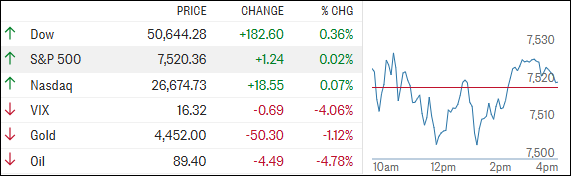

The Dow Jones Industrial Average opened with a 300-point surge and touched a fresh record high. Crude oil dropped nearly 5%. Procter & Gamble (PG) climbed more than 3% and helped lift the index. Micron Technology (MU) added another 4% after its 19% surge the prior day, pushing the stock past the $1 trillion market cap mark.

The catalyst was clear. President Trump said talks with Iran to end the conflict were "proceeding nicely."

"proceeding nicely"

By the close, the major indexes finished mostly flat. The Dow held a modest gain. The S&P 500 and Nasdaq erased their early advances. Bond yields ended little changed after an initial rise. The dollar spiked. Gold briefly lost the $4,500 level before bouncing off $4,400. Bitcoin extended its recent slide.

The Iran Headline Trade: Open High, Fade Close

The simple read

A headline that reduces geopolitical risk lowers the oil risk premium, cuts inflation expectations, and boosts consumer spending power. The Dow's early move reflected that logic.

The better market read

The afternoon fade tells a different story. Reports surfaced suggesting Iran peace talks might not be progressing as smoothly as the morning headlines implied. The crude oil bounce off the session lows reflected that shift. Bond yields reversed their initial rise. The market priced a single headline, not a verified outcome. When the headline's credibility weakened, the move reversed. The Dow's ability to hold a small gain does not confirm the thesis. It shows only that the unwind was incomplete by the close.

Key insight: The Iran talk trade is not confirmed. The rest of the session is a cautionary signal.

Oil's 5% Drop: Positioning Squeeze, Not Supply Shift

A 5% single-day drop in crude is a large move. The mechanism determines whether this is a trend change or a one-off.

What drove the move

The Iran headline was the trigger. Speculative long positions in crude had built up as geopolitical risk premia expanded. A headline that threatens to remove that premium forces a rapid unwind. The 5% drop is consistent with a positioning squeeze. It does not reflect a fundamental shift in global oil supply-demand balances.

What would confirm the move

A sustained drop requires either a verifiable Iran deal that adds supply or a demand-side shock. The OPEC+ production schedule and Chinese import data are the next concrete inputs. If crude stabilizes above recent support levels within two sessions, the headline-driven nature is confirmed.

What would weaken the thesis

Any escalation in Iran-related rhetoric or military activity would reverse the oil drop. The afternoon reports of less-smooth-than-hoped talks are exactly the kind of signal that would stop the crude selloff. A failed deal would re-inflate the risk premium.

Gold's $4,500 to $4,400 Route: Support Test

Gold briefly lost the $4,500 level before bouncing off $4,400. The move coincided with the dollar spike and the shift in Iran sentiment.

The mechanism

Gold sold off when the dollar strengthened and when the Iran headline reduced safe-haven demand. The bounce off $4,400 suggests buyers stepped in at that level, treating it as a support zone. The question is whether that support holds on a second test.

What would break gold

A sustained dollar rally would pressure gold further. If the Fed signals a slower pace of rate cuts, the dollar strengthens and gold likely tests $4,400 again. A confirmed Iran deal removes the geopolitical premium entirely.

What would support gold

Central bank buying remains a structural bid. If the dollar rally stalls and the Iran talks remain inconclusive, gold should hold the $4,400 to $4,500 range. The next Fed decision is the most likely catalyst for a breakout in either direction.

Micron and the Rotation into Memory Chips

Micron's 4% gain on top of the prior day's 19% surge pushed the stock past the $1 trillion market cap threshold. A UBS call citing long-term AI deals provided the catalyst.

The shift in AI exposure

Traders are gravitating toward memory chip names as the preferred AI play. This is a rotation from the earlier cycle where Nvidia and large-cap AI infrastructure dominated. Memory chips have a different risk profile: they are more cyclical, more dependent on spot pricing, and more exposed to the consumer electronics demand cycle.

The valuation question

A $1 trillion market cap for a memory chip maker requires sustained pricing power in a historically cyclical industry. The UBS thesis rests on long-term AI deals that lock in demand. If those deals materialize, the valuation can be justified. If AI demand slows or memory oversupply returns, the downside is significant.

Risk to watch: The memory cycle historically turns on supply additions. If competitors ramp production in response to the AI demand signal, pricing pressure will follow. The next earnings reports from Samsung and SK Hynix will provide the first real check.

The S&P 500 Divergence: 2% vs. 8,000

The strategist split on the S&P 500 outlook is unusually wide. One strategist calls for a modest 2% gain by year-end, citing rising bond yields and inflation expectations. Others target 8,000, pointing to continued earnings strength.

The 2% case

Rising bond yields compress equity risk premia. If the 10-year Treasury yield continues to climb, the S&P 500's forward P/E multiple contracts. Earnings growth would need to accelerate to offset that compression. The strategist making this call is betting that yields are the dominant variable.

The 8,000 case

An 8,000 target implies roughly a 30% gain from current levels. That requires either a significant multiple expansion or earnings growth well above consensus. The bull case rests on AI-driven productivity gains flowing through to corporate profits faster than the market currently prices.

Practical rule: When the range of strategist targets is this wide, the market is pricing a high degree of uncertainty. The correct response is to identify the data points that will resolve the divergence. The next CPI print and the Fed's June meeting are the two most likely catalysts.

Cycle Signals and the AlphaScala View

The domestic Trend Tracking Index (TTI) sits 7.15% above its moving average, with a Buy signal effective May 20, 2025. The International TTI stands 9.77% above its moving average, with a Buy signal effective May 8, 2025. Neither signal moved meaningfully on the session.

PG carries an Alpha Score of 52/100, labeled Mixed, in the Consumer Staples sector. The stock's 3% gain was a function of the Dow's oil-driven tailwind, not company-specific news. For traders tracking staples, the question is whether relative strength can persist if bond yields continue to rise.

Bottom line for traders: The Iran talk trade is not confirmed. Oil's 5% drop was positioning-driven, not fundamental. The Dow's record high was intraday only. Until the next concrete catalyst – a verified Iran deal, a CPI print, or a Fed decision – the market is likely to trade in a range. The S&P 500's 2% to 8,000 target range reflects that uncertainty, not a directional signal.

For related analysis on commodity positioning and energy sector risks, see our oil profile and gold profile. The APD at Bernstein: Hydrogen Spending Under the Microscope piece offers a parallel look at how policy headlines drive sector positioning.

| Asset | Intraday Move | Key Level |

|---|

| Dow Jones Industrial Average | +300 points (intraday high) | Record high |

| Crude Oil | -5% | Bounce from lows |

| Gold | Lost $4,500, bounced off $4,400 | $4,400 support |

| Micron Technology (MU) | +4% | $1 trillion market cap |

| Procter & Gamble (PG) | +3% | Contributed to Dow |

| Bitcoin | Extended slide | Not specified |