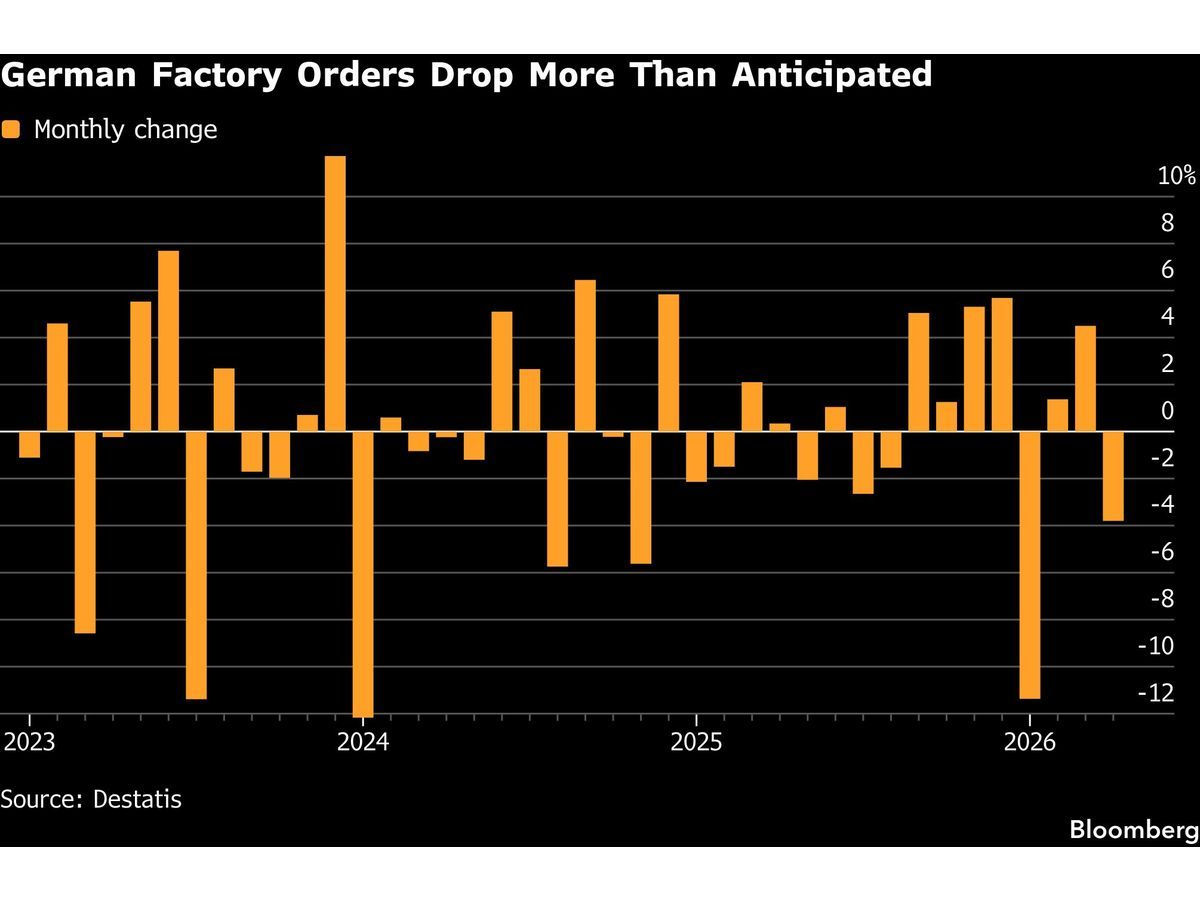

German factory orders fell more than expected in April, deepening concerns that Europe's largest economy may contract in the second quarter as the impact of the Iran conflict and surging energy costs intensifies.

Demand dropped 3.8% month-on-month, the statistics office Destatis reported Monday, far worse than the 2% decline forecast in a Bloomberg survey. The reading followed a downwardly revised 4.5% gain in March. The automotive industry and electrical equipment drove the drop, with machinery and equipment also contributing. Destatis noted large-scale orders had no impact. A less volatile three‑month comparison showed a 3.1% fall.

Why April's Order Miss Changes the Growth Outlook

The Simple Read: Q2 GDP Now at Risk

Germany's economy grew 0.3% in the first quarter. Business activity contracted in both April and May. The factory orders miss adds a hard data point to the anecdotal softening. The economy ministry said in a statement that rising energy and commodity prices, together with heightened geopolitical uncertainty, are reducing demand, particularly for capital goods. Against this backdrop, the ministry expects industrial activity to show only modest growth in the months ahead.

The Better Read: The Transmission Mechanism Runs Through Capital Goods

The drop was concentrated in capital goods orders – the machinery, equipment, and electrical gear that signal corporate investment plans. When capital goods orders fall, the lagged effect hits industrial production, employment, and tax receipts over the following two to three quarters.

Joerg Kraemer, chief economist at Commerzbank, warned the economy will probably "contract slightly" in the second quarter. A second‑quarter contraction would qualify as a technical recession if confirmed by the third quarter.

The Conflict Channel: How the Iran War Hits German Industrial Demand

Direct Input Costs and Supply Chain Bottlenecks

Germany is a net energy importer. The conflict in the Middle East has lifted oil and gas prices materially since March. Higher input costs compress margins in energy‑intensive sectors – metals, chemicals, automotive – which respond by deferring new equipment orders and paring production.

The economy ministry explicitly cited "growing supply chain bottlenecks" as a factor. For German manufacturers that rely on just‑in‑time delivery, any disruption in Red Sea or Gulf transit routes directly impairs production scheduling.

The Second‑Order Effect: Policy Uncertainty Slows Decision‑Making

Companies facing an unpredictable geopolitical environment tend to shift from expansion to cash preservation. Capital goods orders are discretionary. They are the first line item to get cut when CFOs see no clarity on energy costs, trade policy, or demand six months out.

The drop in electrical equipment orders is a textbook example. That sub‑sector is heavily exposed to export demand and requires multi‑year investment cycles in semiconductor and automation equipment. When order books thin, the response chain runs from procurement freezes to hiring pauses to inventory destocking.

The Interest Rate Headwind: ECB Tightening Collides With Weakening Demand

The Rate Hike Is Now a Growth Risk

The European Central Bank is widely expected to raise borrowing costs later this week. For the German economy, that timing compounds the damage from the factory orders miss. If the ECB delivers a hike while industrial demand is already contracting, the transmission to business lending rates will slow the recovery in capital expenditure.

What This Changes for the Bund Yield and the Euro

Factory orders that undershoot by nearly 2 percentage points typically push the Bund yield lower and weigh on the euro against the dollar. The ECB rate decision is the dominant variable this week. A dovish hike – where the ECB hikes but signals a pause – could cap Bund yields and give the euro temporary support. A hawkish hike with no pause signal would reinforce the growth‑over‑rates trade, steepening the curve as short‑end yields rise while long‑end yields fall on growth concerns.

The Fiscal Impulse Gap: Why the Infrastructure Fund Hasn't Offset the Weakness

The €500 Billion Fund: Sluggish Start, Slowest Transmission

Data last week showed that the €500 billion ($577 billion) infrastructure fund had a sluggish start. The fund is designed to channel stimulus into defense and public infrastructure, which should support industrial orders through procurement and construction. The lag between fund allocation and actual order placement is measured in quarters, not months.

Why This Matters for the Setup

The fiscal booster would arrive when industrial demand is already in a downcycle. That creates a divergence. Short‑term indicators – PMIs, factory orders, capacity utilization – will continue to deteriorate for at least two to three months before the infrastructure money shows up in factory order books. The risk is that the recovery narrative gets priced in too early, then disappointed by hard data.

Chancellor Merz's Growth Forecast Meets Political Headwinds

A 2026 Promise That Contradicts the 2025 Data

Friedrich Merz predicted that 2026 would be a "year of growth." The April factory orders data puts that forecast at risk. If the German economy contracts in Q2 2025, Merz faces a recession that begins 18 months before his promised recovery. The political friction is already visible: party unrest over his plummeting popularity limits his capacity to push through structural reforms or expedite infrastructure spending.

The risk is that political gridlock delays the fiscal response, which in turn makes the industrial downturn deeper and longer than the ECB's rate path alone would cause.

What Would Confirm the Political Risk Scenario

- A delay or reduction in the €500 billion infrastructure fund's disbursement schedule.

- A failed confidence vote or coalition realignment that pushes industrial policy to the back burner.

- A worsening in business confidence indices (Ifo, ZEW) that specifically cite political uncertainty rather than energy costs or rates.

Affected Assets and Watchlist Items

The Direct Bearish Trade

- German industrial equities (Siemens, ThyssenKrupp, automotive supply chain) face margin compression from rising energy costs and weakening order books.

- DAX futures: a Q2 contraction would put pressure on earnings expectations, making the index vulnerable to further multiple compression unless the ECB explicitly pivots.

- Bund futures: a flight‑to‑safety bid will strengthen if the ECB's hike is seen as a mistake. The short end of the curve (2-year Schatz) will be more sensitive to the rate decision. The long end (30-year Bund) will respond to the growth downgrade.

The Conditional Risk-On Trade

- German defense contractors: if the infrastructure fund is redirected or accelerated toward military procurement, the orders could offset weakness in commercial capital goods. This remains speculative until disbursement data improves.

- Euro‑denominated credit: investment‑grade corporate bonds tighten slowly if the ECB signals a rate pause. The April orders miss increases the probability of that signal. A collapse would arrive only if the Q2 GDP print comes in negative.

What Weakens the Bearish Thesis

- A surprise rebound in May factory orders above 2% would break the three‑month trend. The next release is due in early July.

- An ECB hike paired with explicit forward guidance that the tightening cycle is finished. That would front‑load the recovery in business confidence.

- A rapid uptick in infrastructure fund disbursements, measured by public tenders hitting the EU procurement database.

The April factory orders report sets a low bar for May. If the consensus expects a recovery after the -3.8% print, a negative number would confirm an industrial recession regardless of ECB action. The next confirmatory data point is the May factory orders release scheduled for early July. Between now and then, weekly PMI readings and the ECB rate decision will set the intraday narrative. The hard data remains the only signal that changes the structural outlook for German industrial exposure.