Stocks● Neutral

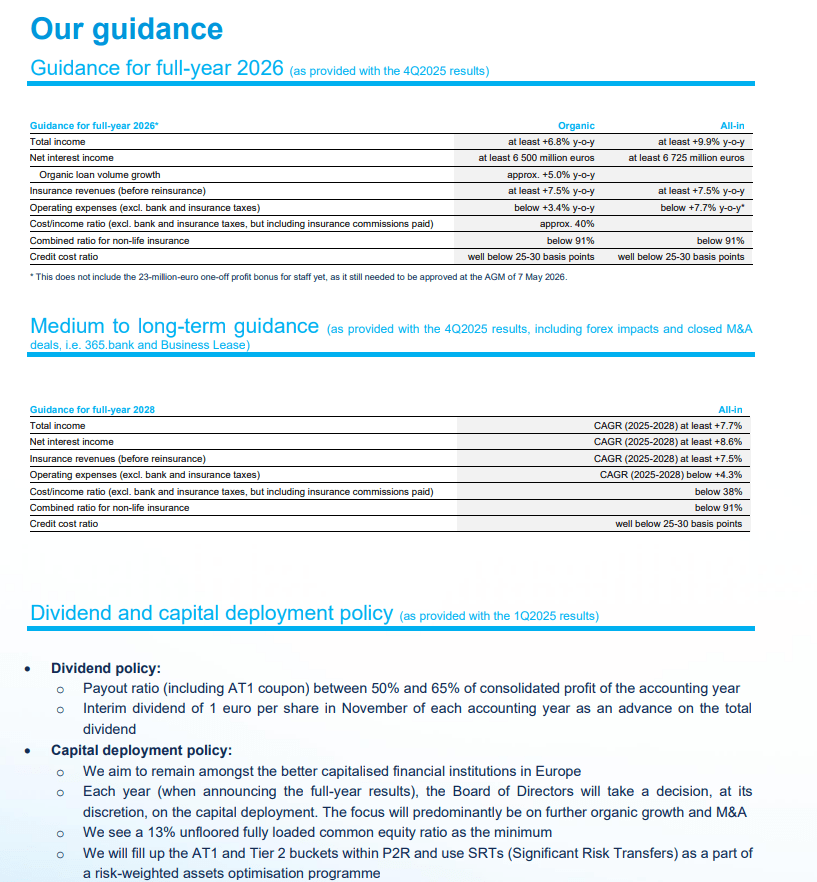

KBC Reaffirms FY26 Outlook as Net Interest Income Jumps 18% YoY

Q1 GAAP EPS of €1.32 on €3.23B total income, up 10.6% Y/Y. Net interest income rose 18% Y/Y. The reaffirmed FY26 outlook now defines the stock’s rate-path benchmark.

Continue with

KBC Group reported first-quarter GAAP earnings of €1.32 per share, lifting total income 10.6% year-on-year to €3.23 billion. The bank simultaneously reaffirmed its full-year 2026 guidance, anchoring the stock’s investment case to a specific rate-path assumption.

The immediate read is a clean print. A beat on net interest income (NII), a top-line acceleration, and an unchanged outlook signal that KBC is translating the higher-for-longer rate environment into income without suffering a credit-quality blowup. That simple take underpins the positive intraday reaction.

The better market read separates the headline NII surge from the underlying trajectory and asks whether the reaffirmed outlook prices in any ECB easing.

Net Interest Income: Headline vs Like-for-Like

NII reached €1.67 billion, rising 4% from the previous quarter and 18% from the same period a year ago. On a like-for-like basis – stripping out one-off items – the increase was a more measured 2% sequentially and 15% year-on-year. That gap matters. It says rate sensitivity is supplying a tailwind, yet underlying loan-book momentum is not running at the full headline pace.

The composition of NII growth also tells a real economy story. KBC operates primarily in Belgium, Central and Eastern Europe, and Ireland. The headline gearing suggests deposit margins are still widening while asset yields reprice upward with lag. The like-for-like deceleration hints that loan volumes are not compensating for the step-down in tailwind that arrives the moment ECB rate expectations pivot.