Back to Markets

Stocks● Neutral

Indonesian Export Push Threatens Malaysian Palm Oil Shipments

Malaysian palm oil exports fell 6.2% in May to 1.22M tons. An Indonesian export overhaul could deepen the slump. Watch the June 10 official data release.

Continue with

Malaysian palm oil exports could tumble for a third straight month in June if buyers favor cheaper Indonesian supplies as Jakarta’s overhaul of commodity shipments sparks a push to move cargoes before the new rules fully take hold. The shift threatens to deepen a slump that already pushed May shipments to their weakest level since February.

Indonesian Export Overhaul Reshapes Trade Flows

An Indonesian plan to take control of exports began on June 1, with producers expected to start submitting sales figures via newly formed state-owned firm PT Danantara Sumberdaya Indonesia. The system is still in a transition phase. Companies are allowed to keep handling transactions until Danantara takes over specific export activities as early as September, or by January 1 at the latest, senior officials said last week.

Why Cheaper Indonesian Supply Matters

Indonesian palm oil is currently more attractively priced than Malaysian supplies, giving the country room to capture market share, according to traders. There were initial expectations the new Indonesian rules would divert demand to Malaysia. That has not happened so far because key importers, especially those in India, had already made ample purchases in the first quarter, according to Paramalingam Supramaniam, a director at Selangor-based brokerage Pelindung Bestari Sdn.

The Mechanism: Pre-Policy Export Rush

The transition period creates an incentive for Indonesian producers to accelerate shipments before Danantara fully controls export activities. That dynamic, combined with already lower prices, puts direct pressure on Malaysian palm oil futures and the country’s export volumes.

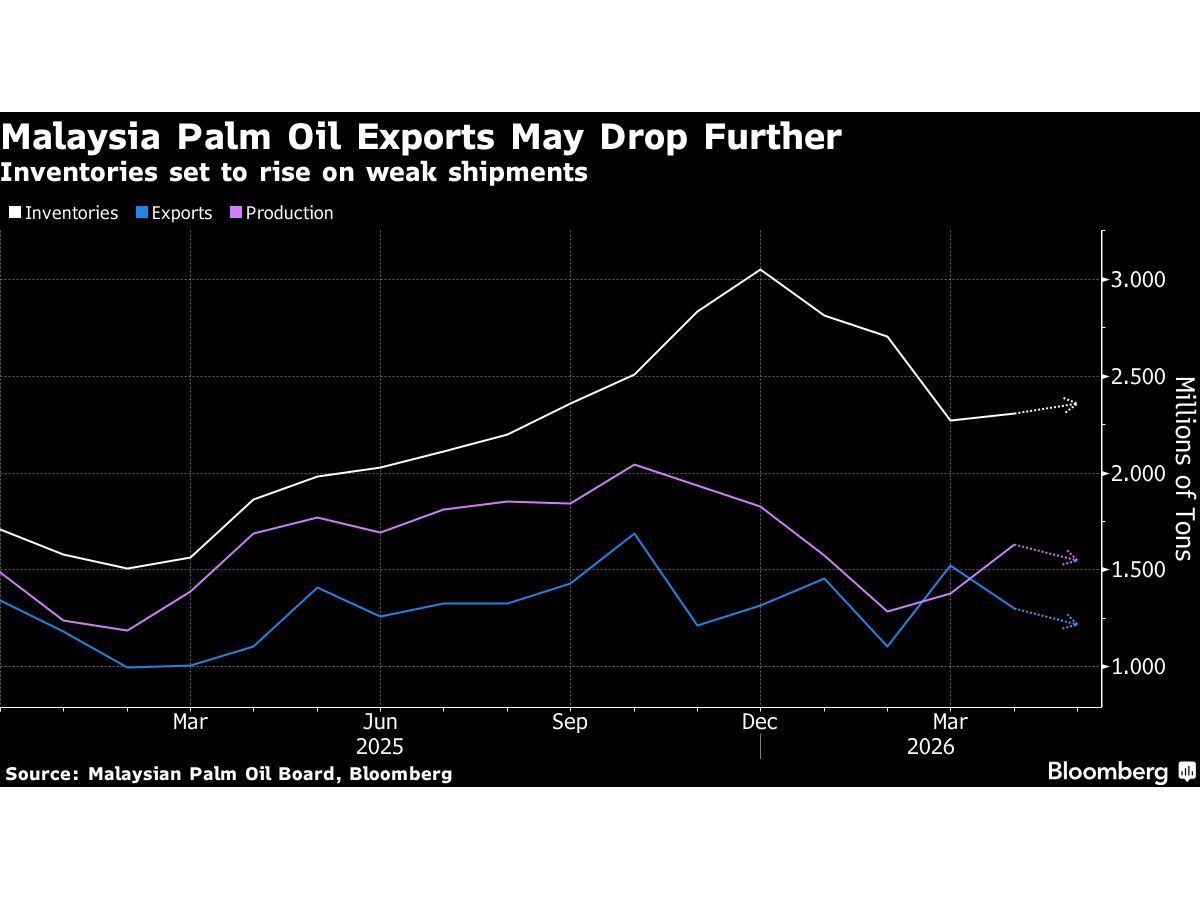

Malaysian Shipments Slump as Inventories Rise

Malaysian exports fell 6.2% in May from a month earlier to 1.22 million tons, according to the median of 11 estimates in a Bloomberg survey of plantation executives, traders and analysts. That is the weakest level since February, and follows a 14% drop in April.

Key May Data Points

- Exports: 1.22 million tons (down 6.2% month-over-month)

- Inventories: 2.36 million tons (up 2.2%)

- Crude palm oil production: 1.55 million tons (down 4.9%)

The Malaysian Palm Oil Board is scheduled to publish official figures on June 10. That release will either confirm the bearish trend or provide the first evidence of a recovery.

The Inventory Build Signals Weak Demand

Inventories rose even as production fell, a combination that typically points to demand destruction rather than supply constraints. The 2.2% inventory build to 2.36 million tons suggests that buyers are either well-stocked or switching to cheaper alternatives.