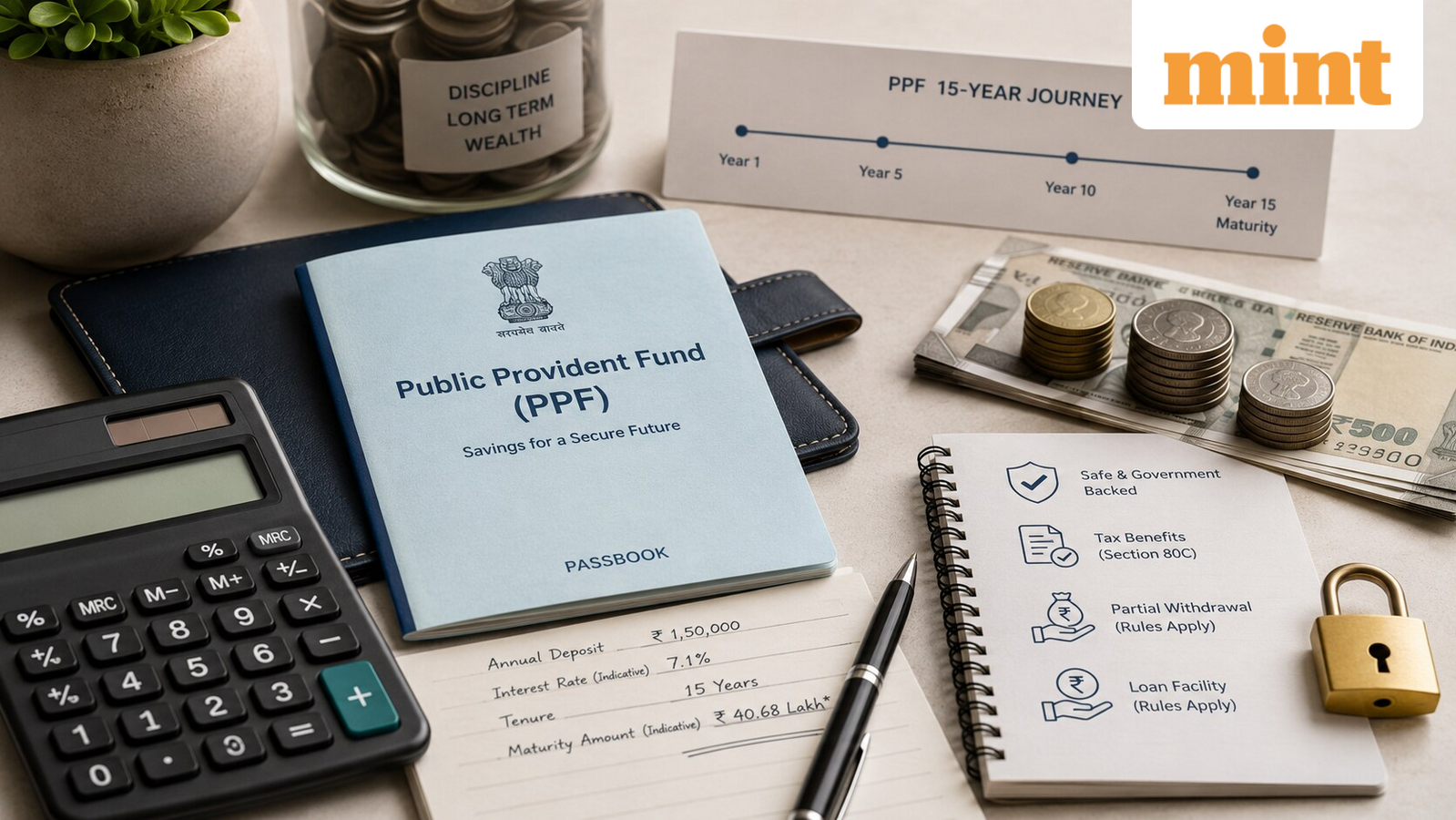

A Public Provident Fund account locks savings for 15 years. That is the deal. You get tax-free compounding and EEE status in exchange for keeping the money inside. Life, however, does not always cooperate. Hospital bills, education costs, a job offer abroad – the PPF rules allow early access in specific situations. The catch is a hidden penalty that most account holders discover only when they apply.

When the government lets you close early

The Finance Ministry permits premature closure for three reasons: treatment of a serious illness affecting the account holder, spouse, children, or dependent parents; higher education expenses; and a change in residency – either a work visa or permanent relocation abroad. The account must have completed five financial years from the end of the year it was opened. That means a PPF opened in the 2020-21 financial year becomes eligible for early closure only after March 31, 2026.

The interest penalty is retrospective

Close early and the interest earned from day one gets recalculated at a rate 1% lower than what was originally credited. This is not a flat fee. It is a retrospective cut that erodes returns across the entire life of the account. If the account earned 7.1% annually, the effective yield drops to 6.1% for every year the account was open. On a balance of ₹5 lakh held for six years, that difference costs roughly ₹3,500 in lost interest – and the gap widens the longer the account was active before closure.

Partial withdrawal is almost always the better move

Starting from the sixth financial year, you can withdraw up to 50% of the balance that stood at the end of the fourth preceding year. No penalty applies. The interest rate stays unchanged. The account remains active and the remaining balance continues to compound tax-free. If you need ₹2 lakh for a medical bill, a partial withdrawal preserves the compounding on the rest. The only cost is the opportunity cost of the withdrawn amount. That is a far better trade than losing 1% on the entire corpus.

How to process the withdrawal

Fill out Form C. You can download it from your bank's website or collect a physical copy from the branch. Attach supporting documents – medical certificates, admission letters, visa proof. Submit in person or online if the bank offers digital PPF services. The bank or post office processes the request and credits the amount to your linked savings account.

Tax treatment stays favorable

PPF enjoys Exempt-Exempt-Exempt status. Contributions qualify for deduction under Section 80C up to ₹1.5 lakh per year. Interest earned and withdrawal amounts are tax-free. That includes partial withdrawals and premature closure, though premature closure triggers the interest penalty. The tax advantage is real. It only works if you can keep the money inside for the full 15-year term. If you anticipate needing liquidity before year 15, balance PPF with a more liquid debt instrument like an ELSS fund or a bank recurring deposit. The five-year lock-in is not negotiable. Plan accordingly.