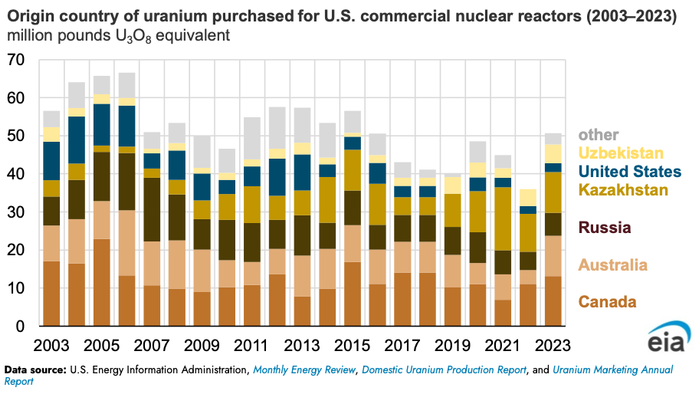

Kazakhstan has initiated plans to establish a strategic uranium reserve, a move that threatens to tighten an already strained global supply chain. As the world’s largest producer of the nuclear fuel, Kazakhstan’s decision to sequester a portion of its output directly impacts the availability of uranium for international markets. This shift in policy forces utilities and energy providers to reconsider their procurement strategies as the structural deficit in the uranium market becomes more pronounced.

Impact on Global Uranium Availability

The move by Kazakhstan creates an immediate bottleneck for global supply. Because the country accounts for a significant percentage of total global production, the removal of even a fraction of that volume for domestic reserves reduces the surplus available to Western markets. This development exacerbates the existing supply-demand imbalance that has persisted for years. Utilities that rely on long-term contracts with Kazakh producers now face increased competition for remaining spot market supplies.

This policy shift highlights the vulnerability of the nuclear energy sector to geopolitical decisions in key producing regions. When a major supplier prioritizes domestic security over export volume, the resulting scarcity forces price discovery to occur at higher levels. The market is now forced to account for a new variable where supply is no longer solely determined by mining capacity but by state-level strategic mandates.

Sector Read-Through and Valuation Risks

Energy companies with heavy exposure to nuclear power generation are the most exposed to this supply contraction. The cost of fuel, while historically a smaller portion of total operating expenses for nuclear plants, is becoming a more volatile line item. As producers and utilities adjust to these new constraints, the valuation of companies tied to the nuclear fuel cycle will likely undergo a repricing to reflect the increased cost of securing reliable supply.

AlphaScala data currently tracks various sectors with varying degrees of volatility. For instance, ON Semiconductor Corporation (ON stock page) holds an Alpha Score of 45/100 with a mixed label, while Agilent Technologies (A stock page) holds an Alpha Score of 55/100 with a moderate label. While these companies operate in different sectors, they illustrate the broader market environment where supply chain dependencies dictate performance metrics.

The Path to Market Equilibrium

The next concrete marker for this narrative will be the specific volume of uranium earmarked for the reserve and the timeline for its implementation. Any further announcements regarding export quotas or state-controlled inventory levels will serve as the primary catalyst for price volatility in the uranium spot market. Investors should monitor upcoming reports from major mining conglomerates operating in Kazakhstan, as these will provide the first clear indicators of how much production capacity will be diverted from the global market.

This situation remains linked to broader trends in stock market analysis where resource scarcity is increasingly driving sector-specific performance. The transition toward nuclear energy as a baseload power source requires a stable fuel supply, and any disruption to that stability will continue to influence capital allocation in the energy sector.