Back to Markets

Commodities● Neutral

Oil Surge Resets Treasury Rate Path After Iran Talks Stall

Treasury yields climb as crude jumps 8.5% on Iran talks breakdown, repricing Fed hike expectations. ISM data adds pressure. Next catalyst: EIA inventory.

Continue with

Treasuries fell Monday as an impasse in US-Iran negotiations sent crude oil surging and revived the inflation-risk narrative. The move challenges the recent rally built on optimism about a reopening of the Strait of Hormuz.

The Oil-Yield Mechanism: Geopolitical Catalyst vs. Economic Backdrop

US government bond yields are tracking crude oil prices with unusual precision. Since the US military action against Iran in late February, the relationship has been inverse: when oil climbs, yields rise on inflation and rate-hike expectations. When oil falls, yields drop.

Monday’s session was a textbook example. US benchmark crude surged 8.5% at its intraday peak before settling with a 5.5% gain. Treasury yields followed, climbing five to nine basis points across maturities before settling one to four basis points higher on the day. The 10-year note yield touched 4.51% before closing near 4.47%.

The Iran Talks Reversal

The catalyst was a report from Iran’s semi-official Tasnim news agency that Tehran would suspend message exchanges with Washington in protest over Israeli actions. The market partially recovered after the US stated that Israel and Hezbollah had agreed to stop attacking each other in Lebanon and that talks with Iran were continuing.

Gennadiy Goldberg, head of US rates strategy at TD Securities, described the market’s vulnerability: “The market has been very optimistic in its assessment over the past week that the US-Iran agreement is a done deal. This leaves markets highly sensitive to any negative news, particularly today’s headlines that Iran has stopped talking to the US.”

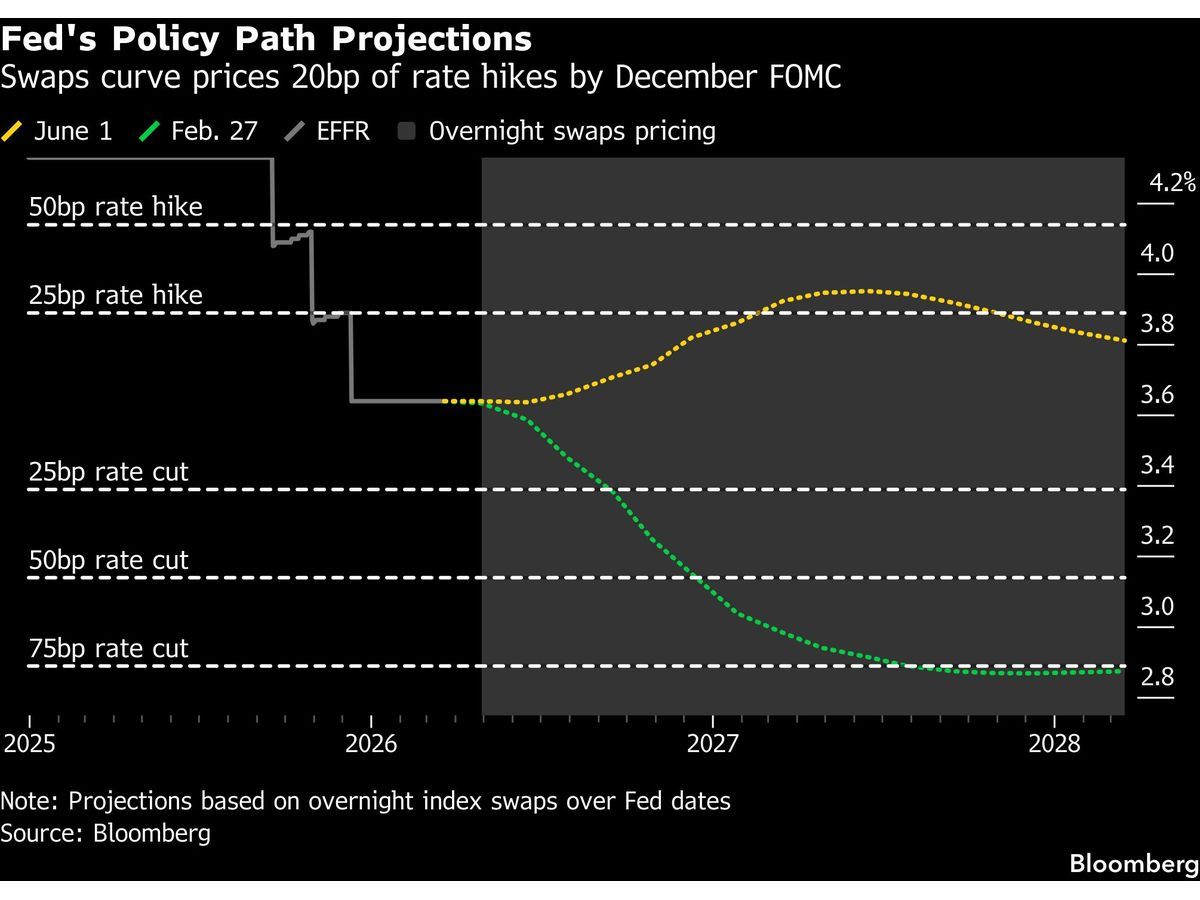

Rate-Hike Expectations Reappear in Swap Markets

The oil-driven yield move has a direct consequence for Fed policy expectations. Interest-rate swaps now show traders have fully priced in a rate hike by March 2027, with about a 50% chance of a move as early as October. That is a sharp reversal from the dovish positioning that dominated earlier in the year.

ISM Manufacturing Adds Pressure

Treasuries also absorbed pressure from Institute for Supply Management survey data showing US manufacturing activity expanded in May at the fastest pace in four years. The report underscored the resilience of the US economy, feeding doubt that the current Fed policy rate range of 3.5% to 3.75% is restrictive enough to cool inflation.

Curve Flattening Reflects Front-End Tightening

Shorter and intermediate Treasuries underperformed as rate-hike expectations built. The gap between five-year and 30-year yields temporarily narrowed to less than 80 basis points, the smallest spread in more than a year. A flattening curve typically signals that the market expects the Fed to tighten sooner than previously anticipated.

Sector Read-Through: Energy, Transport, and Consumer Exposure

The oil-Treasury linkage creates a clear read-through for several sectors.

Energy Producers: Direct Beneficiaries

Higher crude prices directly benefit upstream producers. The read-through is strongest for companies with exposure to US shale production and Middle East operations that can capture the higher per-barrel revenue. The risk is that sustained oil above $90 per barrel invites political pressure for price controls or windfall taxes.