The Great Retreat: Investors Exit India

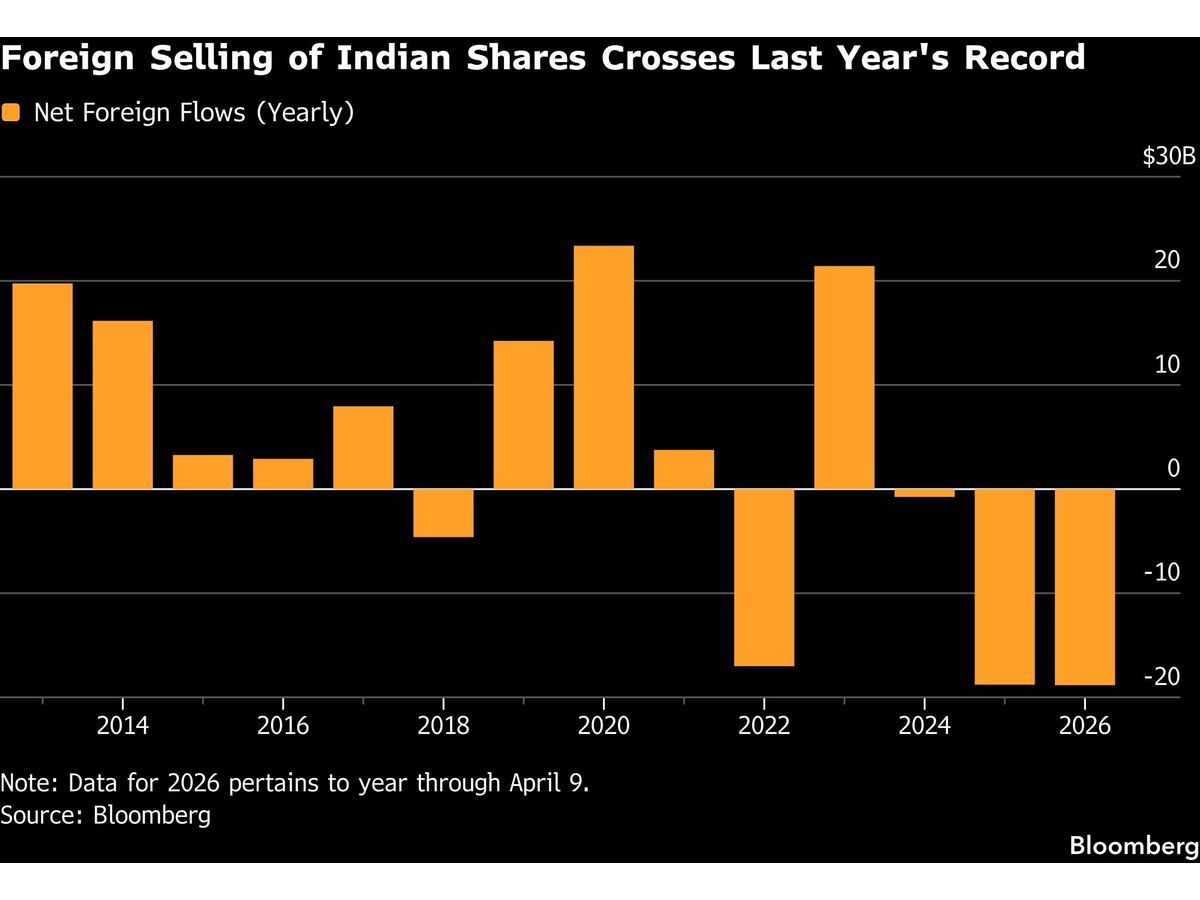

Global institutional investors are staging an unprecedented exodus from the Indian stock market, pulling capital at a record-shattering pace. This shift in sentiment marks a decisive end to the bull run that had positioned India as the world’s fastest-growing major economy. The primary catalyst for this liquidation is a mounting energy shock, exacerbated by the escalating conflict between the United States and Iran, which has sent shockwaves through energy-dependent emerging markets.

For months, India was the darling of the global emerging markets (EM) portfolio, buoyed by strong domestic consumption and resilient GDP figures. However, the current geopolitical climate has inverted that narrative, prompting international funds to reassess the risk-reward profile of the Nifty 50 and the broader BSE Sensex. The speed of the sell-off underscores a growing fear among institutional managers that the inflationary pressures of rising crude oil prices could systematically derail India's economic momentum.

Energy Shocks and Macroeconomic Fragility

India’s Achilles' heel has long been its reliance on imported energy. As a net importer of crude oil, the nation is disproportionately sensitive to volatility in the Middle East. The ongoing US-Iran friction threatens to disrupt supply chains and inflate the cost of energy imports, which directly impacts India’s current account deficit and weakens the rupee.

Market analysts note that the current “growth fears” are not merely speculative; they are anchored in the reality of input costs. As energy prices spike, corporate margins are expected to contract, forcing a downward revision of earnings forecasts for India’s heavyweights across the manufacturing, automotive, and logistics sectors. When global liquidity tightens due to geopolitical instability, India—previously seen as a 'safe haven'—is now being treated as a high-beta play that investors are keen to derisk.

What This Means for Traders

For traders, this record-breaking pace of divestment signals a potential shift in the structural trend of the Indian indices. Historically, India has benefited from the 'China Plus One' strategy, attracting massive inflows as global firms diversified away from Beijing. The current outflow suggests that geopolitical risk premium is now being priced into Indian assets with high urgency.

Traders should monitor the following key indicators:

- The Rupee (INR) / USD Pair: Any sustained weakness in the rupee will likely accelerate the flight of foreign capital, as dollar-denominated returns for international investors continue to evaporate.

- Crude Oil Benchmarks: As long as the US-Iran situation remains unresolved, the volatility in Brent and WTI crude will remain the primary driver for Indian market sentiment.

- Foreign Institutional Investor (FII) Flows: Daily data releases on FII activity will be critical in determining whether this is a short-term liquidity event or a long-term repositioning of portfolios.

The Outlook: A Balancing Act

Looking ahead, the resilience of the Indian market will depend on whether domestic institutional investors (DIIs) can absorb the selling pressure from their foreign counterparts. While domestic retail participation has been a pillar of support for the Indian bourses over the past three years, the sheer volume of the current foreign exit is testing the limits of that support system.

Investors should remain cautious. While India’s long-term macroeconomic fundamentals—such as its demographic dividend and digital infrastructure—remain intact, the short-term outlook is dominated by external macro shocks. Until the geopolitical landscape stabilizes and the energy-linked inflationary pressure on the rupee eases, the path of least resistance for Indian equities appears to be to the downside.