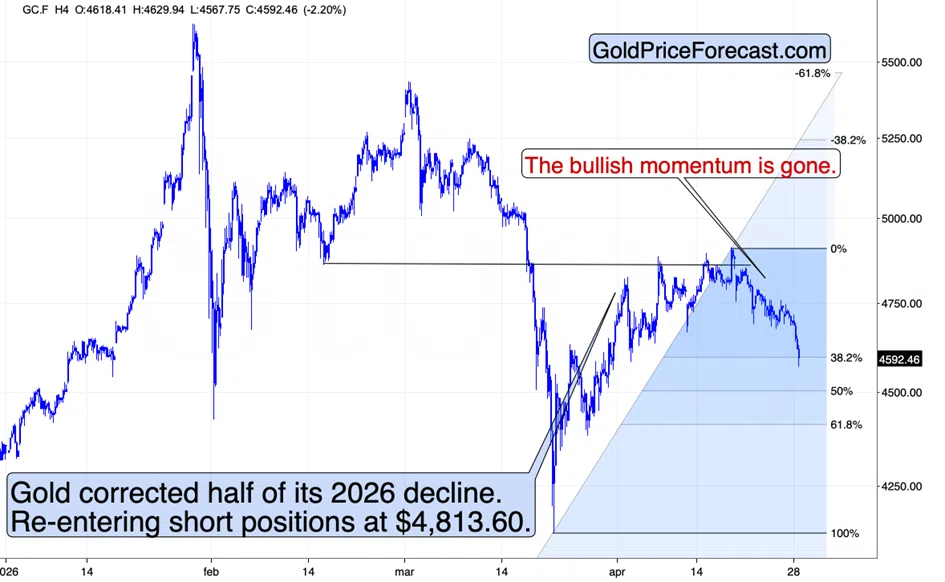

Precious metals are currently facing a significant disconnect between geopolitical instability and price performance. Despite urgent warnings from international bodies regarding global food security and escalating regional conflicts, gold and silver prices have trended downward. This movement suggests that the traditional role of gold as a primary safe-haven asset is being superseded by broader macroeconomic pressures, specifically the persistent strength of the U.S. dollar.

Dollar Strength and Liquidity Constraints

The inverse relationship between the U.S. dollar and gold remains the dominant driver of current price action. When the dollar appreciates, gold becomes more expensive for holders of foreign currencies, which suppresses global demand. This currency dynamic is currently outweighing the fear premium typically associated with geopolitical crises. Investors are prioritizing liquidity and yield-bearing assets over non-yielding precious metals, leading to a rotation of capital out of the gold market.

Mining stocks have mirrored the decline in physical metal prices, indicating that the market is discounting the future profitability of extraction operations. This sell-off in the mining sector suggests that investors are not merely reacting to short-term price fluctuations but are reassessing the long-term valuation of gold-linked equities. The lack of a sustained rally during periods of high uncertainty points to a shift in how institutional capital perceives risk-adjusted returns in the current interest rate environment.

Structural Weakness in Precious Metals

The current market environment for gold is characterized by several factors that hinder a recovery:

- Increased opportunity costs associated with holding gold in a high-interest-rate environment.

- A lack of sustained physical buying interest at current price levels.

- Technical selling pressure that has accelerated as key support levels were breached.

These factors have created a feedback loop where downward momentum attracts further technical selling. While geopolitical tensions usually provide a floor for gold prices, the current lack of response suggests that the market is currently more sensitive to monetary policy and currency valuations than to external security threats. This trend is consistent with broader shifts in global asset allocation, as detailed in our record gold valuation signals shift in global asset allocation analysis.

AlphaScala data currently tracks various market segments for potential volatility. For those monitoring consumer staples and cyclicals, Kellanova holds an Alpha Score of 56/100, while Amer Sports, Inc. maintains an Alpha Score of 47/100, reflecting the mixed sentiment currently permeating consumer-facing sectors.

Market participants should look to the next Federal Reserve policy meeting and upcoming inflation data as the primary catalysts for a potential reversal. If the dollar begins to soften in response to shifting economic indicators, gold may regain its status as a hedge. Until then, the disconnect between geopolitical headlines and metal prices is likely to persist, making the next monthly employment report a critical marker for determining whether the dollar maintains its current dominance or begins to lose momentum.