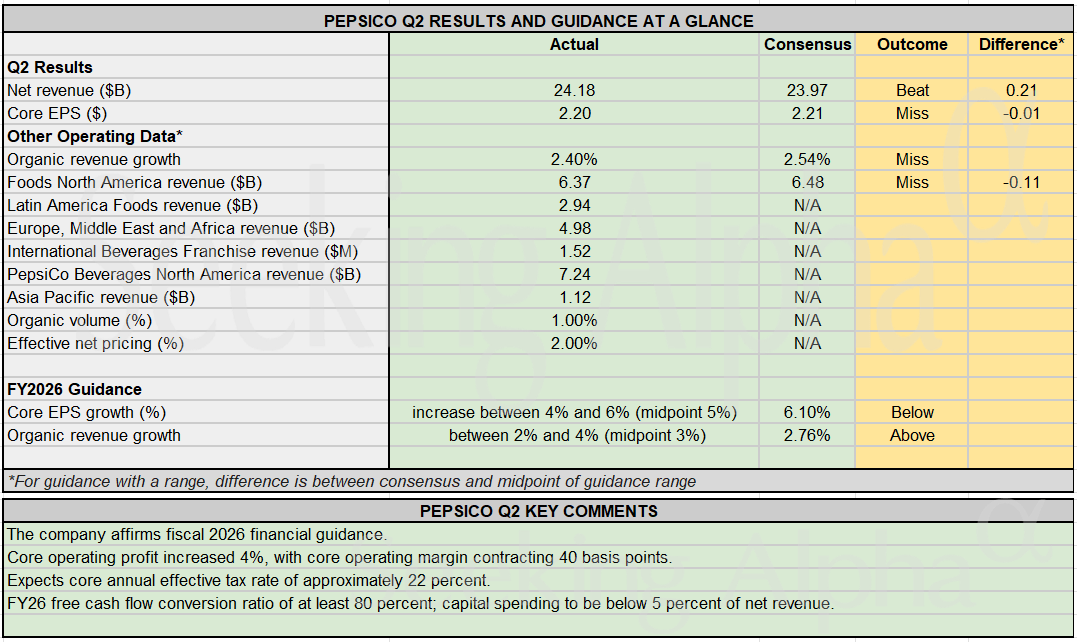

PepsiCo's second-quarter revenue topped analyst estimates. Core earnings per share and organic sales growth both missed. The company reaffirmed its full-year 2026 outlook.

Revenue came in above expectations, helped by pricing actions and favorable mix in North American beverages and international markets. Core EPS fell short of consensus, weighed by higher commodity costs and currency translation. Organic growth, which strips out acquisitions and foreign exchange, also lagged forecasts. The company said volume trends were softer in some categories.

The affirmed guidance indicates management expects the headwinds to be temporary, according to the release. The miss on two key profit metrics leaves the margin story unresolved. Input cost inflation, particularly in grains and packaging, has been a persistent drag. Currency headwinds from a stronger dollar also cut into reported earnings.

The snack business, which accounts for roughly half of PepsiCo's revenue, saw slower volume growth in North America. The beverage segment performed better on pricing. Unit case volumes remained under pressure in some markets.

The revenue beat was broad-based. The North American beverage segment and the international division both contributed. Pricing actions offset some volume weakness. The Frito-Lay North America segment saw slower volume growth. Quaker Foods continued to face headwinds from recall-related disruptions.

Core EPS missed by a few cents, according to the release. Higher cost of goods sold and unfavorable currency drove the miss. Operating margins contracted slightly year-over-year.

Organic sales growth came in below the company's long-term algorithm. The company said volume trends were softer than expected.

PepsiCo's international business contributed to the revenue beat, with growth in Latin America and Asia. Currency headwinds partially offset those gains. The company's international segment remains a growth driver. Volatility in emerging markets adds uncertainty to the outlook.

The company's balance sheet remains solid. PepsiCo generated healthy cash flow from operations in the quarter, supporting its dividend and share repurchase program. Management has prioritized returning cash to shareholders while investing in the business.

The reaffirmed FY26 outlook implies that management expects the second half to improve. The first-half performance sets a higher bar for the back half. Investors will watch for any change in tone on the earnings call.

Key questions for the call include the trajectory of input costs and the pace of volume recovery in North America. Any commentary on consumer health and trade-down behavior will be closely watched.

The pattern of revenue beats paired with earnings misses is a recurring theme this season, as discussed in our analysis of the tightrope market. For PepsiCo, the next quarterly report will show whether cost pressures ease and volumes recover.

PepsiCo reports in U.S. dollars and faces headwinds from a strong dollar. The company's next quarterly report is due in October.