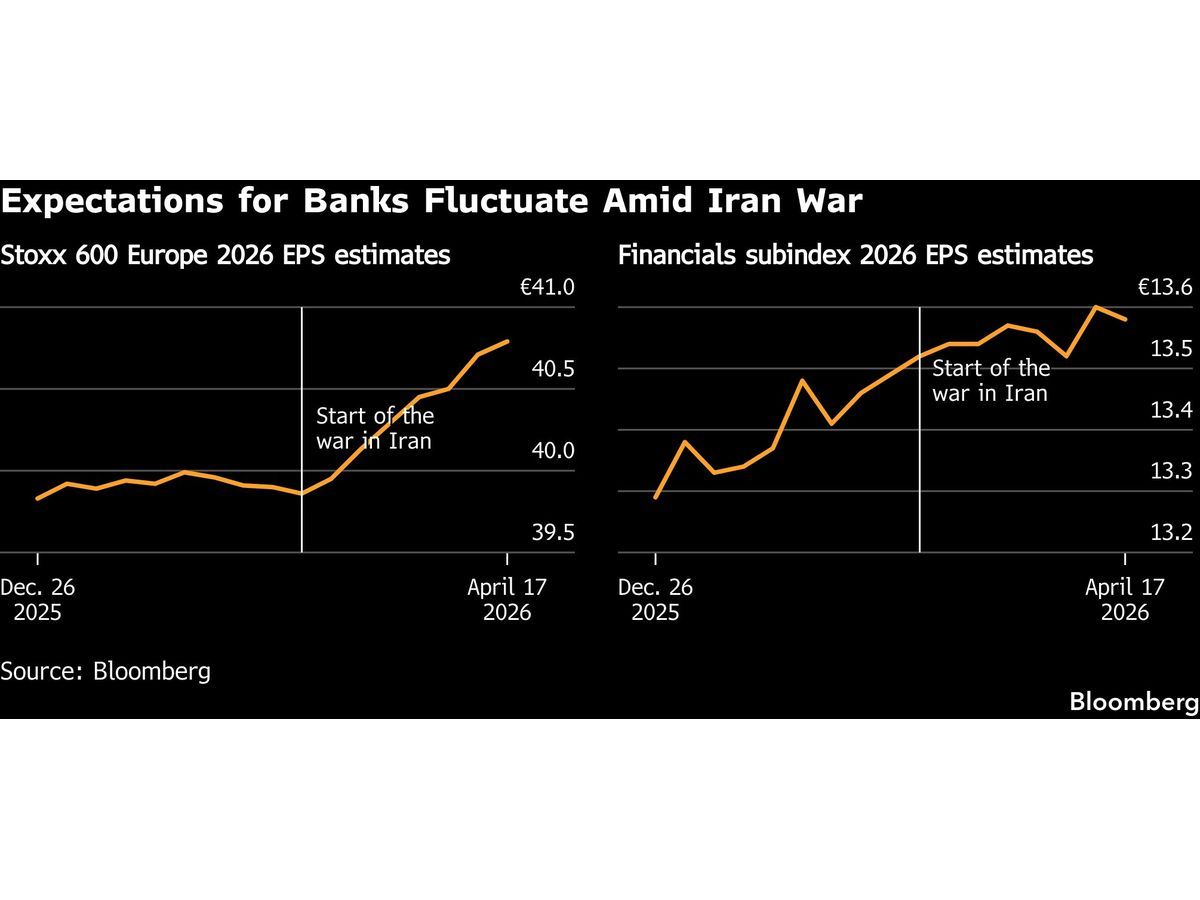

European banks are entering the current reporting cycle facing a cooling outlook as the momentum from strong fourth-quarter earnings encounters new pressure from geopolitical instability and slowing loan demand. While the sector previously benefited from a period of high interest rates and robust net interest margins, the current environment suggests that the tailwinds supporting these record performances are beginning to fade.

Lending Volume and Margin Compression

The primary challenge facing the sector is the intersection of stagnant loan growth and the potential for rising credit costs. As economic activity in key European markets remains muted, the demand for corporate and retail credit has failed to recover to levels seen in previous cycles. Banks are now navigating a landscape where the benefit of higher deposit rates is being offset by the need to increase provisions for potential loan losses. This shift is forcing institutions to re-evaluate their revenue projections for the remainder of the fiscal year.

Operational efficiency has become the secondary focus for management teams attempting to protect bottom-line results. With revenue growth constrained, cost-cutting measures are being prioritized to maintain capital ratios. The ability of these banks to sustain their current dividend and buyback programs will depend heavily on whether they can stabilize their net interest margins despite the broader macroeconomic uncertainty.

Geopolitical Risk and Capital Allocation

Geopolitical tensions are creating a direct impact on the risk appetite of major European lenders. Exposure to regions affected by ongoing conflict is forcing banks to tighten underwriting standards, which further suppresses lending volume. This risk-averse posture is a departure from the aggressive expansion strategies observed throughout the previous year.

Investors are currently monitoring how these institutions allocate capital in a period of low growth. The following list highlights the key variables currently influencing bank balance sheets:

- Increased loan loss provisioning due to regional economic volatility.

- Stagnant demand for new corporate credit lines.

- Pressure on net interest margins as deposit costs remain elevated.

For those tracking the broader financial landscape, recent results from regional players like the Bank of Queensland Reports Q2 2026 Results Amid Margin Pressures provide a useful comparison for how interest rate environments are impacting mid-tier and large-cap institutions differently. While European banks have historically maintained stronger capital buffers, the current environment tests the resilience of these reserves against a backdrop of persistent inflation and geopolitical risk.

AlphaScala data reflects the current sentiment across various sectors, with AS (Amer Sports, Inc.) currently holding an Alpha Score of 47/100, indicating a mixed outlook as consumer-facing firms navigate similar macroeconomic headwinds. The next concrete marker for the banking sector will be the mid-quarter regulatory disclosures, which will provide the first clear look at how loan portfolios are performing under the stress of current interest rate policies and geopolitical pressures.