Back to Markets

Stocks● Neutral

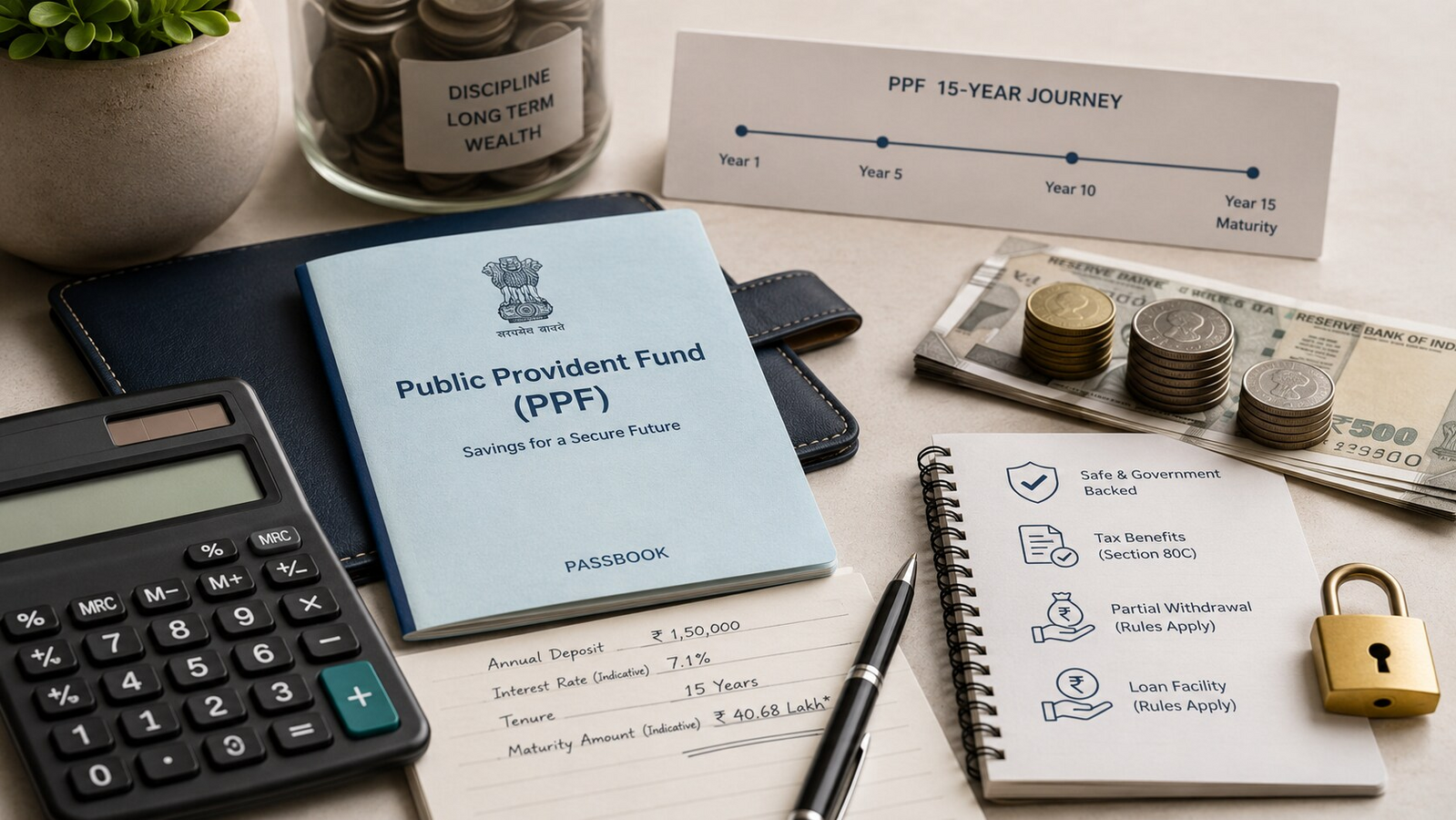

How ₹5,000 monthly PPF for a child compounds over 30 years

A ₹5,000 monthly PPF contribution at 7.1% grows to ₹60.5 lakh over 30 years. Delaying eight years cuts the corpus by over ₹26 lakh.

Continue with

The public provident fund (PPF) has been around since 1986. It is a government-backed savings scheme with a guaranteed interest rate, currently at 7.1%. For parents looking to build a long-term corpus for a child's education, wedding, or even a first home, the math on consistent contributions is straightforward.

You can open a PPF account at any post office or bank branch with standard KYC documents. A parent or legal guardian can open it for a minor. The account must be converted to the child's name once they turn 18.

The core question is how much a fixed monthly contribution grows over time. Take ₹5,000 per month. At the current 7.1% rate, a 30-year investment window produces a corpus of roughly ₹60.5 lakh. That number drops sharply if the start is delayed. A 22-year window – starting when the child is eight rather than at birth – yields about ₹34.4 lakh. The difference in final value is over ₹26 lakh.

Delaying by eight years costs more than a quarter of the final corpus. That is the single biggest variable in the PPF calculation, and it is the one thing a parent controls completely.

The scheme has a 15-year lock-in, extendable in blocks of five years. Contributions are tax-deductible under Section 80C up to ₹1.5 lakh per year. The interest is tax-free. These features make PPF one of the few remaining instruments where the entire return is post-tax, which matters for anyone in a higher tax bracket comparing it to fixed deposits or debt mutual funds.

A few practical points. The minimum annual deposit is ₹500. The maximum is ₹1.5 lakh in a financial year. Missing a year does not close the account but triggers a penalty of ₹50 per year. The account can be closed only after the 15-year lock-in, or earlier for specific reasons like higher education or medical emergency.