Stocks● Neutral

Monsoon Slowdown Starting Thursday Risks India Kharif Planting

India's monsoon faces a western disturbance slowdown from Thursday, compressing the kharif planting window. ECMWF models show early pause; a Bay of Bengal circulation on June 22-23 could revive momentum.

Continue with

The vigorous monsoon that has swept India's west coast for the past several days is about to hit a speed bump. A western disturbance approaching northwest India will weaken the rain-bearing flows, according to the India Meteorological Department (IMD), and the European Centre for Medium-Range Weather Forecasts (ECMWF) suggests the slowdown may begin as early as Thursday.

The development creates a concrete catalyst for commodity markets, fertilizer demand projections, and rural consumption plays. A sluggish monsoon in the first half of June compresses the optimal planting window for kharif crops – cotton, sugarcane, paddy, and pulses – and raises the risk that sowing delays will pressure volumes later in the season.

Western Disturbance Interrupts Monsoon Flow

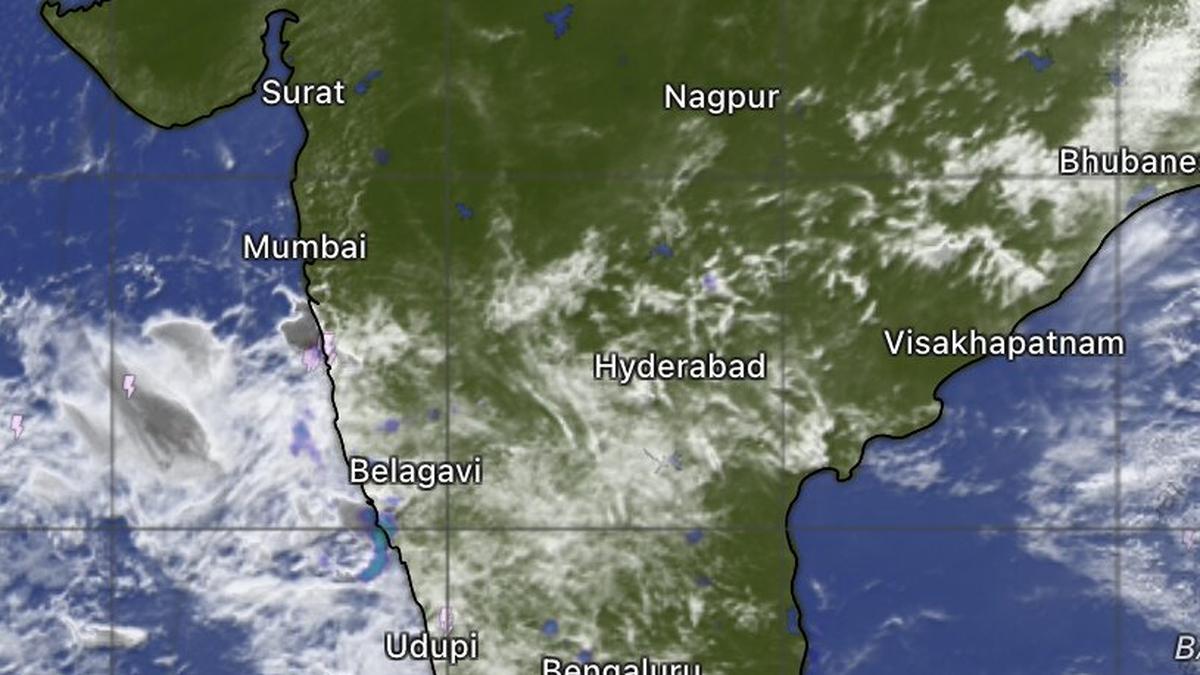

Satellite imagery Tuesday morning showed monsoon clouds south of Mumbai, extending toward the rest of the west coast up to Thiruvananthapuram. The rains remain active from Ratnagiri in Maharashtra through Panaji in Goa, Mangaluru in Karnataka, and into Kerala. Interior areas of Maharashtra, Karnataka, Telangana, Andhra Pradesh, and Tamil Nadu are reporting thundershowers.

A cyclonic circulation persists over the east-central Arabian Sea off the south Konkan coast, channeling moisture into Karnataka, Goa, Telangana, and Andhra Pradesh. Over Mumbai, however, winds are expected to stay weak, delaying the city's formal monsoon onset by several days.

The Intruder: Western Disturbance

An incoming western disturbance and its associated trough extending into the northeast Arabian Sea off the Konkan coast are expected to alter the monsoon's trajectory. The IMD states the disturbance will affect the Himalayan region over the next two days. A relatively weaker successor is expected around Saturday and may persist until June 17.

ECMWF modeling indicates the monsoon slowdown could begin as early as Thursday. Heavy rainfall on Wednesday will be largely confined to the coastal belt from Panaji through Karwar and Bhatkal to Mangaluru in Karnataka and Kannur in Kerala. After Wednesday, both the intensity and spatial extent of rainfall are likely to decrease progressively.

Why the Pause Matters for Market Read-Through

Monsoon performance is the single largest input for India's agriculture output and, by extension, for rural incomes, consumer demand, and inflation. Traders watch the June–July rainfall pattern for signals on commodity prices, tractor sales, fertilizer procurement, and fast-moving consumer goods (FMCG) demand in rural India.

Sowing Window Mechanics

Kharif planting typically peaks in June. A delay beyond the first week reduces the time window for crops that are sensitive to planting dates – cotton (late planting lowers yield), sugarcane (affects sucrose content), and paddy (requires sustained water for transplanting). If the monsoon remains sluggish through mid-June, acreage estimates will be trimmed, supporting prices for these commodities later in the season. Conversely, a revival in late June could restore the outlook.

Fertilizer demand also correlates directly with sowing progress. A slow start pressures inventory levels and margins for producers. The longer the delay, the higher the chance that demand spikes in a compressed window, testing logistics and pricing.