The Certification Clock

Joby Aviation continues to advance its regulatory timeline, yet the company remains a speculative play for investors. While the firm targets 2027 for full-scale monetization, the path to commercial viability is clouded by significant financial pressure. The company is actively working toward FAA certification, a process that is essential for its electric vertical take-off and landing (eVTOL) aircraft, but the timeline keeps the revenue-generating phase years away.

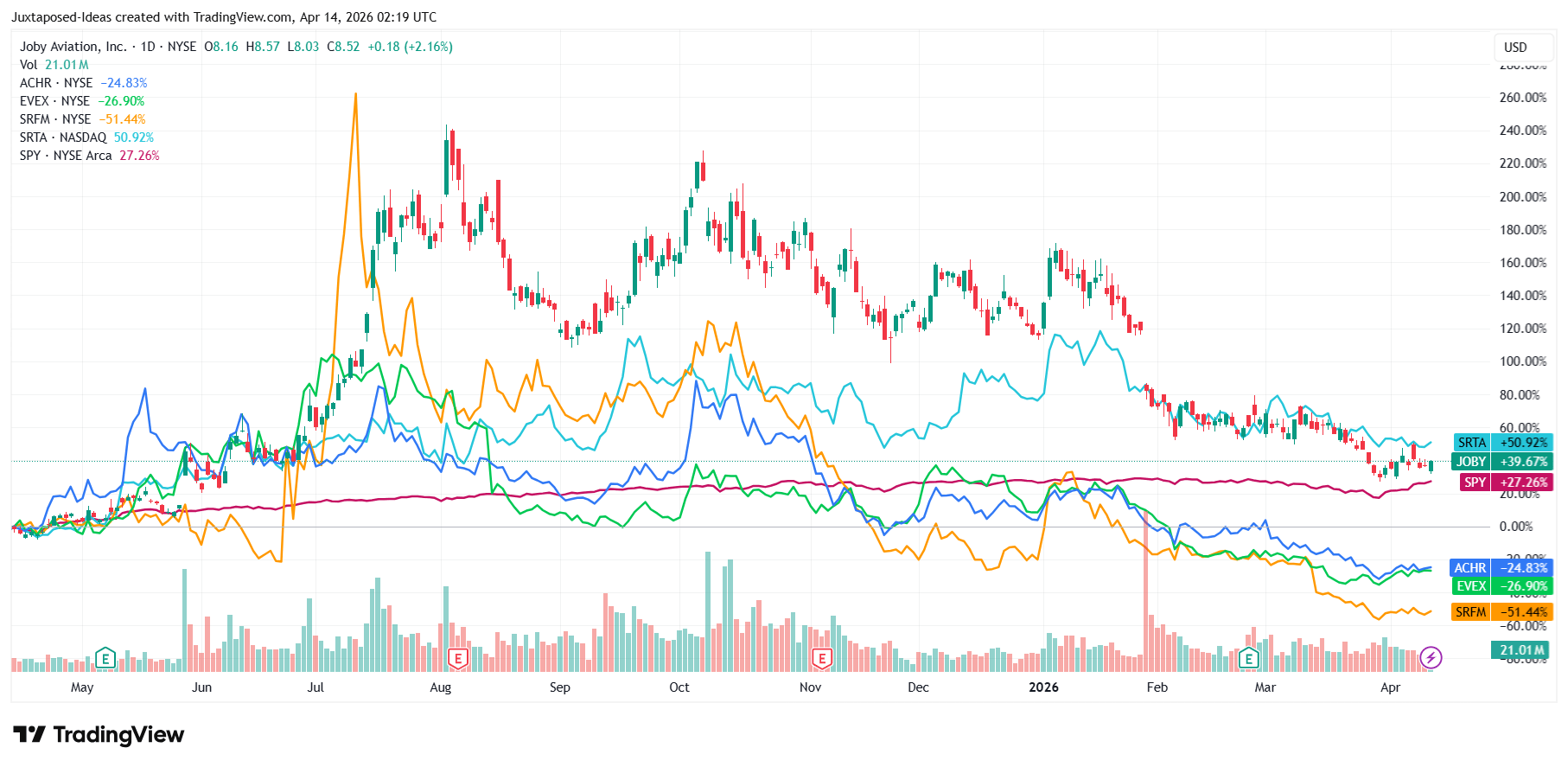

Investors looking for stock market analysis should note that certification progress does not immediately translate into profitability. The gap between current development costs and future revenue streams remains a primary concern for the market.

Strategic Partnerships and Defense Ties

Joby is not sitting idle while it waits for regulatory approval. The company has successfully expanded its footprint through high-level partnerships and defense contracts. These agreements provide a degree of validation for their technology, yet they do not offset the fundamental risks inherent in the business model.

Key developments include:

- Expansion in the UAE: New agreements aimed at establishing regional operations.

- Defense Contracts: Deepening ties with the U.S. military to test aircraft capabilities.

- Regulatory Milestones: Ongoing collaboration with the FAA to finalize airworthiness standards.

"While the company is hitting its operational markers, the burn rate is the metric that matters most for long-term holders," says one industry observer.

Financial Health and Risk Factors

Cash burn remains the most persistent threat to Joby’s equity value. The company is spending aggressively to fund its R&D and manufacturing facilities, and this trajectory is unlikely to change through 2026. Without a clear path to self-sustaining cash flow, the risk of dilution or future liquidity crises stays elevated.

The current valuation reflects a high degree of optimism regarding the eVTOL market. However, investors must reconcile this with the company's fiscal reality.

| Financial Metric | Status/Outlook |

|---|

| FAA Certification | Targeted for 2027 |

| Monetization Window | 2027 and beyond |

| FY2026 Guidance | High cash burn expected |

| Valuation Risk | Currently elevated |

Market Implications

For those evaluating their portfolios, Joby presents a classic high-risk profile. Traders who use best stock brokers to access speculative growth companies will find the stock price sensitive to any delay in the FAA timeline. When a company is years away from its first dollar of commercial revenue, the valuation is entirely dependent on the successful execution of technical and regulatory milestones.

If the company misses a deadline, the market reaction is often swift. Conversely, successful test flights or new contract wins provide temporary relief but rarely solve the underlying issue of capital consumption.

What to Watch Next

Investors should prioritize monitoring the company's quarterly cash burn rate rather than just the press releases regarding new partnerships. The transition from a prototype-focused entity to a commercial operator is where most companies in this sector struggle. Until Joby demonstrates a clear ability to contain expenses while maintaining its pace toward 2027, the risk-to-reward ratio remains unattractive for conservative capital.