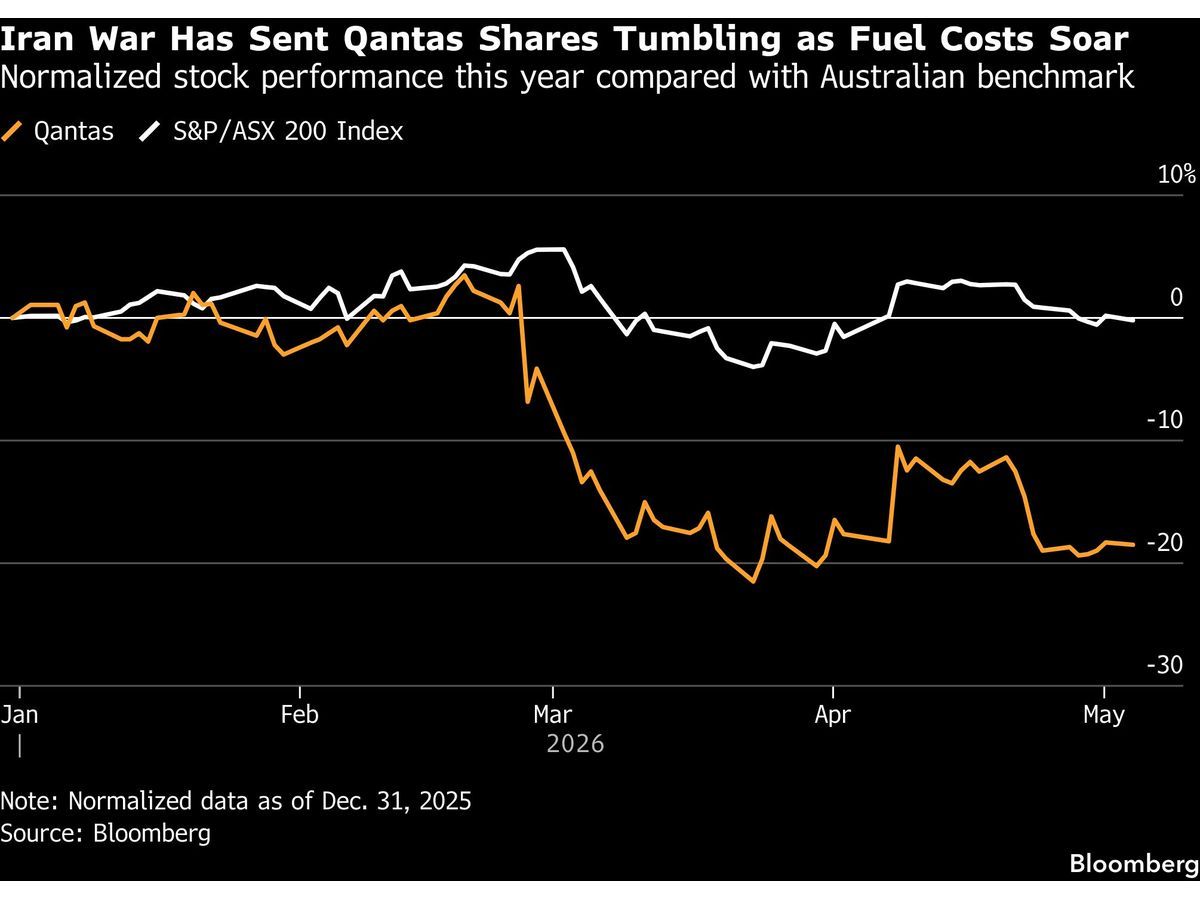

Qantas Airways Ltd. CEO Vanessa Hudson has signaled a shift in the airline's operational outlook, expressing increased optimism regarding jet fuel availability through mid-June. This development follows a period of intense volatility in energy markets triggered by the ongoing conflict in the Middle East, which began in late February. While the broader aviation sector continues to grapple with the inflationary pressures of higher energy costs, the ability of Qantas to secure supply commitments on a rolling six-week basis suggests that the immediate risk of fuel shortages has moderated.

Diversification of Supply Chains

The core of this supply stabilization lies in a geographic pivot for fuel procurement. Historically, Qantas relied heavily on refineries and suppliers located in Japan, China, and South Korea. The disruption of traditional trade routes and the geopolitical instability in the Middle East forced a rapid reorientation of these logistics. Hudson confirmed that suppliers are now sourcing significantly higher volumes of fuel from the Americas, specifically citing the United States and Mexico as critical contributors to the current supply chain. This diversification is the primary mechanism allowing the airline to maintain its operational rhythm despite the ongoing regional conflict.

For investors, the transition from Asian-centric supply to Western-hemisphere sourcing represents a fundamental change in the airline's cost structure and logistical risk profile. While the fuel bill for the fiscal second half ending in June remains elevated—projected between A$3.1 billion and A$3.3 billion compared to an initial estimate of A$2.5 billion—the reliability of the supply chain appears to have returned to pre-conflict standards. The return to a rolling six-week commitment cycle is a specific indicator that the market for refined products is finding a new equilibrium.

Demand Resilience and Capacity Management

Despite the upward pressure on ticket prices necessitated by these higher fuel costs, Qantas reports that consumer appetite for both domestic and international travel remains robust. Hudson noted that demand is holding up across the entire network, suggesting that the price elasticity of air travel in the current environment is lower than some analysts previously feared. This resilience allows the airline to pass through a portion of the increased energy costs to the end consumer without triggering a significant contraction in volume.

However, the airline is not operating at full capacity. To manage costs and navigate the logistical complexities of the current environment, Qantas has extended service adjustments through the end of September. These measures include a 5% reduction in domestic services, primarily impacting Qantas and Jetstar flights between major Australian cities, as well as reduced flight frequencies to New Zealand. Furthermore, the airline has maintained extra direct flights to Europe, a strategic move designed to bypass the Middle East, thereby mitigating the risk of further airspace closures or regional volatility.

Sector Read-Through and Competitive Positioning

The operational challenges faced by Qantas are mirrored across the broader aviation industry. Smaller rival Virgin Australia Holdings Ltd. is reportedly considering extending its own flight cuts into the third quarter, indicating that the supply-side constraints are not unique to the national carrier. The industry-wide trend of capacity discipline serves as a buffer against the volatility in commodities analysis markets, particularly as Persian Gulf Escalation Forces Crude Oil Price Rebound remains a persistent threat to margins.

While the aviation sector deals with these energy-linked headwinds, other real estate and infrastructure-heavy sectors are also recalibrating. For instance, Welltower Inc. currently holds an Alpha Score of 52/100, reflecting a mixed outlook as broader market participants weigh the impact of sustained inflation on capital-intensive industries. The ability of a firm to secure its supply chain, as Qantas has done with its fuel commitments, is becoming a primary differentiator for valuation in a high-cost environment.

Risks to the Operational Thesis

While the current outlook is more optimistic than it was in April, the situation remains fragile. The conflict in the Middle East is dynamic, and the recent exchange of fire between the US and Iran in the Persian Gulf serves as a reminder that energy prices remain sensitive to geopolitical flare-ups. Any further escalation that threatens maritime transit or refinery operations in the region could quickly reverse the progress made in diversifying supply chains.

Investors should monitor the duration of the current service cuts as a proxy for management's confidence in long-term fuel price stability. If Qantas or its peers begin to restore capacity before the end of the third quarter, it would indicate a belief that the energy market has stabilized. Conversely, a further extension of flight cuts would suggest that the cost of fuel or the difficulty of procurement is expected to remain a structural drag on profitability for the remainder of the fiscal year. The current stability is built on a six-week horizon; until that window expands, the sector remains vulnerable to sudden shifts in the WTI Crude Oil Technical Setup Ahead of Key Data Catalysts.