Haley Sacks, the financial educator known as Mrs. Dow Jones to a million-plus social media following, appeared on TODAY to promote her new book "Future Rich Person" and outline a set of personal-finance principles. The segment distilled her approach into three actionable tips: negotiate a higher salary, invest rather than save, and adopt what she calls the IBIZA mindset. For a retail audience that often treats financial media as a direct instruction manual, the appearance matters. It will shape how a large cohort of new earners allocates capital in the coming months.

Salary Negotiation as a High-Return Trade

Sacks frames a salary increase as the highest-return move a young professional can make. The logic is straightforward: a $5,000 raise secured early compounds across decades of earnings, 401(k) contributions, and future job benchmarks. The market read is less about the negotiation tactic and more about the discount rate embedded in the advice. A salary bump is a guaranteed, tax-inefficient cash flow stream. It carries no correlation to equity markets, no duration risk, and no liquidity premium. In portfolio terms, it functions like a zero-volatility bond with an infinite maturity, except the principal is your own labor.

That structure makes the advice sound. The execution risk, however, is high. Negotiation outcomes depend on industry wage rigidity, employer budget cycles, and the worker's BATNA. Sacks' followers who internalize the message without a concrete walk-away alternative may overestimate their leverage. The better market read: treat the salary negotiation as an option on future earnings, not a sure thing. The premium is the preparation and the risk of a strained relationship. The payoff is asymmetric only when the BATNA is real.

The Saving-to-Investing Shift and Its Hidden Costs

The second pillar, investing rather than saving, is a staple of financial-influencer content. Sacks' version pushes followers to move cash from deposit accounts into assets that outpace inflation. The naive interpretation is that savings accounts are a guaranteed loss of purchasing power. The better market read acknowledges that cash is not just a returnless asset; it is a liquidity option that protects against forced selling of risk assets during a drawdown.

A 2022-style equity decline of 20% combined with a job loss turns a fully invested portfolio into a source of realized losses. The saver with six months of expenses in a high-yield account avoids selling the dip. The investor who followed the "invest rather than save" rule without a liquidity buffer crystallizes a permanent impairment. Sacks' framework likely assumes an emergency fund exists. The segment summary does not specify the sequencing. For the market, the risk is that a wave of new retail participants interprets the advice as a directive to go all-in on equities, reducing the cash cushion that stabilizes household balance sheets during recessions.

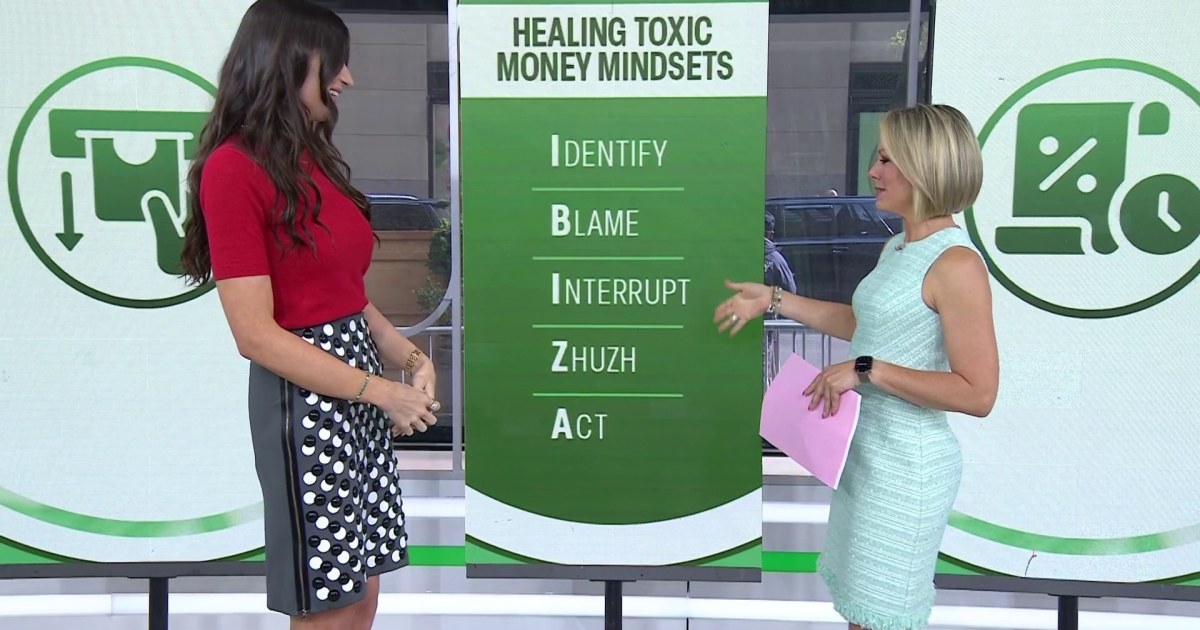

The IBIZA Mindset: A Behavioral Framework Without a Backtest

The segment references an IBIZA mindset without defining the acronym. In the absence of a detailed breakdown, the concept functions as a behavioral wrapper. Most personal-finance frameworks of this type aim to reduce impulsive spending, automate savings, and reframe consumption as a trade-off against future freedom. The market-relevant question is whether the mindset produces a measurable shift in savings rate or equity allocation among her followers.

Behavioral nudges work best when they are paired with commitment devices: automatic payroll deductions, default enrollment in target-date funds, or lock-up periods. Without those mechanisms, the IBIZA mindset risks becoming a feel-good label that does not survive a market correction or a lifestyle-inflation event. The practical edge for someone building a watchlist is to track flows into broad-market ETFs favored by first-time investors. If Sacks' book drives a measurable uptick in account openings or recurring deposit programs at platforms like Robinhood or Fidelity, the marginal bid for equities could show up in weekly flow data for funds such as SPDR S&P 500 ETF Trust (SPY) or Vanguard Total Stock Market ETF (VTI).

Equity ETF Flows as the Confirmation Signal

The appearance gives a clear signal about the narrative that will reach millions of new earners. The next concrete marker is whether the book's launch correlates with a rise in retail net buying of equity ETFs over the subsequent four to six weeks. A sustained increase would confirm that the advice is converting into actual order flow. A flat reading would suggest the audience consumed the content without altering behavior, leaving the market impact contained. For now, the segment is a sentiment input, not a tradeable catalyst. The market analysis backdrop remains one where inflation surprises, such as the recent hot CPI print, can quickly reset rate expectations and test the conviction of new equity buyers.