West Texas Intermediate crude steadied near $92 a barrel after its biggest single-day gain in about a month. The previous session saw WTI add more than 5% on a report that Iran had halted negotiations with Washington in protest of Israeli attacks in Lebanon. Brent crude settled just under $95. The price action reflects a market that had been pricing in a best-case resolution for the Strait of Hormuz and now faces a return of the same transport risk that drove oil to multi-year highs earlier this year.

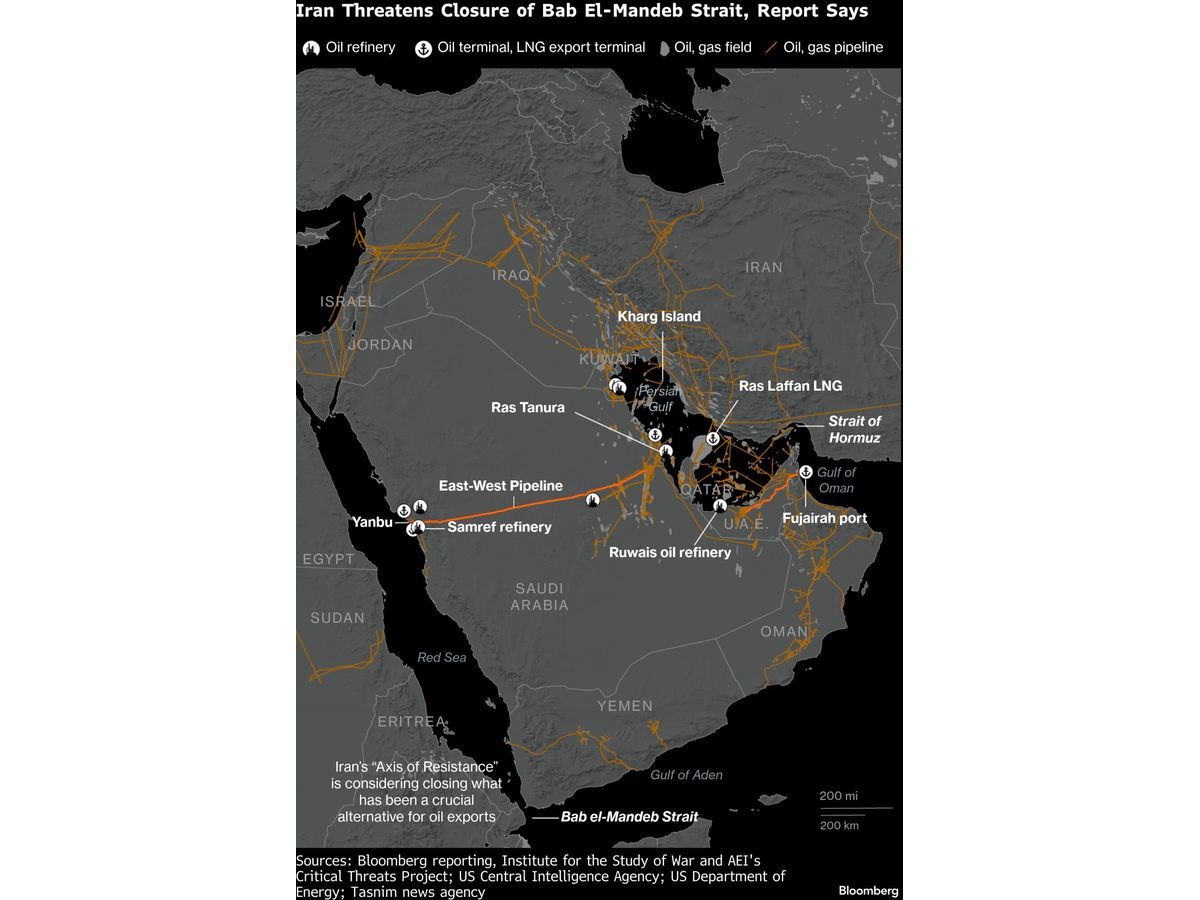

US President Donald Trump told ABC News that a memorandum of understanding with Iran to reopen the Strait of Hormuz could happen within the next week, adding that the US still had “to get a few more points” before a deal. That statement contradicted a report from Iran’s semi-official Tasnim news agency, which said Tehran and its regional proxies had placed on their agenda the complete closure of both the Strait of Hormuz and the Bab el-Mandeb Strait – the critical alternative route for oil exports from the region. The conflicting signals have left traders without a clear anchor for the risk premium.

Trump and Israeli Prime Minister Benjamin Netanyahu also offered differing accounts of a call about the fighting in Lebanon. A US-brokered ceasefire between Tel Aviv and Hezbollah should be extended from Beirut to include all Lebanese territories, the Lebanese presidency said in a post, with more negotiations scheduled for Tuesday and Wednesday.

“Further indications that the parties are no longer actively negotiating would also remove some of the security blanket the market has been relying on to price toward a best-case outcome,” said Rebecca Babin, senior energy trader at CIBC Private Wealth Group. “We’ve seen plenty of back-and-forth throughout this conflict, and nothing has been set in stone.”

Hormuz Risk Returns to the Forefront

The Strait of Hormuz is the world’s most important oil chokepoint, handling about 20% of global petroleum consumption according to the US Energy Information Administration. Any credible threat to its closure forces immediate repricing across crude futures, tanker rates, and energy equities. The Tasnim report asserted that both Hormuz and Bab el-Mandeb – the southern entrance to the Red Sea – were on the agenda for closure.

The naive read versus the better market read

The simple interpretation is that oil jumped because Iran walked away from talks. The better market read is that the market had been steadily discounting the risk premium over the past month as negotiations progressed. Brent fell from above $100 to just above $90 in that period. Monday’s surge recaptured only part of that decline, which suggests traders are still uncertain whether the ceasefire will collapse entirely.

What changed is the header risk: the probability of a full Hormuz closure went from near-zero to a real tail scenario again. The uncertainty is not just about Iran’s willingness to talk. It is about whether the negotiations have any binding effect on Tehran’s proxies, who operate independently on the ground in Yemen (controlling Bab el-Mandeb) and in the Persian Gulf.

Why the Ceasefire Uncertainty Matters for Oil Inventories

Oil inventories in the US and Europe have been drawing down for weeks, reflecting strong refining margins and limited OPEC+ spare capacity. A sustained disruption at Hormuz would pull tankers out of the market as they wait for passage, effectively removing floating storage capacity and squeezing prompt supply.

The inventory signal to watch

If the negotiations continue to stall, the WTI-Brent spread could widen as Brent carries a higher Hormuz risk premium. The Brent-Dubai spread would react first, because Dubai crude is most exposed to Persian Gulf loadings. Traders should track the weekly EIA crude inventory report for a build in the US Gulf Coast. That would indicate that barrels are being diverted away from the Atlantic Basin and into domestic storage, a sign of logistical strain.

Sector Readthrough: Energy Equities and Shipping

The readthrough for energy equities depends on whether the risk premium sticks. For integrated oil majors with diversified production, the direct impact is limited because they lift crude from multiple basins. For US shale producers concentrated in the Permian, the higher WTI price is a direct margin benefit. A sustained rally would require Brent to stay above $95 to keep the arbitrage open for exports.

Shipping rates and insurance costs

Tanker owners face the most immediate exposure. War risk insurance premiums for vessels transiting the Persian Gulf have already risen. A formal closure of Hormuz would push VLCC rates sharply higher as ships are forced to take longer routes around Africa. The Bab el-Mandeb alternative carries its own Houthi attack risk, as seen in recent Red Sea incidents. The composite effect is that shipping costs for Gulf crude will rise even without a full closure, simply because of elevated uncertainty.

Directly affected peers

Companies with direct exposure to the Strait of Hormuz include tanker operators such as Frontline and Euronav, though neither is mentioned in the source. For the broader sector, the readthrough is clear: any sustained disruption to Gulf flows benefits US crude exporters like Exxon Mobil and Chevron, while refiners on the US Gulf Coast that process heavier Middle Eastern grades face feedstock shortages. That dynamic is visible in the crack spread widening for light-sweet crude versus sour crude.

What Confirms or Weakens the Setup

Three signals will determine whether the risk premium fades or compounds.

- Confirmed talks resumption: If Trump and Iranian officials schedule a face-to-face meeting, the premium will decay quickly, likely retracing back toward the $88-$90 range for WTI.

- Escalation in the Strait: Any physical incident – a tanker inspection, a mine detection, or a military intercept – triggers immediate pricing of the closure tail and could send WTI back above $100.

- US inventory builds: If EIA data shows crude stocks rising on diverted flows, the physical market is already adjusting, which caps the upside for front-month futures even if the risk premium stays elevated.

Traders using USO to track WTI should consider that the ETF rolls futures contracts. A persistent backwardation caused by spot scarcity would add a positive carry cost. For options traders, volatility skew in Brent options has already shifted toward out-of-the-money calls, reflecting demand for upside protection.

Bottom line for traders: The Hormuz risk is binary and unresolved. Price into the uncertainty only if you have a view on the negotiation outcome – not on oil fundamentals alone, because supply and demand are currently in balance without a disruption. The next concrete marker is the outcome of the Lebanese ceasefire talks on Tuesday and Wednesday. If they stall, expect the energy sector to reprice higher across equities and futures.

Internal links: crude oil profile | commodities analysis