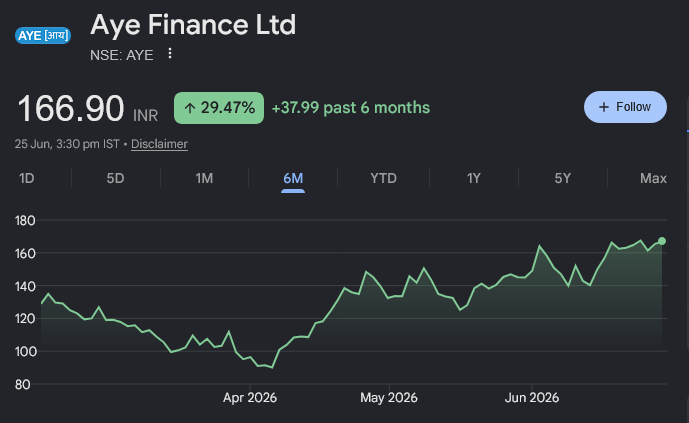

Goldman Sachs and the Abakkus 4to8 Fund are among the institutional investors backing AYE Finance, a recently listed non-bank lender focused on India's micro and small enterprises. The stock, which listed in February 2026 at ₹129 per share, has climbed roughly 30% to a market cap near ₹4,144 crore.

AYE Finance does not lend to large corporates or salaried borrowers. Its average loan ticket is about ₹1.8 lakh, targeting small manufacturers, traders and service providers that formal banks often bypass. That niche sits inside a structural gap: India's MSME sector contributes roughly 30% of GDP but faces a credit shortfall that specialized lenders are trying to fill.

The company's Assets Under Management stood at ₹6,027 crore as of the latest filing, having grown at a 30% CAGR between FY23 and FY25. That pace suggests the underwriting model is scaling without obvious strain, though the real test will come as the book ages and the portfolio moves beyond the early-vintage tailwind.

Goldman's participation is worth noting less for the dollar amount than for the signal. The firm does not typically surface in micro-MSME lending at this stage of a company's life. Abakkus, a domestic multi-asset manager, adds a layer of local market knowledge that foreign allocators often lack when evaluating Indian NBFCs.

The stock has already repriced since the IPO. At current levels, the question is whether AYE can sustain 30% AUM growth while keeping credit costs contained. The company's loan book is concentrated in unsecured or lightly secured products, which means asset quality will matter more than origination speed over the next two to three reporting cycles.

For now, the institutional backing gives the story a floor. The ceiling depends on execution in a segment where defaults tend to cluster during economic slowdowns, not expansions. The next quarterly update will show whether the growth trajectory is intact or starting to moderate.